Fill Out a Valid A 3 Alabama Form

Fill Out a Valid A 3 Alabama Form

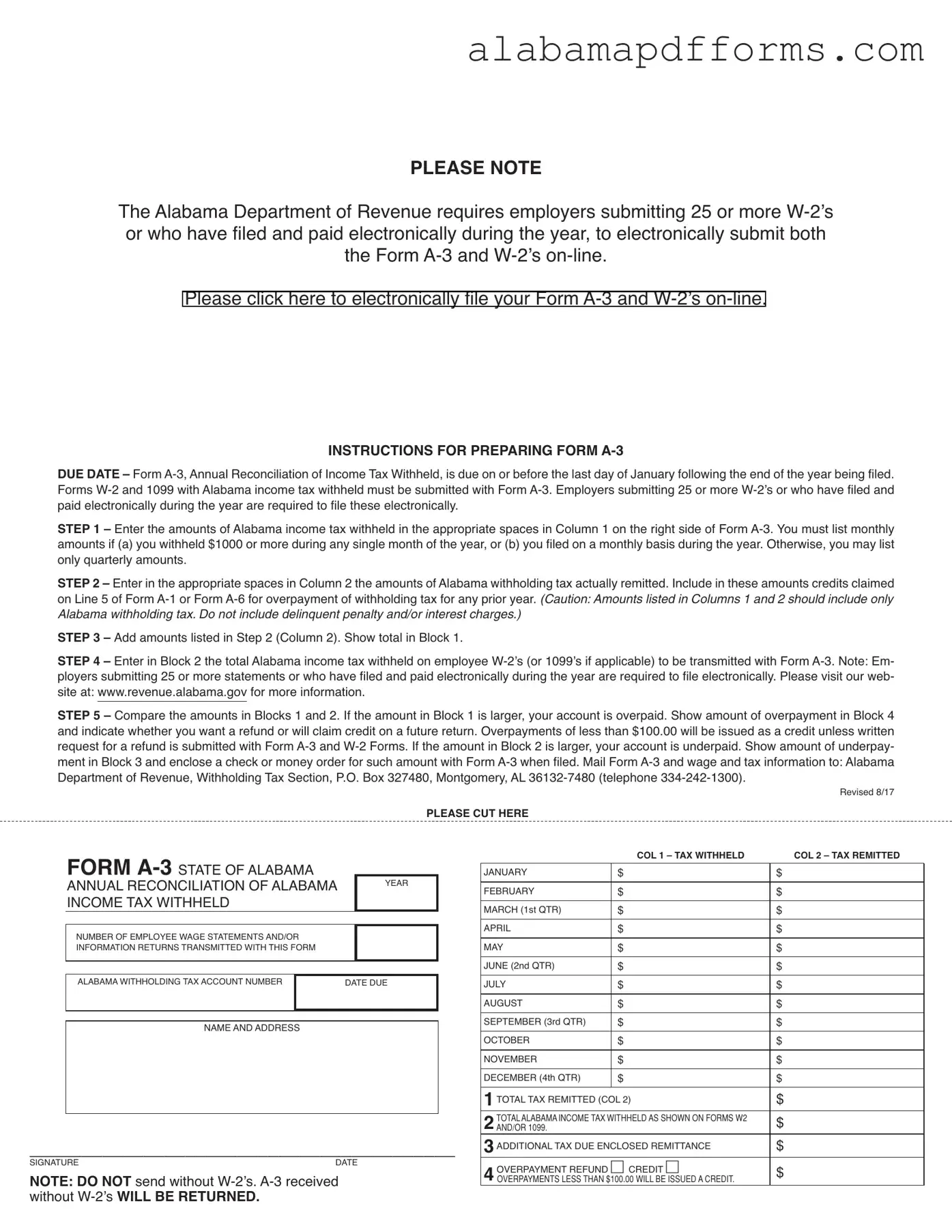

The A-3 Alabama form plays a crucial role in the annual reconciliation process for employers in the state. This form, officially titled the Annual Reconciliation of Income Tax Withheld, is essential for ensuring that the income tax withheld from employees is accurately reported and reconciled with what has been remitted to the state. Employers who have withheld Alabama income tax from their employees are required to submit this form, along with Forms W-2 and 1099, by the end of January each year. For those who have filed 25 or more W-2s or have opted for electronic filing and payment during the year, electronic submission of both the A-3 and the W-2s is mandatory. The form requires employers to detail the amounts of Alabama income tax withheld and remitted throughout the year, including a comparison of these figures to determine if there are any overpayments or underpayments. It also provides a structured process for addressing any discrepancies, allowing employers to either request a refund for overpayments or remit additional payments for underpayments. Understanding the A-3 form is vital for compliance and to avoid potential penalties, making it an important task for employers as they prepare for the annual tax filing season.

