Fill Out a Valid Alabama 20C Form

Fill Out a Valid Alabama 20C Form

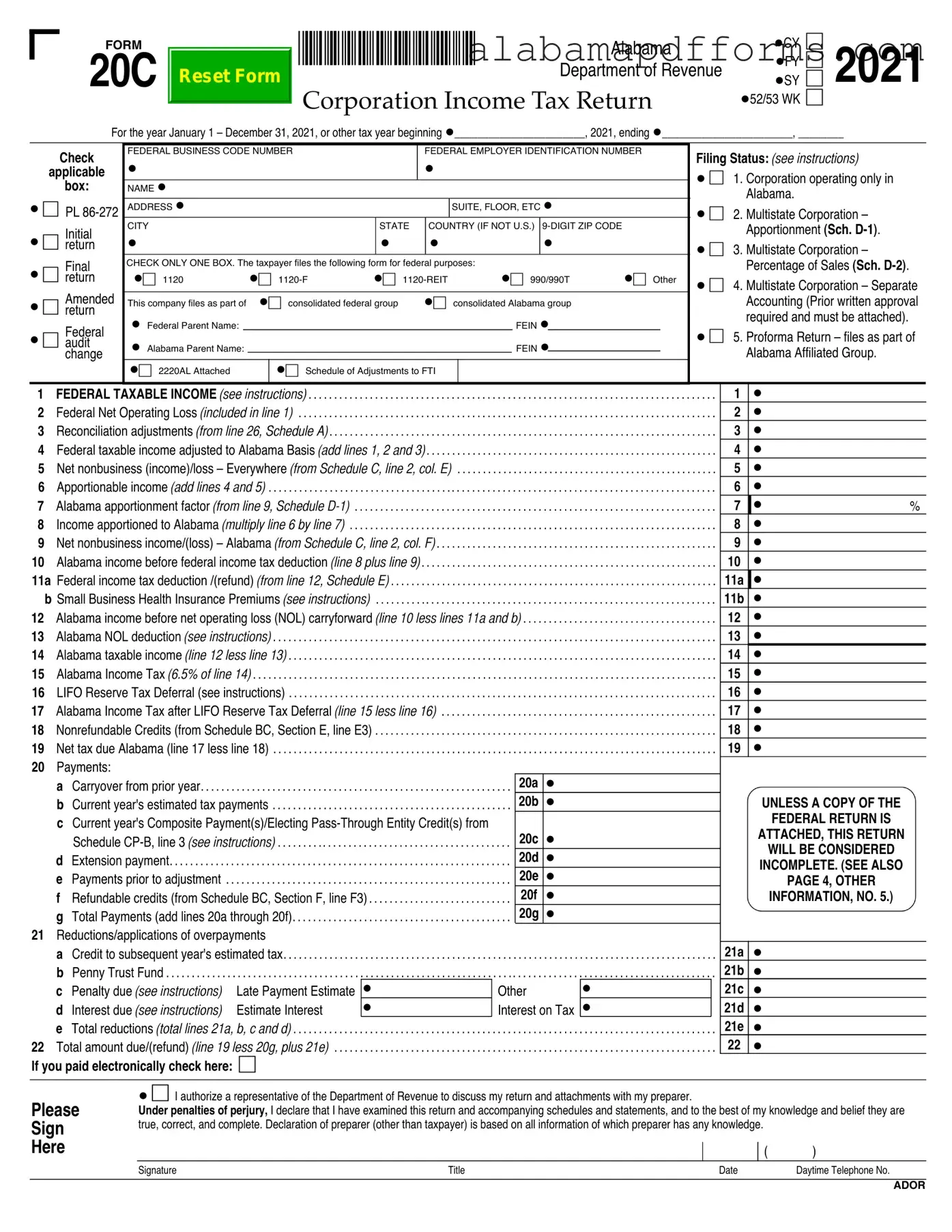

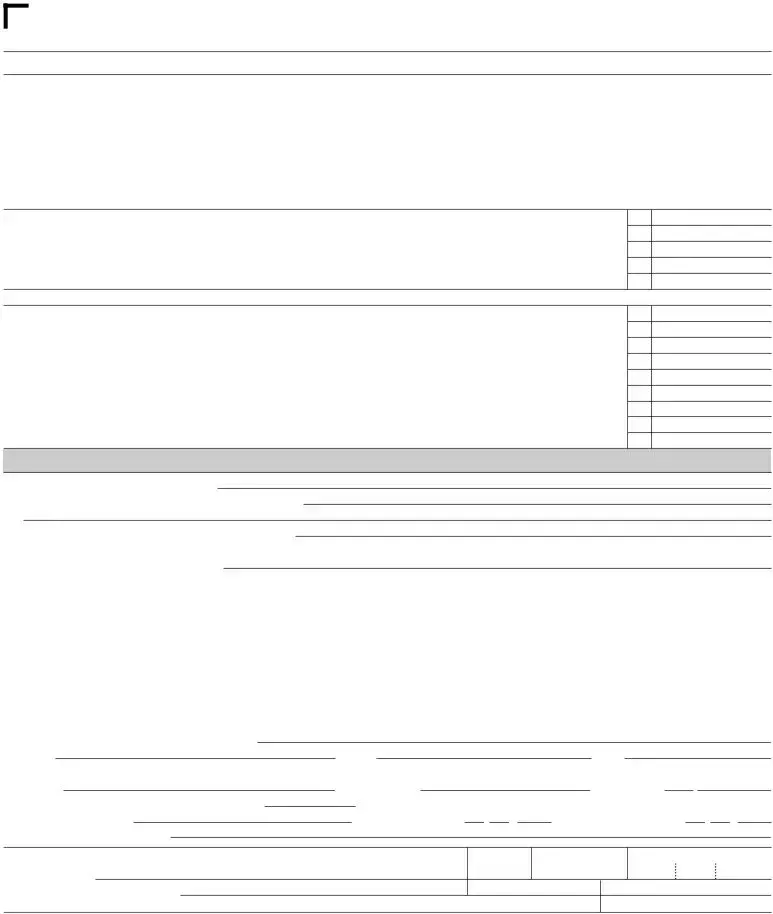

The Alabama 20C form is a crucial document for corporations operating within the state, serving as the Corporation Income Tax Return. This form is designed for various types of corporations, including those solely operating in Alabama and multistate corporations that must apportion their income across different jurisdictions. It covers the tax year from January 1 to December 31, 2010, or any other specified tax year. Corporations must provide essential information such as their federal business code number, employer identification number, and filing status. The form includes sections for reporting federal taxable income, adjustments for Alabama-specific tax regulations, and calculations for apportionable income. Corporations also need to address any net operating loss carryforwards and applicable deductions, including federal income tax deductions. Additionally, the form requires detailed schedules for reconciliation adjustments, allocation of nonbusiness income, and apportionment factors, which are essential for determining the corporation's tax liability in Alabama. Accurate completion of the Alabama 20C form is vital for compliance with state tax laws and for ensuring that corporations meet their tax obligations effectively.

