Fill Out a Valid Alabama 20S Form

Fill Out a Valid Alabama 20S Form

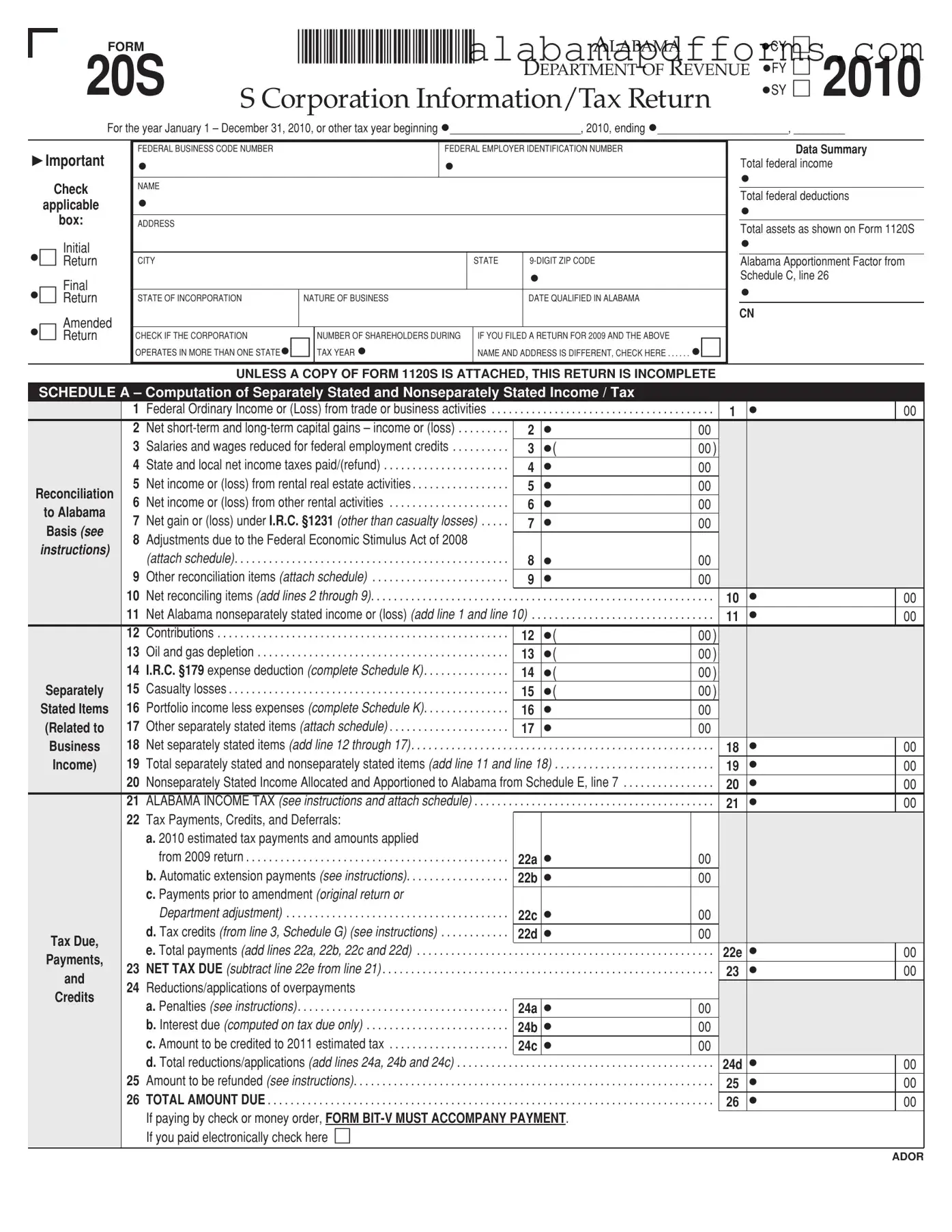

The Alabama 20S form is an essential document for S corporations operating within the state, serving as a comprehensive tax return that outlines the corporation's income, deductions, and tax liabilities for a specific tax year. This form is crucial for ensuring compliance with Alabama tax laws and is used to report various financial details, including total federal income, deductions, and apportionment factors. The form is structured to include sections for calculating both separately stated and nonseparately stated income, allowing corporations to accurately report their earnings and any adjustments required under Alabama tax regulations. Additionally, the Alabama 20S form requires information about the corporation's operations, such as its nature of business, the number of shareholders, and whether it operates in multiple states. Proper completion of this form not only helps in determining the state income tax owed but also ensures that corporations can claim any eligible tax credits and deductions. Filing this form accurately is vital for S corporations to maintain their status and avoid potential penalties, making it a key component of their annual tax obligations.

Misconception 1: The Alabama 20S form is only for corporations operating solely in Alabama.

This is incorrect. The Alabama 20S form is applicable to S corporations operating in multiple states as well. If a corporation conducts business in more than one state, it must complete the apportionment factor section of the form to allocate income appropriately.

Misconception 2: Filing the Alabama 20S form is optional for S corporations.

In reality, S corporations must file the Alabama 20S form if they have income derived from Alabama sources. Failure to file can result in penalties and interest on any taxes owed.

Misconception 3: The Alabama 20S form does not require any attachments.

This is misleading. The form requires several attachments, including a copy of the Federal Form 1120S. Incomplete submissions may delay processing and lead to additional inquiries from the Alabama Department of Revenue.

Misconception 4: All income reported on the Alabama 20S form is subject to Alabama state tax.

This is not accurate. Certain types of income, such as nonbusiness income, may be allocated differently. The form includes sections for separately stated items that may not be taxed in Alabama.

Misconception 5: Only large S corporations need to file the Alabama 20S form.