This is not true. The Alabama Department of Revenue requires that the A-3 form be submitted along with the corresponding W-2s. If W-2s are missing, your A-3 will be returned.

While employers with 25 or more W-2s or those who have filed electronically during the year must file electronically, any employer can choose to file electronically for convenience.

The due date is strict. Form A-3 must be submitted by the last day of January following the end of the year being filed. Missing this deadline can lead to penalties.

Only Alabama withholding tax should be reported. Delinquent penalties and interest charges should not be included in the amounts listed.

Overpayments of less than $100 will be credited unless you request a refund in writing. Be sure to indicate your preference in Block 4 of the A-3 form.

It's essential to compare the totals in Blocks 1 and 2. If Block 1 is larger, you have an overpayment. If Block 2 is larger, you owe additional tax. Failing to do this can lead to complications.

The A-3 form is an annual reconciliation and must be submitted by the designated due date. Timely submission is crucial for compliance.

For those required to file, the A-3 form is mandatory. Employers must ensure they comply with all filing requirements to avoid penalties.

PLEASE NOTE

The Alabama Department of Revenue requires employers submitting 25 or more

Please click here to electronically file your Form

INSTRUCTIONS FOR PREPARING

STEP1 – Enter the amounts of Alabama income tax withheld in the appropriate spaces in Column 1 on the right side of Form

STEP3 – Add amounts listed in Step 2 (Column 2). Show total in Block 1.

STEP4 – Enter in Block 2 the total Alabama income tax withheld on employee

STEP5 – Compare the amounts in Blocks 1 and 2. If the amount in Block 1 is larger, your account is overpaid. Show amount of overpayment in Block 4 and indicate whether you want a refund or will claim credit on a future return. Overpayments of less than $100.00 will be issued as a credit unless written request for a refund is submitted with Form

Revised 8/17

PLEASE CUT HERE

|

|

ANNUAL RECONCILIATION OF ALABAMA |

YEAR |

|

|

INCOME TAX WITHHELD |

|

NUMBER OF EMPLOYEE WAGE STATEMENTS AND/OR

INFORMATION RETURNS TRANSMITTED WITH THIS FORM

ALABAMA WITHHOLDING TAX ACCOUNT NUMBER |

DATE DUE |

|

|

NAME AND ADDRESS

_________________________________________

SIGNATURE DATE

NOTE: DO NOT send without

without

|

COL1 – TAX WITHHELD |

COL2 – TAX REMITTED |

|

|

|

JANUARY |

$ |

$ |

|

|

|

FEBRUARY |

$ |

$ |

|

|

|

MARCH (1st QTR) |

$ |

$ |

|

|

|

APRIL |

$ |

$ |

|

|

|

MAY |

$ |

$ |

|

|

|

JUNE (2nd QTR) |

$ |

$ |

|

|

|

JULY |

$ |

$ |

|

|

|

AUGUST |

$ |

$ |

|

|

|

SEPTEMBER (3rd QTR) |

$ |

$ |

|

|

|

OCTOBER |

$ |

$ |

|

|

|

NOVEMBER |

$ |

$ |

|

|

|

DECEMBER (4th QTR) |

$ |

$ |

|

|

|

1TOTAL TAX REMITTED (COL 2) |

$ |

|

|

|

|

2AND/ORTOTAL ALABAMA1099. INCOME TAX WITHHELD AS SHOWN ON FORMS W2 |

$ |

|

3ADDITIONAL TAX DUE ENCLOSED REMITTANCE |

$ |

|

|

|

|

4OVERPAYMENT REFUND CREDIT |

$ |

|

OVERPAYMENTS LESS THAN $100.00 WILL BE ISSUED A CREDIT. |

|

|

Alabama Court Forms - The CS-22 form is a legal document issued by an Alabama court.

The use of a West Virginia Hold Harmless Agreement form is crucial for parties engaging in activities where liabilities may arise, as it explicitly outlines the responsibilities and protections in place. By signing this document, one can ensure that they are safeguarded against potential claims, allowing for smoother operations and peace of mind. For more detailed information, you can refer to the Hold Harmless Agreement guidelines available online.