Here are some common misconceptions about the Alabama 20C form, which is used for Corporation Income Tax Returns:

Understanding these misconceptions can help ensure compliance and maximize potential benefits when filing the Alabama 20C form.

FORM

20C

Reset Form

*2100012C* Alabama

Department of Revenue

Corporation Income Tax Return

•CY

•FY

•SY

•52/53 WK

6

6 2021

6

6

For the year January 1 – December 31, 2021, or other tax year beginning •_______________________, 2021, ending •_______________________, ________

Check

applicable

box:

•6 PL

•6 returnInitial

•6 returnFinal

•6 returnAmended

•6 auditFederal change

FEDERAL BUSINESS CODE NUMBER |

|

FEDERAL EMPLOYER IDENTIFICATION NUMBER |

|

Filing Status: (see instructions) |

|||

• |

|

|

• |

|

|

|

|

|

|

|

|

|

• 6 1. Corporation operating only in |

||

NAME • |

|

|

|

|

|

|

|

|

|

|

|

|

|

Alabama. |

|

ADDRESS • |

|

|

|

SUITE, FLOOR, ETC • |

|

|

|

|

|

|

|

|

• 6 2. Multistate Corporation – |

||

CITY |

|

STATE |

COUNTRY (IF NOT U.S.) |

|

|

||

|

|

|

Apportionment (Sch. |

||||

• |

|

• |

• |

• |

|

|

• 6 3. Multistate Corporation – |

CHECK ONLY ONE BOX. The taxpayer files the following form for federal purposes: |