All S corporations, regardless of size, must file the Alabama 20S form if they have income from Alabama sources. This requirement applies to small and large entities alike, ensuring compliance with state tax regulations.

FORM |

*1000012S* |

ALABAMA |

•CY |

|

|

|

20S |

|

|

|

|

|

|

|

DEPARTMENT OF REVENUE |

•SY |

2010 |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

•FY |

|

|

|||||||

|

|

|

|

|

S Corporation Information/Tax Return |

|

|

|

|

||||||||||||

|

For the year January 1 – December 31, 2010, or other tax year beginning •_______________________, 2010, ending •_______________________, _________ |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Important |

|

FEDERAL BUSINESS CODE NUMBER |

|

|

FEDERAL EMPLOYER IDENTIFICATION NUMBER |

|

|

|

|

|

|

Data Summary |

||||||||

|

|

• |

|

|

|

• |

|

|

|

|

|

|

|

Total federal income |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Check |

|

NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total federal deductions |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

applicable |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||||

|

box: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets as shown on Form 1120S |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Initial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

• |

Return |

|

CITY |

|

|

|

|

|

STATE |

|

|

|

|

Alabama Apportionment Factor from |

|||||||

|

Final |

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

Schedule C, line 26 |

||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||

Return |

|

STATE OF INCORPORATION |

NATURE OF BUSINESS |

|

|

DATE QUALIFIED IN ALABAMA |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

CN |

|

|

|

|||||||||||

|

Amended |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return |

|

CHECK IF THE CORPORATION |

|

NUMBER OF SHAREHOLDERS DURING |

IF YOU FILED A RETURN FOR 2009 AND THE ABOVE |

|

|

|

|

|

|

|

|

||||||||

|

|

|

OPERATES IN MORE THAN ONE STATE• |

|

TAX YEAR • |

NAME AND ADDRESS IS DIFFERENT, CHECK HERE |

• |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNLESS A COPY OF FORM 1120S IS ATTACHED, THIS RETURN IS INCOMPLETE |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SCHEDULE A – Computation of Separately Stated and Nonseparately Stated Income / Tax |

|

|

|

|

|

|

|

|

|||||||||||||

|

|

1 |

Federal Ordinary Income or (Loss) from trade or business activities . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

