Fill Out a Valid Alabama 40X Form

Fill Out a Valid Alabama 40X Form

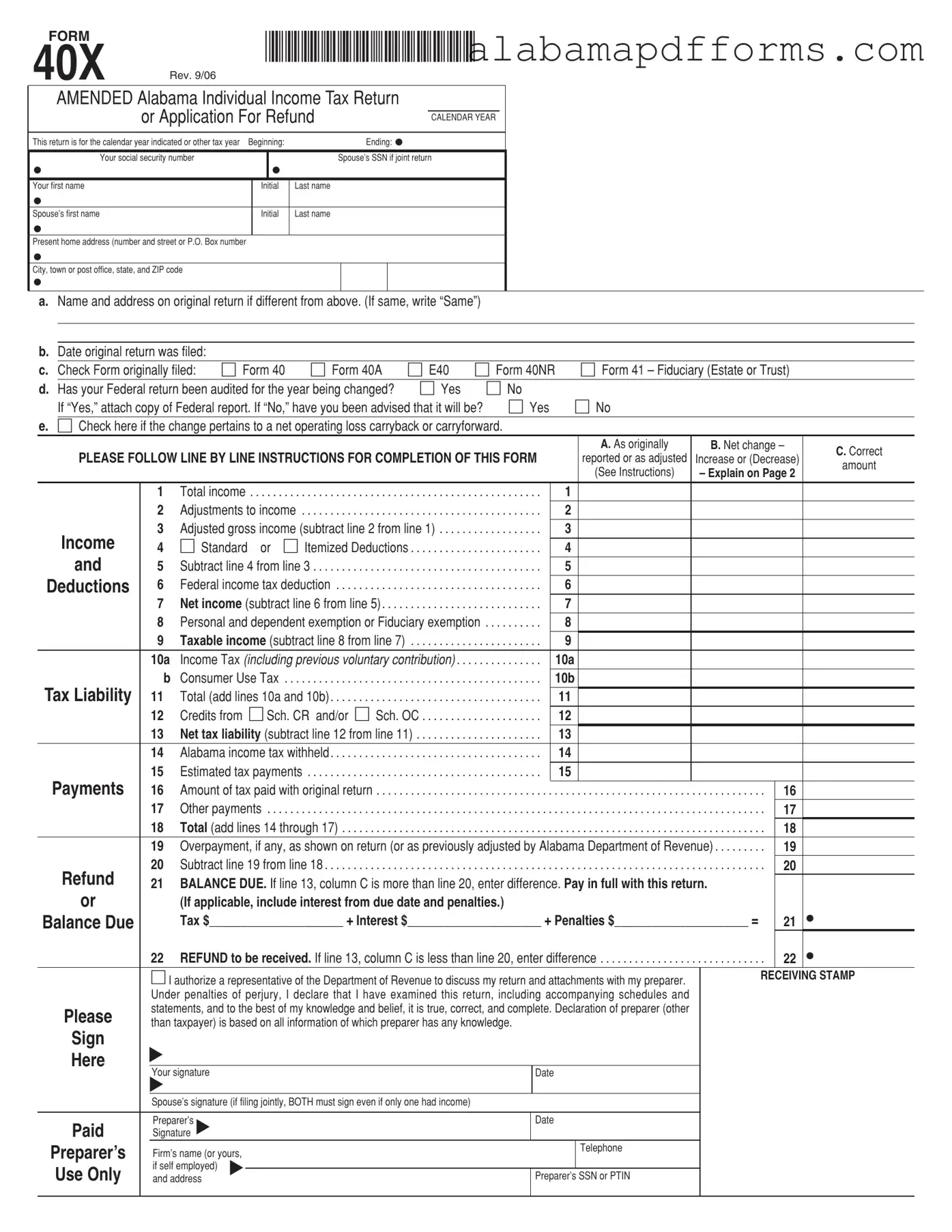

The Alabama 40X form serves as a crucial tool for individuals seeking to amend their previously filed Alabama Individual Income Tax Return or to request a refund. This form is specifically designed for taxpayers who need to correct errors or report changes related to their income, deductions, or credits from an earlier return. It requires detailed information such as the taxpayer's Social Security number, the original return's filing date, and the specific reasons for the amendments. The form also includes sections for calculating total income, adjusted gross income, and taxable income, as well as any applicable deductions and credits. Additionally, taxpayers must provide their signature and, if applicable, their spouse's signature when filing jointly. Clear instructions guide users through each line, ensuring that they report changes accurately. The completed form must be mailed to the appropriate Alabama Department of Revenue address, distinct from where current returns are sent, to ensure proper processing. Understanding the Alabama 40X form is essential for anyone looking to rectify their tax filings effectively.

