Fill Out a Valid Alabama 40Es Form

Fill Out a Valid Alabama 40Es Form

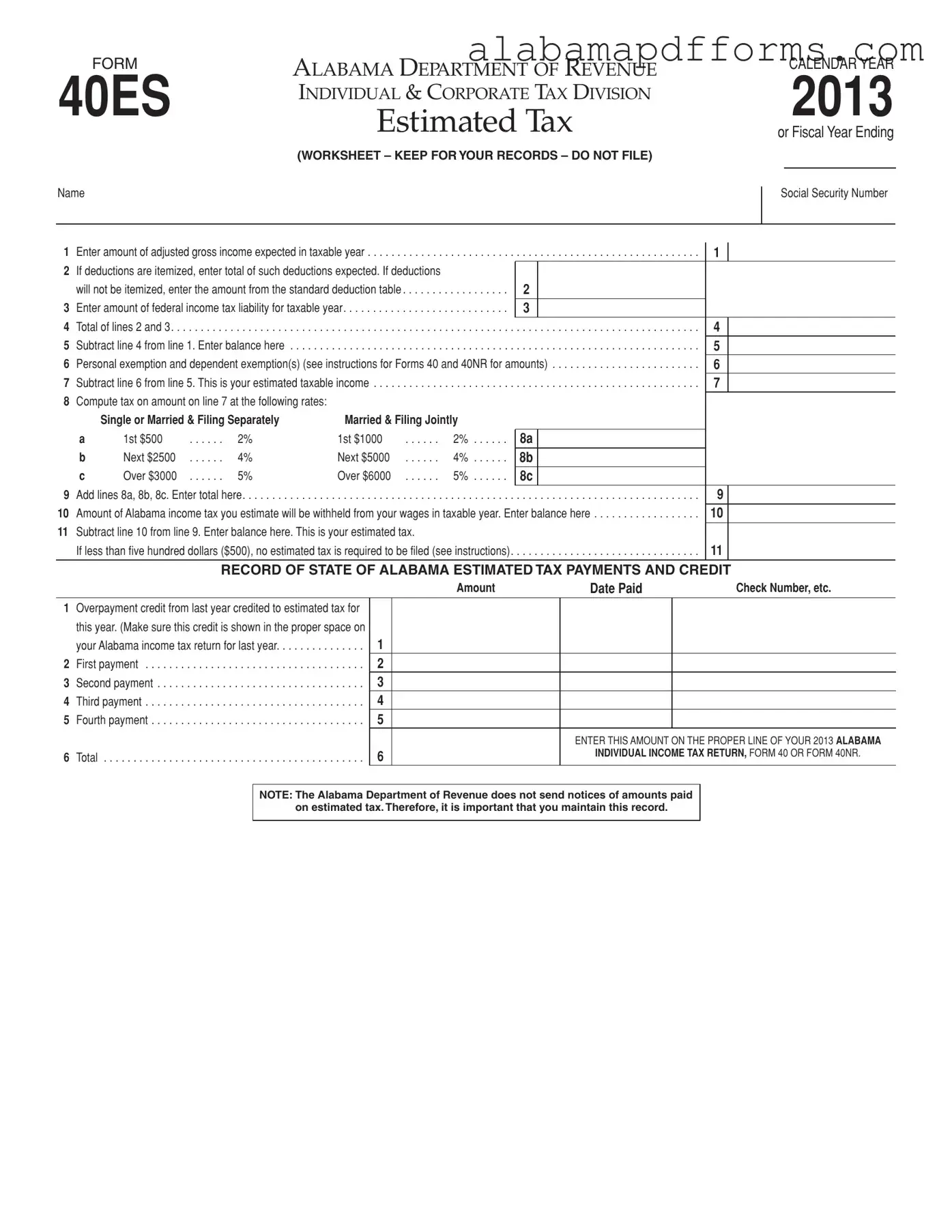

The Alabama 40ES form is an essential tool for individuals and corporations alike, helping them navigate the complexities of estimated tax payments in the state. This form, officially known as the Estimated Income Tax Payment Voucher, is designed to assist taxpayers in calculating their anticipated tax liabilities for the year. It requires you to input your expected adjusted gross income, any deductions you plan to take, and your federal tax liability, allowing for a clear picture of your estimated taxable income. The form breaks down the tax rates applicable based on your filing status, whether single, married filing jointly, or married filing separately. Additionally, it provides guidance on when to file and how to make payments, ensuring you stay compliant with Alabama tax regulations. Notably, if your estimated tax is less than $500, you may not need to file at all. Keeping accurate records of your payments is crucial, as the Alabama Department of Revenue does not send notifications of amounts paid. Understanding the nuances of the 40ES form can help you manage your tax obligations effectively, avoiding penalties and ensuring a smoother tax season.