1 |

|

• |

|

|

00 |

||||||||

|

|

2 |

Net |

2 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

3 |

. . . . . . . . . .Salaries and wages reduced for federal employment credits |

3 |

•( |

00 ) |

|

|

|

|

|

|

|

||||||||

|

|

4 |

. . . . . . . . . . . . . . . . . . . . . .State and local net income taxes paid/(refund) |

4 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

5 |

Net income or (loss) from rental real estate activities |

|

|

|

|

|

|

|

|

|

|

|

|||||||

Reconciliation |

5 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

6 |

Net income or (loss) from other rental activities |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

to Alabama |

6 |

• |

00 |

|

|

|

|

|

|

|

||||||||||

|

7 |

Net gain or (loss) under I.R.C. §1231 (other than casualty losses) |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

7 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

|

Basis (SEE |

|

|

|

|

|

|

|

|||||||||||||

|

8 |

Adjustments due to the Federal Economic Stimulus Act of 2008 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

INSTRUCTIONS) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

(attach schedule) |

|

|

|

|

|

|

8 |

• |

00 |

|

|

|

|

|

|

|

||

|

|

|

|

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

|

|

|

|

|

|

|

|||||

|

|

9 |

. . . . . . . . . . . . . . . . . . . . . . . .Other reconciliation items (attach schedule) |

9 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

10 |

Net reconciling items (add lines 2 through 9) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

10 |

|

• |

|

|

00 |

|||||||||

|

|

11 |

. .Net Alabama nonseparately stated income or (loss) (add line 1 and line 10) |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

11 |

|

• |

|

|

00 |

||||||||||

|

|

12 |

Contributions . . . |

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

12 |

•( |

00 ) |

|

|

|

|

|

|

|

||

|

|

13 |

. . . . . . . .Oil and gas depletion |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

13 |

•( |

00 ) |

|

|

|

|

|

|

|

|||

|

|

14 |

. . . . . . . . . . . . . . .I.R.C. §179 expense deduction (complete Schedule K) |

14 |

•( |

00 ) |

|

|

|

|

|

|

|

||||||||

|

|

15 |

Casualty losses . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Separately |

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

15 |

•( |

00 ) |

|

|

|

|

|

|

|

||||

|

Stated Items |

16 |

. . . . . . . . . . . . . . .Portfolio income less expenses (complete Schedule K) |

16 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

(Related to |

17 |

Other separately stated items (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

17 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

|

|

18 |

Net separately stated items (add line 12 through 17) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Business |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

18 |

|

• |

|

|

00 |

|||||||||

|

Income) |

19 |

. . . . . . . . . . . . . . . . . . . . . . . .Total separately stated and nonseparately stated items (add line 11 and line 18) |

. . . . |

19 |

|

• |

|

|

00 |

|||||||||||

|

|

20 |

. . . . . . . . . . . .Nonseparately Stated Income Allocated and Apportioned to Alabama from Schedule E, line 7 |

. . . . |

20 |

|

• |

|

|

00 |

|||||||||||

|

|

21 |

ALABAMA INCOME TAX (see instructions and attach schedule) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

21 |

|

• |

|

|

00 |

|||||||

|

|

22 |

Tax Payments, Credits, and Deferrals: |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

a. 2010 estimated tax payments and amounts applied |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

from 2009 return |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

22a |

• |

00 |

|

|

|

|

|

|

|

||

|

|

|

|

. . . . . . . . . . . . . . . . . .b. Automatic extension payments (see instructions) |

22b |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

c. Payments prior to amendment (original return or |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

Department adjustment) . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

22c |

• |

00 |

|

|

|

|

|

|

|

||

|

Tax Due, |

|

|

. . . . . . . . . . . .d. Tax credits (from line 3, Schedule G) (see instructions) |

