Fill Out a Valid Alabama 2100 Form

Fill Out a Valid Alabama 2100 Form

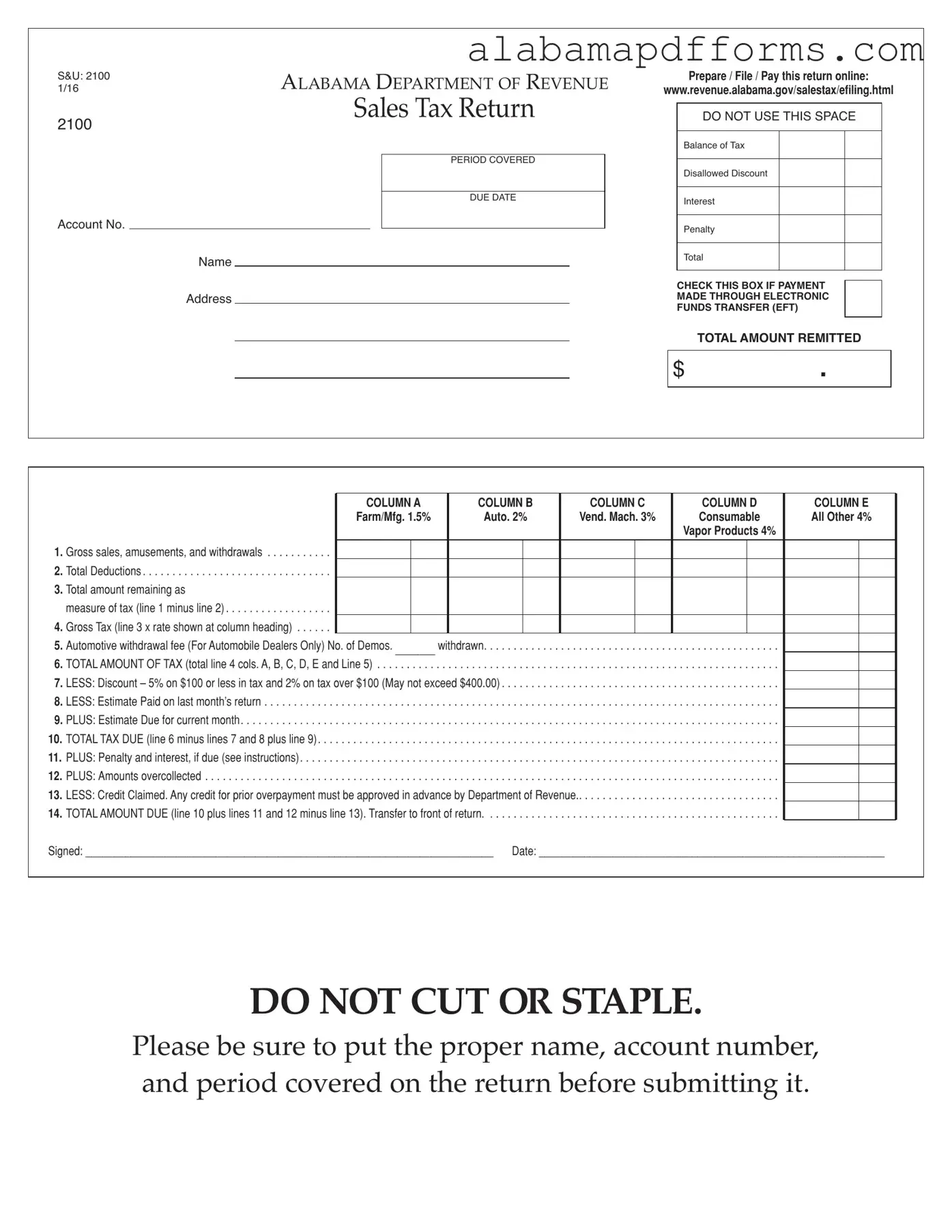

The Alabama 2100 form is a crucial document for businesses operating within the state, serving as the official sales tax return. This form provides a comprehensive overview of a business's gross sales, deductions, and the total amount of tax owed for a specific period. It includes various sections that detail different tax rates applicable to items such as automotive products, vending machines, and consumable goods. The form also allows for adjustments through discounts, estimated payments, and credits for any prior overpayments. Timely submission is essential, as it helps avoid penalties and interest charges, ensuring compliance with Alabama’s tax regulations. Business owners must carefully fill out the form, including their account number and the period covered, to facilitate a smooth filing process. With the option to prepare, file, and pay online, the Alabama 2100 form aims to simplify tax reporting for businesses, making it easier to manage their financial obligations.