•6 |

|

Percentage of Sales (Sch. |

||||

•6 1120 |

•6 |

•6 |

•6 990/990T |

Other |

• 6 4. Multistate Corporation – Separate |

||

|

|

|

|

|

|

|

|

This company files as part of |

•6 consolidated federal group |

•6 consolidated Alabama group |

|

|

Accounting (Prior written approval |

||

• Federal Parent Name: |

|

|

|

FEIN • |

|

|

required and must be attached). |

|

|

|

|

|

• 6 5. Proforma Return – files as part of |

||

• Alabama Parent Name: |

|

|

|

FEIN • |

|

|

|

|

|

|

|

|

Alabama Affiliated Group. |

||

|

|

|

|

|

|

|

|

•6 2220AL Attached |

•6 Schedule of Adjustments to FTI |

|

|

|

|

||

1 |

FEDERAL TAXABLE INCOME (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

2 |

Federal Net Operating Loss (included in line 1) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

3 |

Reconciliation adjustments (from line 26, Schedule A) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

4 |

Federal taxable income adjusted to Alabama Basis (add lines 1, 2 and 3) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

5 |

Net nonbusiness (income)/loss – Everywhere (from Schedule C, line 2, col. E) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

6 Apportionable income (add lines 4 and 5) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

7 |

Alabama apportionment factor (from line 9, Schedule |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

8 |

Income apportioned to Alabama (multiply line 6 by line 7) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

9 |

Net nonbusiness income/(loss) – Alabama (from Schedule C, line 2, col. F) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

10 |

Alabama income before federal income tax deduction (line 8 plus line 9) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

11a Federal income tax deduction /(refund) (from line 12, Schedule E) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

|

b Small Business Health Insurance Premiums (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

12 |

Alabama income before net operating loss (NOL) carryforward (line 10 less lines 11a and b) . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

13 |

Alabama NOL deduction (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

14 |

Alabama taxable income (line 12 less line 13) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

15 |

Alabama Income Tax (6.5% of line 14) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

16 LIFO Reserve Tax Deferral (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

17 |

Alabama Income Tax after LIFO Reserve Tax Deferral (line 15 less line 16) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

18 |

Nonrefundable Credits (from Schedule BC, Section E, line E3) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

19 |

Net tax due Alabama (line 17 less line 18) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

20 |

Payments: |

20a |

|

|

|

a |

Carryover from prior year |

• |

|

|

20b |

|||

|

b |

Current year's estimated tax payments |

• |

|

|

|

|||

cCurrent year's Composite Payment(s)/Electing

|

Schedule |

|

20c |

• |

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . 20d |

|

|||

d |

Extension payment |

|

|

• |

|

|

. . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . 20e |

|

|||

e Payments prior to adjustment |

|

|

• |

|

||

. . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . 20f |

|

|||

f Refundable credits (from Schedule BC, Section F, line F3) |

• |

|

||||

. . . 20g |

|

|||||

g Total Payments (add lines 20a through 20f) |

|

• |

|

|||

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . |

|

||||

21 Reductions/applications of overpayments |

|

|

|

|

||

a Credit to subsequent year's estimated tax |

. . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|||

b |

Penny Trust Fund |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . .. . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

c |

Penalty due (see instructions) |

Late Payment Estimate |

• |

Other |

|

• |

d |

Interest due (see instructions) |

Estimate Interest |

• |

Interest on Tax |

• |

|

e Total reductions (total lines 21a, b, c and d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

22 Total amount due/(refund) (line 19 less 20g, plus 21e) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If you paid electronically check here: 6

1•

2•

3•

4•

5•

6•

7 • |

% |

8•

9•

10•

11a •

11b •

12•

13•

14•

15•

16•

17•

18•

19•

UNLESS A COPY OF THE

FEDERAL RETURN IS

ATTACHED, THIS RETURN

WILL BE CONSIDERED

INCOMPLETE. (SEE ALSO

PAGE 4, OTHER

INFORMATION, NO. 5.)