22d |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

Payments, |

|

|

. . . . . . . . . .e. Total payments (add lines 22a, 22b, 22c and 22d) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

22e |

• |

|

|

00 |

|||||||

|

23 |

NET TAX DUE (subtract line 22e from line 21) |

|

|

|

|

|

23 |

|

• |

|

|

00 |

||||||||

|

and |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

|

|

|

||||||||||||

|

24 |

Reductions/applications of overpayments |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Credits |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

a. Penalties (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

24a |

• |

00 |

|

|

|

|

|

|

|

|||

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . .b. Interest due (computed on tax due only) |

24b |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

c. Amount to be credited to 2011 estimated tax |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

24c |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

d. Total reductions/applications (add lines 24a, 24b and 24c) |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

24d |

• |

|

|

00 |

||||||||

|

|

25 |

. . . . . . . . . . . . . . . . . . . . .Amount to be refunded (see instructions) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

25 |

|

• |

|

|

00 |

|||||||

|

|

26 |

. . . . . .TOTAL AMOUNT DUE |

. . . |

. . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

26 |

|

• |

|

|

00 |

|||

|

|

|

|

If paying by check or money order, FORM |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

If you paid electronically check here |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ADOR |

|

|

*1000022S* |

Page 2 |

|

FORM 20S – 2010 |

|

|

|

|

SCHEDULE B – Allocation of Nonbusiness Income, Loss, and Expense |

|

|

|

|

|

Identify by account name and amount all items of nonbusiness income, loss, and expense removed from apportionable income and those items which are directly allocable to Alabama. Adjustment(s) must also be made for any proration of expenses under Alabama Income Tax Rule

allowable deduction that is applicable to both business and nonbusiness income of the taxpayer shall be prorated to each class of income in determining income subject to tax as provided…” (See instructions).

|

DIRECTLY ALLOCABLE ITEMS |

|

ALLOCABLE GROSS INCOME / LOSS |

|

|

|

RELATED EXPENSE |

|

NET OF RELATED EXPENSE |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

Column A |

|

Column B |

|

|

Column C |

|

Column D |

|

Column E |

|

Column F |

|||

|

|

|

Everywhere |

|

Alabama |

|

|

Everywhere |

|

Alabama |

|

Everywhere |

|

Alabama |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Col. A less Col. C) |

(Col. B less Col. D) |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonseparately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1c |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1d Total (add lines 1a, 1b, and 1c) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

• |

||

Separately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1e |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1f |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1g |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1h Total (add lines 1e, 1f, and 1g) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

• |

||

SCHEDULE C – Apportionment Factor Schedule. Do not complete if entity operates exclusively in Alabama. |

|

|

|||||||||||||||

|

TANGIBLE PROPERTY AT COST FOR |

|

|

ALABAMA |

|

|

|

|

|

EVERYWHERE |

|||||||

|

PRODUCTION OF BUSINESS INCOME |

BEGINNING OF YEAR |

|

END OF YEAR |

|

BEGINNING OF YEAR |

|

END OF YEAR |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Inventories |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Land |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Furniture and fixtures |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Machinery and equipment |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Buildings and leasehold improvements |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||

6 |

IDB/IRB property (at cost) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Government property (at FMV) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

Less Construction in progress (if included) |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||

