Fill Out a Valid 96 Alabama Form

Fill Out a Valid 96 Alabama Form

The 96 Alabama form serves as a vital document for ensuring compliance with state income tax regulations. It summarizes annual information returns and is particularly important for individuals, corporations, and associations that make significant payments of $1,500 or more to taxpayers subject to Alabama income tax. This form must be submitted to the Alabama Department of Revenue by March 15 of the following year, capturing all relevant payments made during the calendar year. When filing, it is essential to include details such as the payer's Social Security number or Federal Employer Identification Number (FEIN), along with their address and signature. Additionally, if Alabama income tax has been withheld from the payments, the form directs users to file a different form, known as Form A-3, instead. For those who have voluntarily withheld taxes, it is crucial to file Form 99 or an approved substitute, regardless of the payment amount. Understanding these requirements helps ensure that all necessary information is accurately reported, thus avoiding potential penalties or issues with the state tax authority.

Misconceptions about the 96 Alabama form can lead to confusion and errors in filing. Here are seven common misunderstandings:

Understanding these misconceptions can help ensure compliance and accuracy when dealing with Alabama tax filings.

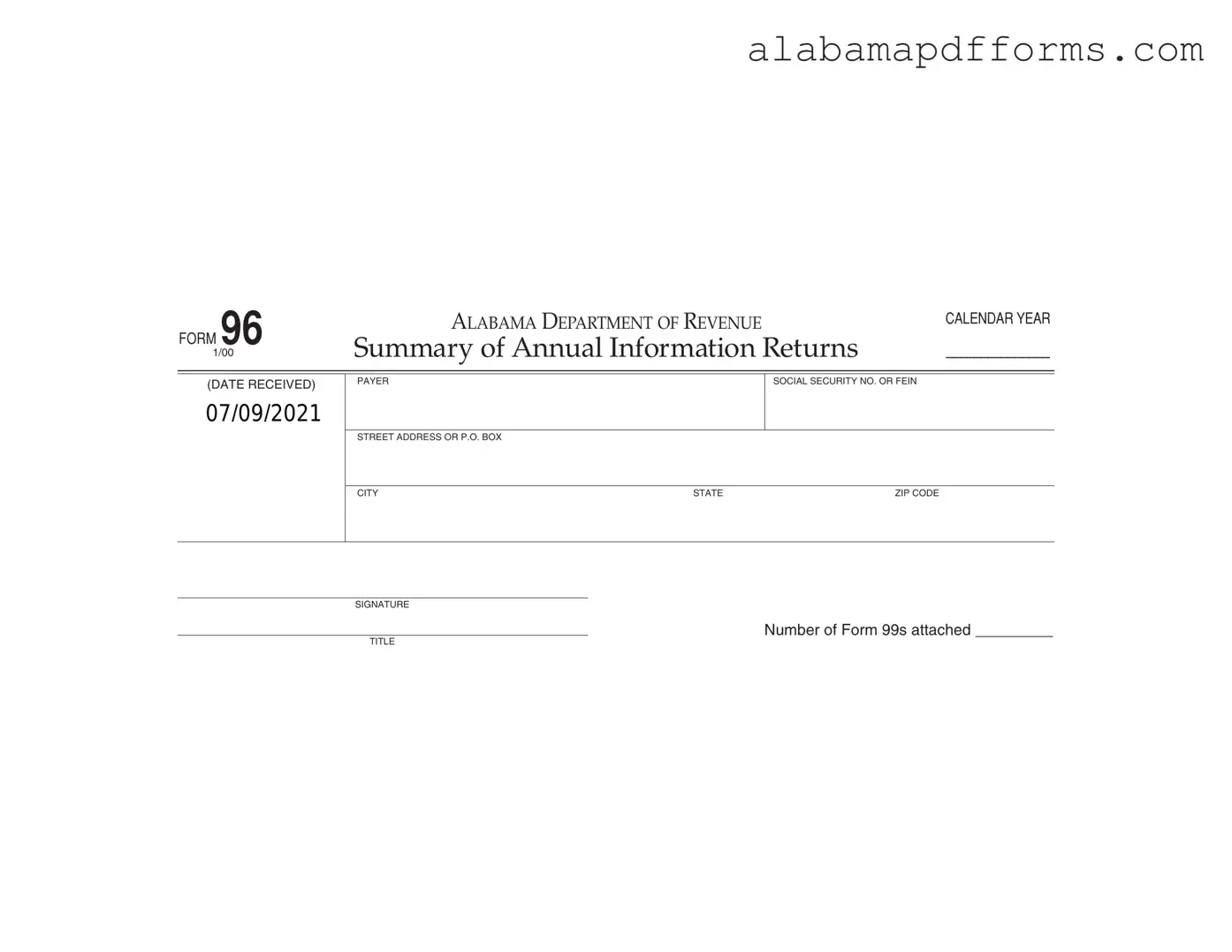

FORM 96 |

ALABAMA DEPARTMENT OF REVENUE |

CALENDAR YEAR |

|

|

|

1/00 |

Summary of Annual Information Returns |

_______________ |

(DATE RECEIVED)