21a •

21b •

21c •

21d •

21e •

22•

Please

Sign

Here

•6 I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

|

|

( |

) |

Signature |

Title |

Date |

Daytime Telephone No. |

ADOR

*2100022C* |

PAGE 2 |

ALABAMA 20C – 2021 |

|

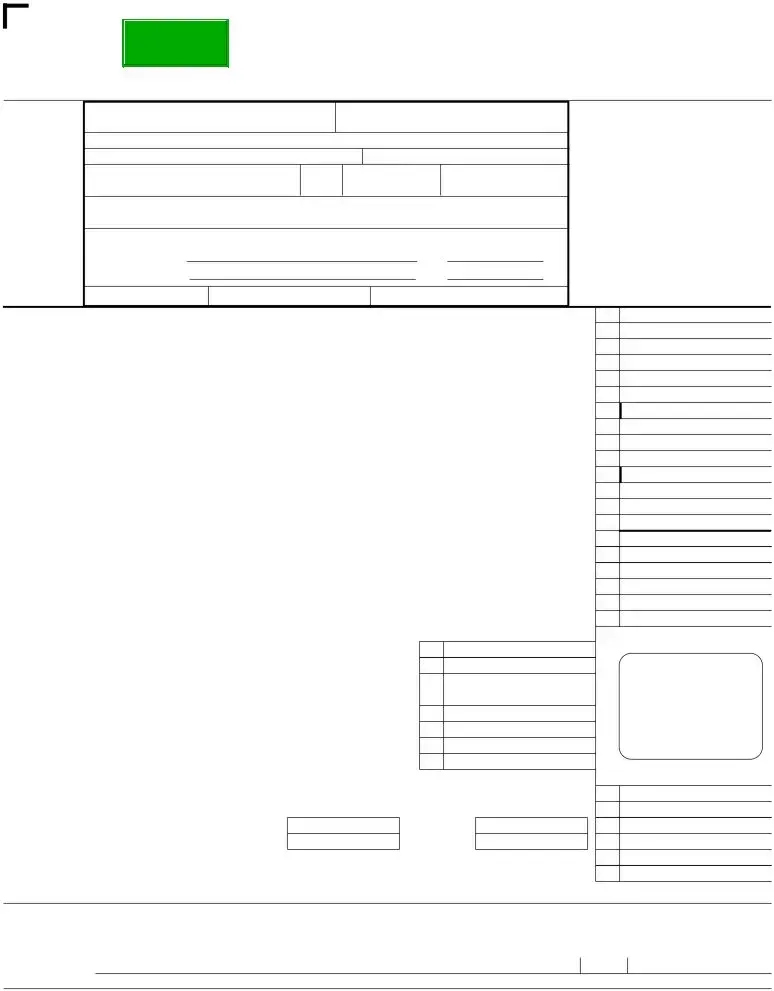

Schedule A Reconciliation Adjustments of Federal Taxable Income to Alabama Taxable Income |

|

ADDITIONS

1 |

State and local income taxes |

1 |

• |

2 |

Federal exempt interest income (other than Alabama) on state, county and municipal obligations (everywhere) |

2 |

• |

3Dividends from corporations in which the taxpayer owns less than 20 percent of stock to the extent properly deducted on

|

federal income tax return (see instructions) |

3 |

• |

4 |

Federal depreciation on pollution control items previously deducted for Alabama (see instructions) |

4 |

• |

5 |

Net income from foreclosure property pursuant to |

5 |

• |

6Related members interest or intangible expenses or costs. From Schedule AB (see instructions).

|

Total Payments 6a • |

minus Exempt Amount 6b • |

equals 6c |

• |

7 |

Captive REITS: Dividends Paid Deduction (from federal Form |

. . . . . . 7 |

• |

|

8 |

Contributions not deductible on state income tax return due to election to claim state tax credit |

. . . . . 8 |

• |

|

9 |

• |

|

9 |

• |

10 |

• |

|

10 |

• |

11 |

Total additions (add lines 1 through 10) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . 11 |

• |

DEDUCTIONS

12 |

Refunds of state and local income taxes (due to overpayment or over accrual on the federal return) |

12 |

• |

13 |

Interest income earned on direct obligations of the United States |

13 |

• |

14Interest income earned on obligations of Alabama or its subdivisions or instrumentalities to extent included in

|

federal income tax return (see instructions) |

14 |

• |

15 |

Aid or assistance provided to the Alabama State Industrial Development Authority pursuant to |

15 |

• |

16 |

Expenses not deductible on federal income tax return due to election to claim a federal tax credit |

16 |

• |

17 |

Dividends described in 26 U.S.C. §78 from corporations in which taxpayer owns more than 20% of stock (see instructions) |