10 |

Totals |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Average owned property (BOY + EOY ÷ 2) |

|

|

|

• |

|

|

|

|

|

|

|

• |

|

|||

12 |

Annual rental expense |

|

|

• |

x8 = |

• |

|

|

|

• |

|

x8 = |

• |

|

|||

13 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total average property (add line 11 and line 12) |

|

13a |

• |

|

|

|

. . . . . . |

. . . . |

. . . . . . . . . . . . |

13b |

• |

|

||||

14 |

Alabama property factor — 13a ÷ 13b = line 14 |

. |

. . . . . . |

. . . . . . |

. . . . . . . . . . . |

. . . . . . . |

. . . . . |

. . . . . . . |

. . . . |

. . . . . . . . . . . . |

14 |

• |

% |

||||

|

SALARIES, WAGES, COMMISSIONS AND OTHER COMPENSATION |

|

|

15a |

ALABAMA |

|

15b |

EVERYWHERE |

15c |

|

|||||||

|

RELATED TO THE PRODUCTION OF BUSINESS INCOME |

|

|

|

|

|

|

|

|

|

|

|

|

||||

15 |

Alabama payroll factor — 15a ÷ 15b = 15c |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

% |

|||

|

|

|

SALES |

|

|

|

|

ALABAMA |

|

|

EVERYWHERE |

|

|

||||

16 |

Destination sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

17 |

. . . . . . . . . . . . . . . . . . . . . . . .Origin sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

18 |

. . . . .Total gross receipts from sales |

. . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|

19 |

. . . . . . . . . . . . . . . . . . . . . . . .Dividends |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

20 |

. . . . . . . . . . . . . . . . . . . . . . . .Interest |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

21 |

. . . . . . . . . . . . . . . . . . . . . . . .Rents |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

22 |

. . . . . . . . . . . . . . . . . . . . . . . .Royalties |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

23 |

. . . . . . .Gross proceeds from capital and ordinary gains |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

24Other •___________________________________ (Federal 1120S, line •_____ ) •

25 |

Alabama sales factor — 25a ÷ 25b = line 25c |

25a• |

25b• |

|

25c• |

% |

26 |

Sum of lines 14, 15c, and 25c ÷ 3 = ALABAMA APPORTIONMENT FACTOR (Enter here and on line 4, Schedule E, page 3) |

26 |

• |

% |

||

ADOR

*1000032S* |

|

|

FORM 20S – 2010 |

|

Page 3 |

SCHEDULE D – Apportionment of Federal Income Tax |

|

|

1 Enter the federal income tax from Federal Form 1120S |

1 • |

00 |

2Enter the Alabama income from line 7, Schedule E below, if applicable. (If corporation operates

|

exclusively in Alabama, do not complete lines |

|

. . . . . |

. |

. . . . . . . . . . . . . |

. . . . 2 |

• |

00 |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Apportionment of separately stated items |

|

|

|

|

|

|

|

|

x • |

% = 3c |

|

|

|

|

|

||

3 |

|

3a |

|

• |

|

|

3b |

|

• |

00 |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter in line 3a the amount from line 18, Schedule A |

|

|

|

|

Apportionment Factor |

|

|

|

|

|

|

||||||

|

|

|

|

|

(line 26, Schedule C) |

|

|

|

|

|

||||||||

4 |

Separately stated items allocated to Alabama (line 1h, Column F, Schedule B) |

. . . . 4 |

• |

00 |

|

|

|

|||||||||||

5 |

Total (add lines 2, 3c and 4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . . . . |

. |

. . . . . . . . . . . . . |

. . . . 5 |

• |

00 |

|

|

|

||||||

6 |

. . . . . . . . . . . . . . .Adjusted total income (add line 19, Schedule A to line 1h, Column E, Schedule B) |

. . . . 6 |

• |

00 |

|

|

|

|||||||||||

7 |

Federal income tax apportionment factor |

(line 5 divided by line 6) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 7 |

• |

% |

|||||||||

8 |

Federal income tax apportioned to Alabama (multiply line 1 by the percent on line 7) |

|

|

|

|

|

|

|

|

|

||||||||

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 8 |

• |

00 |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SCHEDULE E – Apportionment and Allocation of Income to Alabama |

|

|

|

|

|

|

|

% |

||||||||||

1 |

Net Alabama nonseparately stated income or (loss) from line 11, Schedule A |

. |

. . . . . |

. |

. . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 1 |

• |

00 |

|||||||

2 |

Nonseparately stated (income) or loss treated as nonbusiness income (line 1d, Column E, Schedule B) |

|

|

|

|

|

||||||||||||

|

|

|

|

|

||||||||||||||

|

– please enter income as a negative amount and losses as a positive amount |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 2 |