Misconceptions about the Alabama 40ES form can lead to confusion regarding estimated tax payments. Below are ten common misconceptions along with clarifications for each.

This form is applicable to both individuals and corporations who need to pay estimated taxes.

Filing is only necessary if you expect to owe at least $500 in tax after subtracting your withholding and credits.

The 40ES form is a worksheet that you keep for your records and do not file with your tax return.

The form must be filed by specific due dates, including April 15, June 15, September 15, and January 15, depending on your payment schedule.

Anyone who expects to owe taxes, including those with income from wages, investments, or other sources, may need to file.

A refund from the previous year does not exempt you from filing estimated taxes if you expect to owe for the current year.

If you meet the criteria for estimated tax payments, they are required to avoid penalties.

Changes in your tax situation require you to file an amended voucher by the next payment deadline.

The Department does not send notices, making it essential to keep accurate records of your payments.

Payments must adhere to the calculated amounts based on your estimated income, and must be made in equal installments or in full by the due dates.

FORM |

ALABAMA DEPARTMENT OF REVENUE |

40ES |

ESTIMATED TAX |

|

INDIVIDUAL & CORPORATE TAX DIVISION |

|

(WORKSHEET – KEEP FOR YOUR RECORDS – DO NOT FILE) |

Name |

|

CALENDAR YEAR

2013

or Fiscal Year Ending

Social Security Number

1 Enter amount of adjusted gross income expected in taxable year |

1 |

2If deductions are itemized, enter total of such deductions expected. If deductions

|

will not be itemized, enter the amount from the standard deduction table |

2 |

|

|

|

3 |

Enter amount of federal income tax liability for taxable year |

3 |

|

|

|

4 |

Total of lines 2 and 3 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

4 |

|

5 |

Subtract line 4 from line 1. Enter balance here |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

5 |

|

6 |

Personal exemption and dependent exemption(s) (see instructions for Forms 40 and 40NR for amounts) |

6 |

|

||

7 |

Subtract line 6 from line 5. This is your estimated taxable income |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

7 |

|

8Compute tax on amount on line 7 at the following rates:

|

Single or Married & Filing Separately |

Married & Filing Jointly |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

a |

1st $500 |

. 2% |

1st $1000 |

2% |

8a |

|

|

|

|

b |

Next $2500 |

. 4% |

Next $5000 |

4% |

8b |

|

|

|

|

c |

Over $3000 |

. 5% |

Over $6000 |

5% |

8c |

|

|

|

|

9 Add lines 8a, 8b, 8c. Enter total here |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . |

. . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

9 |

|

||

|

|

|

|

|

|

||||

10 Amount of Alabama income tax you estimate will be withheld from your wages in taxable year. Enter balance here |

|

10 |

|

||||||

11 Subtract line 10 from line 9. Enter balance here. This is your estimated tax. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

||||

If less than five hundred dollars ($500), no estimated tax is required to be filed (see instructions). |

. . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

11 |

|

||||

|

|

|

|

|

|

|

|||

|

|

RECORD OF STATE OF ALABAMA ESTIMATED TAX PAYMENTS AND CREDIT |

|||||||

|

|

|

|

Amount |

|

Date Paid |

|

Check Number, etc. |

|

1Overpayment credit from last year credited to estimated tax for this year. (Make sure this credit is shown in the proper space on your Alabama income tax return for last year. . . . . . . . . . . . . . .

2 First payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Second payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4 Third payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 Fourth payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6 Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

2

3

4

5

6

ENTER THIS AMOUNT ON THE PROPER LINE OF YOUR 2013 ALABAMA

INDIVIDUAL INCOME TAX RETURN, FORM 40 OR FORM 40NR.

NOTE: The Alabama Department of Revenue does not send notices of amounts paid on estimated tax. Therefore, it is important that you maintain this record.