07/09/2021

PAYER |

SOCIAL SECURITY NO. OR FEIN |

STREET ADDRESS OR P.O. BOX

CITY |

STATE |

ZIP CODE |

SIGNATURE

NUMBER OF FORM 99S ATTACHED _________

TITLE

Instructions

Information returns on Form 99 must be filed by every resident individual, corporation, association or agent making payment of gains, profits or income (other than interest coupons payable to bearer) of $1,500.00 or more in any calendar year to any taxpayer subject to Alabama income tax. If you have voluntarily withheld Alabama income tax from such payments, you must file Form 99 or approved substitute regardless of the amount of the payment. Employers filing Form

Returns must be filed with the Alabama Department of Revenue for each calendar year on or before March 15 of the following year.

Mail to: Alabama Department of Revenue |

NOTE: IF ALABAMA INCOME TAX HAS BEEN WITHHELD ON FORM 99 |

Individual & Corporate Tax Division |

DO NOT USE THIS FORM; USE FORM |

P.O. Box 327489 |

OF ALABAMA INCOME TAX WITHHELD. |

Montgomery, AL |

|

Alabama Lost Title - Failure to accurately complete the form can result in rejection by the Alabama Department of Revenue.

For those looking to navigate the complexities of estate planning, the process can be greatly simplified by utilizing a user-friendly Last Will and Testament form that helps ensure your assets are distributed per your wishes.

Alabama Income Tax Forms - Additional information about lodging tax can usually be found on the department's website.

The IRS Form 1099 is one of the most comparable documents to the Alabama Form 96. Both forms serve the purpose of reporting income paid to individuals or entities. The 1099 form is used at the federal level to report various types of income, including non-employee compensation, interest, and dividends. Just like the Alabama Form 96, the 1099 requires information about the payer and the recipient, including their identification numbers and addresses. The threshold for reporting income on the 1099 form is also similar, as it typically requires reporting payments of $600 or more, which aligns with the Alabama requirement for Form 99.

Another document that shares similarities with the Alabama Form 96 is the W-2 form. Employers use the W-2 to report wages, tips, and other compensation paid to employees. While the W-2 is specifically for employee earnings, both forms require the payer to provide detailed information about the payments made. Additionally, both documents must be filed with the respective tax authorities by a certain deadline, ensuring that income reporting is timely and accurate. The W-2 form also includes information about any taxes withheld, similar to how the Alabama Form 96 addresses withholding for income tax.

The 1098 form, which is used to report mortgage interest payments, also bears resemblance to the Alabama Form 96. Both documents require payers to report payments made to individuals or entities, and they must include identifying information for both the payer and the recipient. While the 1098 focuses on interest payments specifically, it shares the same purpose of ensuring transparency in financial transactions. Both forms are crucial for the tax filing process, as they provide necessary information for the recipients to accurately report their income on their tax returns.

In the context of legal documentation, it's also essential to consider a Hold Harmless Agreement, which serves as a protective measure for parties involved in activities that may pose risks. This agreement ensures that one party cannot hold the other accountable for any claims or damages arising from those activities, thereby providing a layer of security similar to that found in various tax forms where compliance and clarity are crucial.

The Schedule K-1 is another document that has similarities with the Alabama Form 96. Used by partnerships and S corporations, the K-1 reports each partner's or shareholder's share of income, deductions, and credits. Like the Alabama Form 96, the K-1 requires detailed information about the entity making the payments and the individuals receiving them. Both forms play a vital role in ensuring that all parties report their income correctly for tax purposes. The K-1 also needs to be provided to recipients by a specific deadline, similar to the requirements of Form 96.

Lastly, the Form 1042-S is comparable to the Alabama Form 96 in that it reports income paid to foreign persons. This form is used to report amounts subject to withholding, such as interest, dividends, and royalties. Both forms require the payer to disclose information about the payments made and the recipients, ensuring compliance with tax regulations. The Form 1042-S is particularly focused on payments to non-resident aliens, while the Alabama Form 96 pertains to income subject to Alabama state tax, but both share the overarching goal of accurate income reporting.

When filling out the 96 Alabama form, many individuals make common mistakes that can lead to delays or issues with processing. One frequent error is failing to include the correct Payer Social Security Number or FEIN. This number is crucial for identification purposes. Without it, the form may be rejected, causing unnecessary complications.

Another mistake often seen is neglecting to provide a complete street address or P.O. Box. Incomplete addresses can result in miscommunication and delays in processing the form. Ensure that the address is accurate and includes all necessary components, such as the city, state, and ZIP code.

Many people also overlook the importance of signing the form. A signature is required to validate the submission. Without it, the form will be considered incomplete, which can lead to additional follow-up from the Alabama Department of Revenue.

Lastly, failing to indicate the number of Form 99s attached is a common oversight. This information helps the department process the returns efficiently. If this detail is missing, it may cause confusion and delay in processing the overall submission.