• |

00 |

||||||||||||

3 |

Apportionable income or (loss) (add line 1 and line 2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

. . . . . . . . . . . |

. |

. . . . . |

. |

. . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 3 |

• |

00 |

||||||||

4 |

Apportionment ratio from line 26, Schedule C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . |

. |

. . . . . |

. |

. . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 4 |

• |

% |

|||||||

5 |

Income or (loss) apportioned to Alabama (multiply amount on line 3 by percent on line 4) |

|

|

|

|

|

|

|

|

|||||||||

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 5 |

• |

00 |

|||||||||||||

6 |

Nonseparately stated income or (loss) allocated to Alabama as nonbusiness income (Column F, line 1d, Schedule B) |

|

|

|

|

|||||||||||||

. . . . 6 |

• |

00 |

||||||||||||||||

7 |

Nonseparately Stated Income Allocated and Apportioned to Alabama (add lines 5 and 6). Also enter this amount on |

|

|

|

|

|||||||||||||

|

line 2, Schedule D; line 20, Schedule A; and line 1, Schedule K |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 7 |

• |

00 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SCHEDULE F – Alabama Accumulated Adjustments Account |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

1 |

Beginning balance (prior year ending balance) . . . |

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 1 |

• |

00 |

||||||

2 |

Net Alabama nonseparately stated income or (loss) (line 11, Schedule A) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 2 |

• |

00 |

|||||||||

3 |

Net separately stated items (line 18, Schedule A) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 3 |

• |

00 |

|||||||

4 |

Federal income tax deduction (line 1, Schedule D) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 4 |

• |

00 |

|||||||||

5 |

Separately stated nonbusiness items (line 1h, Column E, Schedule B) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 5 |

• |

00 |

|||||||||

6 |

Other additions/(reductions) (Do not include tax exempt income and related expenses) |

|

|

|

|

|

|

|

|

|||||||||

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 6 |

• |

00 |

|||||||||||||

7 |

Less distributions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . |

. . . . . |

|

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 7 |

• |

00 |

|||||

8 |

Ending balance (total appropriate lines) . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . |

. . . . . |

|

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 8 |

• |

00 |

|||||

SCHEDULE G – Tax Credits (CAUTION – SEE INSTRUCTIONS) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

1 |

Employer Education Tax Credit |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . . . . . |

|

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

1 |

• |

00 |

||||||

2 |

Coal Credit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . . . . . |

|

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

2 |

• |

00 |

|||||||

3 |

. . . . . . . . . .TOTAL (add lines 1 and 2). Enter here and on line 22d, Schedule A |

. . . . . . |

|

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

3 |

• |

00 |

|||||||||

SCHEDULE H – The Following Information Must Be Entered For This Return To Be Considered Complete |

|

|

||||||||||||||||

1 |

Indicate tax accounting method used: |

• |

|

Cash • |

Accrual |

• |

Other |

|

|

|

|

|

|

|

|

|||

2Briefly describe your Alabama operations: •

3Enter this company’s Alabama Withholding Tax Account No.: •

4Person to contact for information concerning this return:

Name •

Telephone Number • ( |

) |

Email Address |

|

|

|

|

|

5Location of the corporate records: •

6Check if an Alabama business privilege tax return was filed for this entity: •

7If the privilege tax return was filed using a different FEIN, please provide the name and FEIN used to file the return:

FEIN: • |

NAME: |

|

|

|

|

ADOR

*1000042S*

FORM 20S – 2010

SCHEDULE K – Distributive Share Items

1 Alabama Nonseparately Stated Income (Schedule E, line 7) . . . . . .

Separately Stated Items:

2 Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Oil and gas depletion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4 I.R.C. §179 expense deduction

a. Amount allowed on federal Form 1120S . . . . . . . . . . . . . . . . . . . . .

b. Adjustments required . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

c. Amount to be apportioned . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 Casualty losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6 Portfolio income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7 Interest expense related to portfolio income. . . . . . . . . . . . . . . . . . . . .