17 |

• |

18Dividend income – more than 20% stock ownership (including that described in 26 U.S.C. §951) from

|

corporations to the extent the dividend income would be deductible under 26 U.S.C. §243 if received from domestic corporations. . . . |

18 |

• |

19 |

Dividends received from foreign sales corporations as determined in 26 U.S.C. §922 (see instructions) |

19 |

• |

20 |

Amount of the oil/gas depletion allowance provided by |

20 |

• |

21 |

Additional Alabama depreciation related to Economic Stimulus Act of 2008 (see instructions) |

21 |

• |

22 |

Exemption of gain under |

22 |

• |

23 |

• |

23 |

• |

24 |

• |

24 |

• |

25 |

Total deductions (add lines 12 through 24) |

25 |

• |

26TOTAL RECONCILIATION ADJUSTMENTS (subtract line 25 from line 11 above).

|

Enter here and on line 3, page 1 (enclose a negative amount in parentheses) |

26 • |

|

||||||

|

Schedule B |

|

Alabama Net Operating Loss Carryforward Calculation |

|

|

||||

|

Column 1 |

Column 2 |

Column 3 |

|

Column 4 |

Column 5 |

Column 6 |

||

|

Loss Year End |

Amount of Alabama |

Amount used in years |

|

Amount used |

Remaining unused |

Acquired |

||

|

MM / DD / YYYY |

net operating loss |

prior to this year |

|

this year |

net operating loss |

NOL |

||

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

Alabama net operating loss (enter here and on line 13, page 1). |

• |

|

|

|

|

||||

ADOR

|

*2100032C* |

PAGE 3 |

ALABAMA 20C – 2021 |

||

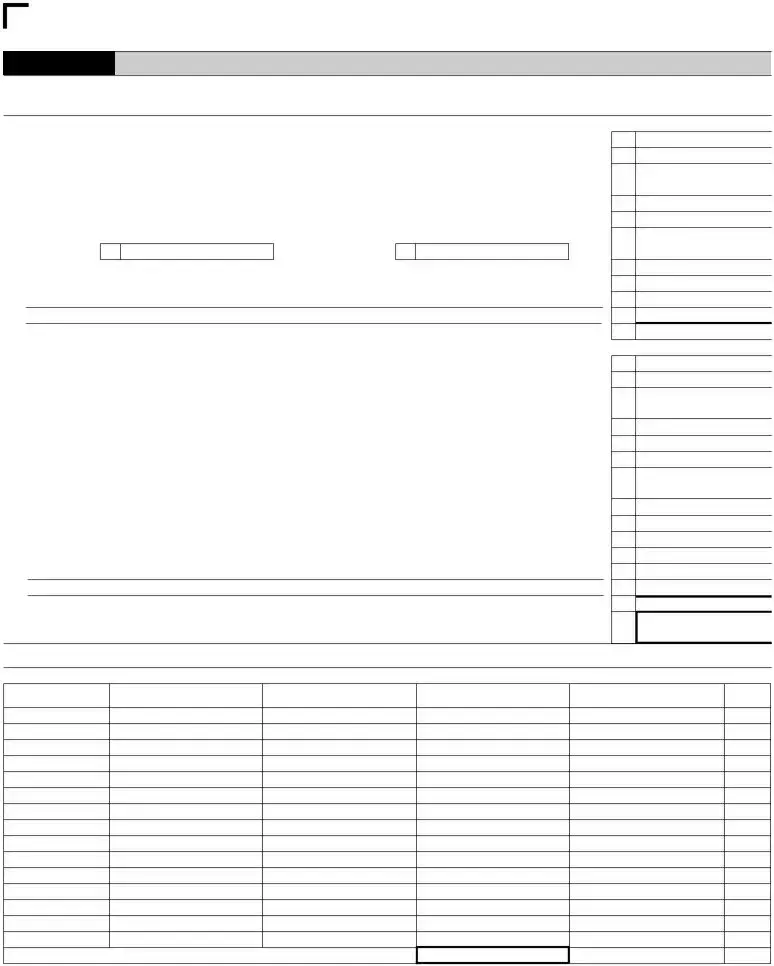

Schedule C |

Allocation of Nonbusiness Income, Loss, and Expense – Use only if you checked Filing Status 2, page 1 |