Alabama Drivers License Division - This report also notes road conditions at the time of the accident.

Alabama Form 40 2023 - The application reflects the estate's responsibility to the state regarding taxes due.

The Alabama Form A-3 is similar to the IRS Form 941, which is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Both forms require employers to reconcile the amounts withheld against what has been remitted to the government. While Form A-3 focuses specifically on Alabama state income tax withheld, Form 941 covers federal taxes. Both forms must be filed periodically, and they require accurate reporting of withheld amounts to ensure compliance with tax obligations.

Another document comparable to the A-3 is the IRS Form W-3, which serves as a transmittal form for W-2s. Employers use Form W-3 to summarize total wages, tips, and other compensation paid to employees, along with the total amount of federal income tax withheld. Similar to the A-3, Form W-3 must be submitted alongside individual W-2 forms. Both documents are essential for reconciling employee earnings and tax withholdings, ensuring that the reported figures align with what has been withheld throughout the year.

For property owners in North Carolina, it is crucial to understand the benefits of using the Transfer-on-Death Deed form, which allows for the seamless transfer of real estate to beneficiaries upon death, eliminating the need for probate. This method ensures that property is passed on according to the owner’s wishes, providing peace of mind to both the owners and their heirs. For further information on the form, visit https://todform.com/blank-north-carolina-transfer-on-death-deed.

The Alabama Form A-3 also shares similarities with the IRS Form 1096, which is a summary form that transmits paper Forms 1099 to the IRS. Employers must complete Form 1096 if they are submitting 1099 forms for independent contractors or other non-employee compensation. Like the A-3, Form 1096 requires accurate reporting of amounts withheld. Both forms play a critical role in ensuring that tax authorities receive complete and accurate information regarding income tax withholdings.

In addition, the A-3 is akin to the IRS Form 944, which is designed for small employers to report annual payroll taxes. While Form A-3 is specific to Alabama state tax withholdings, Form 944 is focused on federal tax obligations. Both forms require employers to reconcile their withholding amounts and ensure that they have properly remitted the correct amounts to the respective tax authorities. They both simplify the reporting process for employers by providing a structured format for summarizing tax withholdings.

The A-3 form is also similar to the IRS Form 1099-MISC, which is used to report payments made to independent contractors and other non-employees. Employers must report any payments made that meet certain thresholds. While the A-3 focuses on employee income tax withholdings, both forms require accurate reporting of amounts to ensure compliance with tax laws. They serve to inform tax authorities of the income distributed and the tax obligations associated with those payments.

Lastly, the A-3 bears resemblance to the Alabama Form A-1, which is used for reporting Alabama withholding tax on a monthly basis. Employers who withhold significant amounts of tax may need to file this form monthly, while the A-3 is an annual reconciliation. Both forms require employers to accurately report withheld amounts and reconcile them against what has been remitted. This ensures that employers maintain compliance with state tax regulations and accurately reflect their withholding activities throughout the year.

Completing the A-3 Alabama form can be a straightforward process, but several common mistakes can lead to complications. One significant error is failing to include all required W-2 forms. The Alabama Department of Revenue mandates that employers must submit W-2 forms alongside the A-3 form. If W-2 forms are missing, the entire submission will be returned, delaying the reconciliation process.

Another frequent mistake involves incorrect entries in the columns for tax withheld and tax remitted. It is essential to enter the amounts accurately in Column 1 and Column 2. For instance, if an employer withheld $1,000 or more in any single month, they must report monthly amounts. Otherwise, only quarterly amounts are permitted. Misreporting these figures can lead to discrepancies and potential penalties.

Employers often overlook the requirement to compare the totals in Blocks 1 and 2. If the total in Block 1 exceeds that in Block 2, it indicates an overpayment. Conversely, if Block 2 is larger, it signifies an underpayment. Failing to conduct this comparison may result in incorrect filings and unnecessary financial consequences.

Additionally, some individuals neglect to sign the form before submission. A missing signature can lead to delays, as the form will not be processed until it is properly signed. This step is crucial and should not be overlooked.

Another common oversight is not specifying the desired action for any overpayment. If an employer indicates an overpayment in Block 4, they must choose whether to request a refund or apply the credit to a future return. Failure to make this selection can cause confusion and may result in the overpayment being automatically credited.

Lastly, some employers may forget to include a check or money order for any underpayment when submitting the form. If Block 3 indicates an additional tax due, it is essential to enclose the payment with the A-3 form. Omitting this payment can lead to further complications and penalties.