8 Other expenses related to portfolio income (attach schedule) . . . . .

9 Other separately stated business items (attach explanation) . . . . . .

10 Small business health insurance premiums (attach explanation) . . .

11 Separately stated nonbusiness items (attach schedule) . . . . . . . . . .

12 Composite payment made on behalf of owner/shareholder . . . . . . .

13 U.S. taxes paid (attach explanation) . . . . . . . . . . . . . . . . . . . . . . . . . . .

14 Alabama exempt income (attach explanation) . . . . . . . . . . . . . . . . . . .

Transactions with Owners:

15 Property distributions to owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

|

|

|

|

|

|

Page 4 |

|

|

Federal Amount |

|

Apportionment |

|

Alabama Amount |

|

Enter on Alabama |

|

|

|

|

|

|

||||

|

|

|

|

|

||||

|

|

Factor |

|

|

Schedule |

|

||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

Part III, Line M |

|

• |

|

|

|

|

|

|

Part III, Line S |

|

• |

|

|

|

|

|

|

Part III, Line Z |

|

• |

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

Part III, Line O |

|

• |

|

|

|

|

|

|

Part III, Line W |

|

• |

|

|

|

|

|

|

Part III, Line Q |

|

• |

|

|

|

|

|

|

Part III, Line P |

|

• |

|

|

|

|

|

|

Part III, Line R |

|

• |

|

|

|

|

|

|

Part III, Line T |

|

|

|

|

|

• |

|

|

Part III, Line Y |

|

• |

|

|

|

|

|

|

Part III, Line AA |

|

|

|

|

|

• |

|

|

Part III, Line U |

|

• |

|

|

|

|

|

|

Part III, Line V |

|

• |

|

|

|

|

|

|

Part III, Line AB |

|

• |

|

|

100% |

• |

|

|

Part III, Line X |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

•I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

|

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are |

|||||

Please |

true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|||||

|

|

|

|

|

|

|

Sign |

|

|

|

|

|

|

Signature |

Date |

|

Daytime Telephone No. |

Social Security No. |

||

Here |

|

|||||

|

|

|

|

|

||

of Officer |

|

|

( |

) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

Title |

|

|

|

|

|

|

of Officer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer’s |

Telephone No. |

|

Date |

Preparer’s Social Security No. |

|

|

|

|

|

|

|

|

|

Signature |

•( |

) |

|

• |

• |

|

|

|

|

|

|

|

Paid

Preparer’s

Use Only

Firm’s Name (or yours • if

and address •

Address

E.I. No. •

ZIP Code •

CHECK LIST

HAVE THE FOLLOWING FORMS BEEN ATTACHED TO THE FORM 20S:

ALABAMA SCHEDULE

ALABAMA SCHEDULE NRA (if applicable)

FEDERAL FORM 1120S (entire form as filed with IRS)

FEDERAL FORM 1120S PROFORMA (if applicable)

FORM

Returns without Payments |

Returns with Payments |

||

|

|

|

|

MAIL TO: Alabama Department of Revenue |

MAIL TO: Alabama Department of Revenue |

||

Pass Through Entity |

Pass Through Entity |

||

PO Box 327441 |

PO Box 327444 |

||

Montgomery, AL |

Montgomery, AL |

||

ADOR

Alabama 3 - It provides a comprehensive overview of qualifications, job history, and personal details.

In many scenarios, a Release of Liability form serves as an essential tool to clarify responsibilities and limit potential conflicts, particularly in recreational activities or volunteer programs. Participants are often required to sign such documents after acknowledging the risks involved, which ensures that they enter into these activities with full awareness of their own responsibilities. For those looking to formalize their agreements, utilizing a Hold Harmless Agreement can further enhance protection against potential claims.