|

Identify by account name and amount, all items of nonbusiness income, loss and expense removed from apportionable income and those items which are directly allocable to Alabama. Adjustment(s) must also be made for any proration of expenses under Alabama Income Tax Rule

|

ALLOCABLE GROSS INCOME / LOSS |

RELATED EXPENSE |

|

NET OF RELATED EXPENSE |

|||

DIRECTLY ALLOCABLE ITEMS OF |

Column A |

Column B |

Column C |

Column D |

|

Column E |

Column F |

NONBUSINESS INCOME OR LOSS |

Everywhere |

Alabama |

Everywhere |

Alabama |

|

Everywhere |

Alabama |

1a • |

• |

• |

• |

• |

• |

|

• |

b • |

• |

• |

• |

• |

• |

|

• |

c • |

• |

• |

• |

• |

• |

|

• |

d • |

• |

• |

• |

• |

• |

|

• |

e • |

• |

• |

• |

• |

• |

|

• |

2 NET NONBUSINESS INCOME / LOSS |

Column E |

Column F |

|

Enter Column E total ((income)/loss) on line 5 of page 1. Enter Column F total (income/(loss)) on line 9 of page 1 |

• |

• |

|

|

|

|

|

Schedule |

Apportionment Factor – Use only if Filing Status 2 or Filing Status 5, page 1 with |

|

|

Amounts must be Positive (+) Values |

|

|

|

|

|

SALES |

|

|

ALABAMA |

EVERYWHERE |

1 |

Gross receipts from sales |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

2 |

Dividends |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

3 |

Interest |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

4 |

Rents |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

5 |

Royalties |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

6 |

Gross proceeds from capital and ordinary gains . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

7 |

Other • |

|

(Federal 1120, line • |

) • |

|

• |

8 |

Total Sales |

. . 8a • |

|

8b • |

||

9 |

Line 8a/8b = ALABAMA APPORTIONMENT FACTOR (Enter here and on line 7, page 1) . . |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . |

|||

|

Schedule |

Percentage of Sales – Use only if you checked Filing Status 3, page 1 – See instructions |

||||

9

•

%

DO NOT USE THIS SCHEDULE IF ALABAMA SALES EXCEED $100,000. |

ALABAMA |

EVERYWHERE |

|

1 |

Gross receipts from sales |

• |

• |

2 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Tax due (multiply line 1, Alabama by .0025) (enter here and on page 1, line 15) |

• |

|

ADOR

|

*2100042C* |

PAGE 4 |

ALABAMA 20C – 2021 |

||

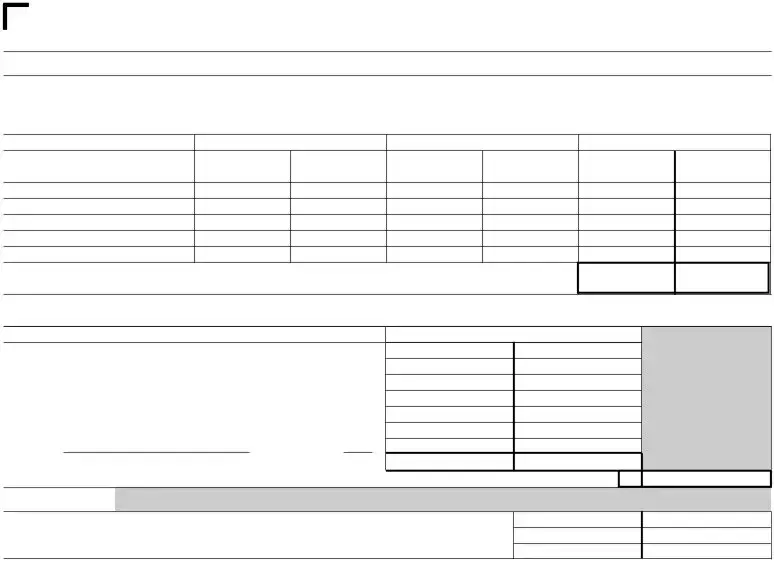

Schedule E |

Federal Income Tax (FIT) Deduction/(Refund) |

|

Only method 1552(a)(1) can be used to calculate the Federal Income Tax Deduction.

(a)If this corporation is an

(b)If this corporation is a

enter the amount of federal income tax paid during the year.