There are several misconceptions surrounding the Alabama 2100 form. Understanding these can help ensure accurate filing and compliance with state tax regulations.

This form is applicable to all businesses that are required to report sales tax, regardless of their size. Small businesses also need to file this return.

Calculating the total tax due is essential. The form requires specific calculations based on gross sales and applicable deductions.

Discounts on the Alabama 2100 form have specific rules. For instance, the maximum discount cannot exceed $400, and it varies based on the amount of tax due.

Late submissions can result in penalties and interest charges. It is crucial to file on time to avoid these additional costs.

While the form itself may not require attachments, businesses should maintain documentation of sales and deductions in case of an audit.

Other taxes, such as automotive withdrawal fees, may also need to be reported depending on the nature of the business.

Gross sales must be calculated according to specific guidelines set by the Alabama Department of Revenue. Accurate reporting is essential.

Businesses must register for electronic filing before they can submit the Alabama 2100 form online. This step is crucial for compliance.

If errors are discovered after submission, businesses can file an amended return to correct any mistakes. Timely action is important to avoid penalties.

S&U: 2100 |

AlAbAmA DepArtment of revenue |

|

|

|

Prepare / File / Pay this return online: |

||||||||||||||||||||||

1/16 |

|

|

www.revenue.alabama.gov/salestax/efiling.html |

||||||||||||||||||||||||

|

|

|

|

Sales tax return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

2100 |

|

|

|

|

|

|

|

|

DO NOT USE THIS SPACE |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance of Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PERIOD COVERED |

|

|

|

|

|

|

Disallowed Discount |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DUE DATE |

|

|

|

|

|

|

Interest |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Account No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Penalty |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CHECKTHISBOXIFPAYMENT |

|

|

|

|

|

||||

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MADETHROUGHELECTRONIC |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FUNDSTRANSFER(EFT) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTALAMOUNTREMITTED |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

. |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

COLUMN A |

COLUMN B |

|

COLUMN C |

|

|

|

COLUMN D |

|

COLUMN E |

|

||||||||||||

|

|

|

|

|

Farm/Mfg. 1.5% |

Auto. 2% |

|

Vend. Mach. 3% |

|

|

|

Consumable |

|

All Other 4% |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vapor Products 4% |

|

|

|

|

|

|

|

||

1. |

. .Gross sales, amusements, and withdrawals |

. . . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

2. |

. . . . . . . . . . . . . . . . . . . . . . .Total Deductions |

. . . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3. |

Total amount remaining as |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

measure of tax (line 1 minus line 2) |

. . . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4. |

. . . . . .Gross Tax (line 3 x rate shown at column heading) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

5. |

Automotive withdrawal fee (For Automobile Dealers Only) No. of Demos. _______ withdrawn |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

6. |

TOTAL AMOUNT OF TAX (total line 4 cols. A, B, C, D, E and Line 5) |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||

7. |

. . . . . . . . . . . . . . . . . . . . . . .LESS: Discount – 5% on $100 or less in tax and 2% on tax over $100 (May not exceed $400.00) |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||||

8. |

. . .LESS: Estimate Paid on last month’s return |

. . . . . . . . . |

. . . . . . |

. . |

. . . . . |

. . . . . . |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||

9. |

. . . . . . .PLUS: Estimate Due for current month |

. . . . . . . . . |

. . . . . . |

. . |

. . . . . |

. . . . . . |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10. TOTAL TAX DUE (line 6 minus lines 7 and 8 plus line 9) |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11. PLUS: Penalty and interest, if due (see instructions) |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||

. . . . . . . . . . . . . . . . . . . . . .12. PLUS: Amounts overcollected |

. . . . . . |

. . |

. . . . . |

. . . . . . |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||||

13. LESS: Credit Claimed. Any credit for prior overpayment must be approved in advance by Department of Revenue |

|

|

|

|

|

|

|

||||||||||||||||||||

. . . . . . . . . . . . . . . . . . . . . . . . . .14. TOTAL AMOUNT DUE (line 10 plus lines 11 and 12 minus line 13). Transfer to front of return |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||||||||||||

Signed: ________________________________________________________________________ |

Date: _____________________________________________________________ |

DO NOT CUT OR STAPLE.

please be sure to put the proper name, account number, and period covered on the return before submitting it.