Alabama Court Forms - This form must be served to the employer within certain legal requirements.

The Alabama 20S form shares similarities with the IRS Form 1120S, which is used for S corporations at the federal level. Both forms require detailed information about the corporation's income, deductions, and credits. They also include sections for reporting separately stated items, ensuring that shareholders can accurately report their shares of income, deductions, and credits on their personal tax returns. The structure of both forms is designed to facilitate the flow of information from the corporation to the shareholders, making it easier for them to comply with tax obligations.

Another document similar to the Alabama 20S form is the IRS Form 1065, which is used by partnerships. Like the 20S form, the 1065 requires a comprehensive report of income, deductions, and other financial information. Both forms emphasize the importance of passing through income and losses to owners or partners, allowing them to report their share on their individual tax returns. The format and purpose of these forms align closely, as they serve to inform the IRS about the financial activities of pass-through entities.

The Alabama Corporate Income Tax Return, also known as Form 20C, parallels the 20S form in that it is used by corporations to report income and calculate taxes owed to the state. While the 20C is for traditional C corporations, both forms necessitate reporting of income, deductions, and credits. The key difference lies in the tax treatment, as C corporations are taxed at the corporate level, while S corporations pass income through to shareholders. However, the required financial disclosures and structure of both forms exhibit considerable similarities.

For landlords and tenants entering into rental agreements, utilizing a proper Lease Agreement template is essential for defining responsibilities and expectations. To aid in this process, you can find a comprehensive guide on how to prepare a Lease Agreement effectively for your property needs.

The IRS Schedule K-1 (Form 1120S) is another document closely related to the Alabama 20S form. This schedule is used to report each shareholder's share of income, deductions, and credits from an S corporation. Both the K-1 and the 20S form aim to ensure that shareholders receive accurate information for their personal tax returns. The K-1 provides a breakdown of the amounts reported on the 20S, reinforcing the connection between the corporate and individual tax reporting processes.

The Alabama Partnership Income Tax Return (Form 65) is similar to the Alabama 20S form as it also serves pass-through entities. Both forms require detailed reporting of income, deductions, and credits. While the 20S is specific to S corporations, the Form 65 caters to partnerships, yet both emphasize the pass-through nature of their income. The alignment in their reporting requirements reflects the common goal of providing transparency in the financial activities of these entities.

Lastly, the Alabama Individual Income Tax Return (Form 40) is related to the 20S form in that it is where individual shareholders report their income from S corporations. While the 20S form focuses on corporate income and deductions, the Form 40 is designed for individuals to report their share of that income. Both forms work together to ensure that income is taxed appropriately, highlighting the interconnectedness of corporate and individual tax filings in the state of Alabama.

Filling out the Alabama 20S form can be challenging. Many individuals make mistakes that can lead to delays or complications. One common error is failing to include the correct Federal Employer Identification Number (EIN). This number is crucial for identifying your business. If it is incorrect or missing, your return may be considered incomplete, and this could lead to penalties.

Another frequent mistake is not providing accurate information regarding the apportionment factor. This factor is essential for determining how much of your income is taxable in Alabama. Miscalculating or omitting this information can result in incorrect tax liabilities. Always double-check your calculations and ensure that all figures are correctly transcribed from the appropriate schedules.

Many also overlook the requirement to attach supporting documents, such as a copy of Form 1120S. The instructions clearly state that without this attachment, the return is incomplete. Failing to include necessary documents can cause delays in processing your return and may result in additional inquiries from the Alabama Department of Revenue.

Lastly, individuals often forget to sign and date the form. An unsigned return is not valid and will be rejected. Ensure that the officer of the corporation signs the form before submission. Taking these steps can help avoid common pitfalls and ensure a smoother filing process.