(c)If this corporation is a member of an affiliated group which files a consolidated federal return, enter the separate company income from line 30 of the proforma 1120 for this company on line 1. You must complete lines

Items excluded from Alabama Taxable Income must be added to adjusted total income on line 8b to calculate the Federal Income Tax deduction. (This includes any amounts listed on Schedule A lines 13, 14, 17, 18, and 19).

1 |

This company’s separate federal taxable income |

1 |

• |

|

2 |

Total positive consolidated federal taxable income |

2 |

• |

|

3 |

This company’s percentage (divide line 1 by line 2) |

3 |

• |

% |

4 |

Consolidated federal income tax (liability/payment) |

4 |

• |

|

5 |

Federal income tax for this company (multiply line 3 by line 4) |

5 |

• |

|

6 |

Federal income tax to be apportioned |

6 |

• |

|

7 |

Alabama income, page 1, line 10 |

7 |

• |

|

8a Adjusted total income, page 1, line 4 |

8a • |

|

||

8b Income excluded from Alabama Taxable Income (include any amounts listed on Schedule A lines 13, 14, 17, 18, and 19) |

8b • |

|

||

8c Adjusted Total Income including items excluded from Alabama Taxable Income (Add lines 8a and 8b) |

8c |

• |

|

|

9 |

Federal income tax ratio (divide line 7 by line 8c) |

9 |

• |

% |

10 |

Federal income tax apportioned to Alabama (multiply line 6 by line 9) |

10 |

• |

|

11 |

Less refunds or adjustments |

11 |

• |

|

12 Net federal income tax deduction / <refund> (enter here and on Page 1, line 11a) |

12 |

• |

|

|

Other Information

1.Briefly describe your Alabama operations. •

2.List locations of property within Alabama (cities and counties). •

3.List other states in which corporation operates, if applicable. •

4.Indicate your tax accounting method:

• 6 Accrual • 6 Cash • 6 Other •

5.If this corporation is a member of an affiliated group which files a consolidated federal return, the following information must be provided:

(a)Copy of Federal Form 851, Affiliations Schedule. Identify by asterisk or underline the names of those corporations subject to tax in Alabama.

(b)Signed copy of consolidated Federal Form 1120, pages

(c)Copy of the spreadsheet of income statements; all supporting schedules for all legal entities that file as part of the consolidated federal group including (but not limited to) a copy of the spreadsheet of income statements (which includes a separate column that identifies the eliminations and adjustments used in completing the federal consolidated return), beginning and ending balance sheets, Schedule

(d)Copy of federal Schedule

(e)Copy of federal Schedule(s) UTP.

6.Enter this corporation’s federal net income (see instructions for page 1, line 1) for the last three (3) years, as last determined (e.g.: per amended federal return or IRS audit).

|

2020 •___________________ |

2019 •_________________ 2018 •___________________ |

|

|

|

|

|

|

7. |

Check if currently being audited by the IRS. • 6 If so, enter the periods: •________________________________________________ |

|

|

|||||

8. |

Location of the corporate records: |

Street address: • |

|

|

|

|

|

|

|

City: • |

|

State: • |

|

|

ZIP: • |

|

|

9. |

Person to contact for information concerning this return: |

|

|

|

|

|

||

|

Name: • |

|

Email Address: • |

|

|

Telephone: • ( |

) |

|

10. |

Files Business Privilege Tax Return. • 6 |

FEIN: • |

/ |

/ |

|

/ |

/ |

|

11. |

State of Incorporation: • |

|

Date of Incorporation: • |

Date Qualified in Alabama: • |

||||

Nature of business in Alabama: •

Paid

Preparer’s

Use Only

Preparer’s signature

Firm’s name (or yours, |

• |

|

if |

• |

|

and address |

|

|

Date |

|

Preparer’s Tax Identification Number |

• |

Check if |

•6 • |

Tel. No. • ( |

) |

E.I. No. • |

|

|

ZIP Code • |

ADOR

ALABAMA 20C – 2021 |

|

PAGE 5 |

|

Alabama Department of Revenue |

Payment returns, mail with |

Alabama Department of Revenue |

|

mail to: |

Income Tax Administration Division |

payment voucher (Form |

Income Tax Administration Division |

|

Corporate Tax Section |

|

Corporate Tax Section |

|

PO Box 327430 |

|

PO Box 327435 |

|

Montgomery, AL |

|

Montgomery, AL |

Federal audit change |

|

|

|

returns, mail to: |

Alabama Department of Revenue |

|

|

|

Income Tax Administration Divisionn |

|

|

|

Corporate Tax Section |

|

|

PO Box 327451

Montgomery, AL

ADOR

Alabama Mvt 41 1 - The Alabama MVT 41 1 form is used to apply for a salvage certificate of title.