Alabama Income Tax Forms - Alternatively, filing can also be done via telephone for convenience.

Additionally, understanding the details and requirements of the Oklahoma Transfer-on-Death Deed is crucial for property owners to ensure a smooth transfer process. For more comprehensive guidance, you can visit todform.com/blank-oklahoma-transfer-on-death-deed/ and find the necessary resources to assist you in filling out this important document.

How Much Is Child Support in Alabama for One Child - Accurate record-keeping is essential for fulfilling legal obligations regarding child support.

Alabama Llc Tax Filing Requirements - This tax return must be filed irrespective of whether the entity operates in one or multiple states.

The Alabama 2100 form is similar to the IRS Form 1040, which is the standard individual income tax return. Both documents require taxpayers to report their income, deductions, and calculate their tax liability. Just as the 2100 form requires the reporting of sales and deductions, the 1040 form allows individuals to list their income sources and claim various deductions. Both forms also have a structured layout that guides taxpayers through the necessary calculations, ensuring that they provide all relevant information to the respective tax authorities.

Another document comparable to the Alabama 2100 is the state-level sales tax return form used by other states, like the California Sales and Use Tax Return (Form BOE-401-A). Similar to the Alabama form, this document is designed for businesses to report their sales tax collections and remit the owed amounts. Both forms require businesses to detail gross sales, deductions, and the total tax due, ensuring compliance with state tax laws. The California form also includes sections for discounts and penalties, much like the Alabama 2100.

The Florida Sales Tax Return (Form DR-15) is another document that mirrors the Alabama 2100 form. Both forms are used by businesses to report sales tax collected during a specific period. They share similar structures, asking for gross sales figures, deductions, and tax calculations. The Florida form also allows for adjustments, such as discounts and credits, akin to what is seen in the Alabama form. This ensures that businesses can accurately report their tax obligations to the state.

The New York State Sales Tax Return (Form ST-100) is also quite similar to the Alabama 2100 form. Both documents require businesses to report their sales, calculate the tax due, and provide details on any deductions or credits. The ST-100 form includes sections for various tax rates and allows for adjustments, just like the Alabama form. This commonality helps businesses across states follow a similar process when fulfilling their sales tax responsibilities.

Understanding the various Sales and Use Tax Returns, it's important to recognize the significance of compliance and accurate reporting in each state. For example, those involved in activities or events in California should also be aware of legal documents that protect their rights, such as the Hold Harmless Agreement, which further mitigates risks associated with participation and liability.

Lastly, the Texas Sales and Use Tax Return (Form 01-114) shares similarities with the Alabama 2100 form. Both forms serve the same purpose: to report sales and use tax collected by businesses. They require similar information, including gross sales, deductions, and the total amount of tax owed. Each form also provides a breakdown of tax rates applicable to different categories of sales, ensuring that businesses can accurately calculate their tax liabilities in compliance with state regulations.

Filling out the Alabama 2100 form can be a straightforward process, but many people make common mistakes that can lead to delays or complications. One frequent error is not providing the correct name and account number. These details are crucial for the Department of Revenue to identify your account. If these are incorrect or missing, your return may not be processed in a timely manner.

Another mistake occurs when individuals fail to accurately calculate their total deductions. This figure is essential for determining the total amount of tax due. If you underestimate or overestimate your deductions, it can result in either a higher tax bill or potential penalties for underpayment. Always double-check your calculations to ensure accuracy.

People also often neglect to check the due date for the return. Submitting the form late can incur penalties and interest charges. Marking your calendar with the due date helps to avoid this issue. Additionally, some individuals forget to sign the form before submitting it. A missing signature can lead to the return being deemed invalid, which means additional hassle to correct the oversight.

Lastly, many filers overlook the importance of the electronic funds transfer (EFT) option. If you are making a payment through EFT, be sure to check the corresponding box on the form. Not doing so can create confusion about how your payment was made and could complicate your filing process.

By being mindful of these common pitfalls, you can ensure a smoother experience when filling out the Alabama 2100 form. Attention to detail is key, and a little extra care can go a long way in avoiding complications.