Form 40ES Instructions

Who Must Pay Estimated Tax

If you owe additional tax for 2012, you may have to pay esti- mated tax for 2013.

You can use the following general rule as a guide during the year to see if you will have enough withholding, or if you should in- crease your withholding or make estimated tax payments.

General Rule. In most cases, you must pay estimated tax for 2013 if both of the following apply.

1.You expect to owe at least $500 in tax for 2013, after sub- tracting your withholding and credits.

2.You expect your withholding plus your credits to be less than the smaller of:

a.90% of the tax to be shown on your 2013 tax return, or

b.100% of the tax shown on the your 2012 tax return. Your 2012 tax return must cover all 12 months.

Special Rule for Higher Income Taxpayers

If your Alabama AGI for 2012 was more than $150,000 ($75,000 if your filing status for 2013 is Married Filing a Separate Return) substitute 110% for 100% in (2b) under General Rule, above.

When and Where to File Estimated Tax

Your estimated tax must be filed on or before April 15, 2013, or on such later dates as specified under “Farmers.” It should be mailed to the Alabama Department of Revenue, Individual Esti- mates, P.O. Box 327485, Montgomery, AL

Payment of Estimated Tax

Your estimated tax may be paid in full or in equal installments on or before April 15, 2013, June 15, 2013, September 15, 2013 and January 15, 2014. If the 15th falls on a Saturday, Sunday, or State holiday, the due date will then be considered the following

business day. Checks or money orders should be made payable to the Alabama Department of Revenue.

Changes In Tax

Even though your situation on April 15 is such that you are not required to file estimated tax at that time, your expected tax may change so that you will be required to file estimated tax later. In such case, the time for filing is as follows: June 15, if the change occurs after April 1 and before June 2; September 15, if the change occurs after June 1 and before September 2; January 15, if the change occurs after September 1. If, after you have filed a voucher, you find that your estimated tax is substantially increased or de- creased as the result of a change in your tax, you should file an amended voucher on or before the next filing date – June 15, 2013, September 15, 2013, January 15, 2014.

Farmers

If at least 2/3 of your estimated gross income for the taxable year is derived from farming, you may pay estimated tax at any time on or before January 15, 2014 instead of April 15, 2013. If you wait until January 15, 2014, you must pay the entire balance of the estimated tax. However, if farmers file their final tax return on or before March 2, 2013, and pay the total tax at that time, they need not file estimated tax.

Fiscal Year

If you file your income tax return on a fiscal year basis, you will substitute for the dates specified in the above instructions the months corresponding thereto.

Penalties for Underpayment

Penalties are provided for underpaying the Alabama income tax by at least $500.00.

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➀ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

✁

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

ADOR |

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➁ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

✁

ADOR

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➂ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

✁

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

ADOR |

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➃ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

✁

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

ADOR |

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

Alabama State Tax Form - Finally, maintaining copies of the submitted form is crucial for future reference or audits.

For those looking to effectively manage rental agreements, understanding the nuances of a comprehensive Lease Agreement form is essential. This form serves as the foundation of a solid landlord-tenant relationship, ensuring both parties are clear on their rights and obligations. To expedite the process, complete your Lease Agreement today.

Alabama Income Tax Forms - The Alabama 2320 form is the State Lodgings Tax Return required for lodging businesses.

The IRS Form 1040 serves as the standard individual income tax return for U.S. taxpayers. Like the Alabama 40ES form, it requires individuals to report their income, deductions, and tax liability. Both forms aim to calculate the amount of tax owed or the refund due. However, while the 40ES focuses on estimated tax payments for the upcoming year, the 1040 is used to report actual income and tax obligations for the previous year. Both forms also include sections for personal information, such as Social Security numbers, and allow for various deductions, though the 1040 typically encompasses a broader range of tax situations.

The IRS Form 1040-ES is specifically designed for estimating and paying quarterly taxes. Similar to the Alabama 40ES, this form is used by individuals who expect to owe tax of $1,000 or more when they file their return. Both forms require taxpayers to estimate their income and deductions for the year, and they outline the payment schedule for estimated taxes. The 1040-ES serves a similar purpose on a federal level, providing a way for taxpayers to avoid penalties for underpayment by making timely estimated payments throughout the year.