Alabama Environment - Completing the form correctly can prevent misunderstandings or disputes regarding patient care.

For those navigating estate planning, a vital resource is the appropriate Last Will and Testament form template, which helps ensure that your wishes are acknowledged and followed after your passing.

Alabama Incident Offense Report - A hate crime reported against a local community member.

The Alabama 20C form is similar to the IRS Form 1120, which is the U.S. Corporation Income Tax Return. Both forms are used by corporations to report their income, deductions, and tax liability to the respective tax authorities. The IRS Form 1120 requires detailed information about a corporation's financial activities, similar to how the Alabama 20C captures income and deductions specific to Alabama. Both forms also require the calculation of taxable income and the application of tax rates to determine the amount owed or refunded.

Another document that shares similarities with the Alabama 20C is the IRS Form 1120-S, used by S corporations. Like the 20C, the Form 1120-S allows for the reporting of income, deductions, and credits, but it is specifically tailored for S corporations that pass income directly to shareholders. Both forms require detailed income reporting and adjustments to arrive at the taxable income, although the 1120-S includes specific provisions for pass-through taxation that do not apply to the 20C.

The Alabama 20C form is also comparable to the state-specific forms used in other states, such as the California Form 100. Each state has its own corporate income tax return that aligns with its tax laws. Similar to the Alabama 20C, California's Form 100 requires corporations to report their income, calculate their tax liability, and provide necessary schedules and attachments. Both forms aim to ensure that corporations comply with state tax regulations and accurately report their financial activities.

Additionally, the Alabama 20C form resembles the IRS Form 1065, which is used for partnerships. Both forms require the reporting of income and deductions, although the 1065 is designed for pass-through entities where income is reported on individual partners' tax returns. The structure of both forms includes schedules for detailing income sources and adjustments, ensuring that the tax authorities receive comprehensive financial information.

In the realm of corporate taxation, understanding liability is crucial, which is why documents like the Hold Harmless Agreement come into play. This agreement outlines the responsibilities of parties involved in business transactions, mitigating potential risks and liabilities that may arise during operations. Just as other state-specific tax forms provide clarity in reporting obligations, a Hold Harmless Agreement protects parties by clearly defining responsibilities and expectations, ensuring a smoother transaction process.

Finally, the Alabama 20C is similar to the IRS Form 990, which is filed by tax-exempt organizations. While the 20C focuses on corporate income taxation, both forms require detailed financial disclosures, including income, expenses, and changes in net assets. They both serve to inform the respective tax authorities about the financial health of the organization, albeit for different types of entities, ensuring compliance with tax obligations and transparency in financial reporting.

Filling out the Alabama 20C form can be a daunting task, and many individuals make common mistakes that can lead to delays or issues with their tax filings. One frequent error is failing to provide the correct Federal Employer Identification Number (FEIN). This number is crucial for identifying the corporation and ensuring that the tax return is processed accurately. Omitting this information or entering it incorrectly can result in significant complications, including penalties or additional scrutiny from the Alabama Department of Revenue.

Another mistake often encountered is related to the filing status. The form has specific checkboxes for different statuses, such as initial, final, or amended returns. Many people neglect to select the appropriate filing status, which can lead to confusion about the nature of the return. It is essential to read the instructions carefully and ensure that the correct box is checked to avoid unnecessary complications.

Moreover, taxpayers frequently miscalculate the Alabama apportionment factor. This factor is used to determine the income that is subject to Alabama tax. Errors can arise from incorrect figures in the Schedule D-1, which details property, payroll, and sales. These calculations require precise data and can be complex, so double-checking the numbers and ensuring they align with the supporting documentation is vital to prevent misreporting.

Lastly, individuals sometimes overlook the requirement to attach a copy of their federal return. The instructions explicitly state that the Alabama return will be considered incomplete without this attachment. Failing to include it can lead to delays in processing and potential penalties. Always ensure that all necessary documents are included when submitting the return to avoid these pitfalls.