The IRS Form 1065 is utilized by partnerships to report income, deductions, and other important financial information. While this form is not for individual taxpayers, it shares similarities with the Alabama 40ES in that it requires the reporting of estimated tax obligations. Partnerships must estimate their income and pay taxes on behalf of their partners, similar to how individuals use the 40ES to estimate their personal tax liabilities. Both forms emphasize the importance of accurate estimations to avoid penalties and ensure compliance with tax regulations.

Understanding the various tax forms is essential for timely compliance, particularly when it comes to estimated tax payments like the Alabama 40ES. This form allows individuals to forecast their tax obligations and avoid penalties throughout the year, ensuring they stay on top of their financial responsibilities. Similarly, individuals and businesses may also consider a Hold Harmless Agreement to further manage their liabilities in different contexts, emphasizing the importance of proper documentation and foresight in financial planning.

The IRS Form 1120 is the corporate income tax return for U.S. corporations. Like the Alabama 40ES, it requires corporations to report their income and calculate their tax liability. Both forms emphasize the need for accurate estimations, especially for corporations that may need to make estimated tax payments throughout the year. While the 40ES is tailored for individuals, the 1120 serves as a parallel for corporate entities, highlighting the commonality of tax estimation across different types of taxpayers.

The IRS Form 941 is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. This form is similar to the Alabama 40ES in that it requires employers to estimate their tax liabilities based on payroll. Both forms emphasize the importance of accurate reporting to avoid underpayment penalties. While the 40ES is focused on individual income tax, the 941 addresses payroll taxes, illustrating the broader context of tax obligations that require estimation and timely payment.

The IRS Form 990 is filed by tax-exempt organizations to provide information about their financial activities. Like the Alabama 40ES, it includes estimates of income and expenses, but it is specifically designed for non-profit entities. Both forms require the reporting of financial information to ensure compliance with tax laws. The 990 shares the common goal of transparency and accountability in financial reporting, though it serves a different audience than the 40ES.

The state of Alabama's Form 40 serves as the individual income tax return for residents. Similar to the Alabama 40ES, it requires taxpayers to report their income and calculate their tax liability. The 40 is filed after the tax year has ended, while the 40ES is for estimated payments throughout the year. Both forms require personal information and aim to ensure that taxpayers meet their obligations, highlighting the ongoing relationship between estimated and actual tax reporting in the state tax system.

Filling out the Alabama 40ES form can be a straightforward process, but mistakes can lead to delays or issues with your tax obligations. One common mistake is failing to use the correct form for the specific tax year. Make sure you are using the form for the year you intend to file. Using an outdated form can result in incorrect calculations and potential penalties.

Another frequent error is not entering your social security number correctly. This number is crucial for identifying your tax records. Double-check that you have entered it accurately, especially if you are filing jointly with a spouse. A simple typo can cause significant problems.

People often forget to include all sources of income when estimating their adjusted gross income. It’s important to consider all income streams, including wages, freelance work, and investments. Underestimating your income can lead to an underpayment of taxes, which may incur penalties later.

Itemized deductions can be confusing. Some filers mistakenly enter the total of their itemized deductions instead of the standard deduction amount if they are not itemizing. Make sure to follow the instructions carefully to avoid this common pitfall.

Line 4 of the form requires you to total your deductions and federal tax liability. Some individuals forget to add these amounts correctly, leading to an inaccurate balance on line 5. Take your time with calculations to ensure accuracy.

Another mistake is not accounting for personal and dependent exemptions. These exemptions can significantly affect your estimated taxable income. Failing to include them can result in a higher estimated tax than necessary.

When calculating your estimated tax, it's essential to apply the correct tax rates based on your filing status. Many people overlook this step or apply the wrong rates, leading to incorrect tax estimates. Review the tax rates carefully to ensure you are calculating correctly.

Additionally, some filers forget to subtract the amount of tax expected to be withheld from their wages. This oversight can inflate the estimated tax amount and lead to unnecessary payments. Always consider withholdings when filling out the form.

Lastly, individuals often neglect to keep a record of their estimated tax payments. The Alabama Department of Revenue does not send notices of payments made, so it is crucial to maintain your own records. This will help you avoid confusion when filing your tax return later.

By being mindful of these common mistakes, you can fill out the Alabama 40ES form more accurately and avoid potential issues down the line.