Misconceptions about the Alabama 40X Form

FORM |

|

|

*XX12830140X* |

||||||||

40X |

|

|

|||||||||

REV. 9/06 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

AMENDED Alabama Individual Income Tax Return |

|

||||||||||

|

or Application For Refund |

|

|

|

|

|

|

||||

|

|

|

|

CALENDAR YEAR |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

This return is for the calendar year indicated or other tax year |

Beginning: |

|

|

Ending: • |

|

||||||

Your social security number |

|

|

|

|

Spouse’s SSN if joint return |

|

|||||

• |

|

|

|

• |

|

|

|

|

|

|

|

Your first name |

|

|

Initial |

Last name |

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

Spouse’s first name |

|

|

Initial |

Last name |

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

Present home address (number and street or P.O. Box number |

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

City, town or post office, state, and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

a.Name and address on original return if different from above. (If same, write “Same”)

b.Date original return was filed:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c. Check Form originally filed: |

|

Form 40 |

Form 40A |

E40 |

Form 40NR |

|

|

Form 41 – Fiduciary (Estate or Trust) |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

d. Has your Federal return been audited for the year being changed? |

Yes |

|

No |

|

|

|

|

|

|

|

|

|||||||||||

|

If “Yes,” attach copy of Federal report. If “No,” have you been advised that it will be? |

Yes |

No |

|

|

|

|

|

||||||||||||||

e. Check here if the change pertains to a net operating loss carryback or carryforward. |

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. As originally |

|

B. Net change – |

C. Correct |

||

|

PLEASE FOLLOW LINE BY LINE INSTRUCTIONS FOR COMPLETION OF THIS FORM |

|

|

reported or as adjusted |

Increase or (Decrease) |

|||||||||||||||||

|

|

|

amount |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(See Instructions) |

|

– Explain on Page 2 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

1 |

Total income |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . |

. |

. |

|

1 |

|

|

|

|

|

|

|

|||||

|

|

2 |

Adjustments to income . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . |

. |

. |

|

2 |

|

|

|

|

|

|

|

|||||

|

Income |

3 |

Adjusted gross income (subtract line 2 from line 1) |

. . |

. . . . . . . . |

. |

. |

|

3 |

|

|

|

|

|

|

|

||||||

|

4 |

. . . . . . . . . . . Standard or Itemized Deductions |

. . |

. . . . . . . . |

. |

. |

|

4 |

|

|

|

|

|

|

|

|||||||

|

and |

5 |

Subtract line 4 from line 3 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . |

. |

. |

|

5 |

|

|

|

|

|

|

|

|||||

Deductions |

6 |

Federal income tax deduction |

. . |

. . . . . . . . |

. |

. |

|

6 |

|

|

|

|

|

|

|

|||||||

|

|

7 |

. . . . . . . . . . . . . . . .Net income (subtract line 6 from line 5) |

. . |

. . . . . . . . |

. |

. |

|

7 |

|

|

|

|

|

|

|

||||||

|

|

8 |

Personal and dependent exemption or Fiduciary exemption |

. . . . . . . . |

. |

. |

|

8 |

|

|

|

|

|

|

|

|||||||

|

|

9 |

Taxable income (subtract line 8 from line 7) |

. . . . . . . . . . . |

. . |

. . . . . . . . |

. |

. |

|

9 |

|

|

|

|

|

|

|

|||||

|

|

|

10a |

Income Tax (including previous voluntary contribution) . . . |

. . |

. . . . . . . . |

. |

. |

|

10a |

|

|

|

|

|

|

|

|||||

|

|

|

b |

Consumer Use Tax |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . |

. |

. |

|

10b |

|

|

|

|

|

|

|

||||

Tax Liability |

11 |

. . . . . . . . . . . . . . . . . . . . . . . . .Total (add lines 10a and 10b) |

. . |

. . . . . . . . |

. |

. |

|

11 |

|

|

|

|

|

|

|

|||||||

|

|

12 |

. . . . . . . . .Credits from Sch. CR and/or Sch. OC |

. . |

. . . . . . . . |

. |

. |

|

12 |

|

|

|

|

|

|

|

||||||

|

|

13 |

. . . . . . . . . .Net tax liability (subtract line 12 from line 11) |

. . |

. . . . . . . . |

. |

. |

|

13 |

|

|

|

|

|

|

|

||||||

|

|

14 |

Alabama income tax withheld |

. . |

. . . . . . . . |

. |

. |

|

14 |

|

|

|

|

|

|

|

||||||

|

|

15 |

Estimated tax payments . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . |

. |

. |

|

15 |

|

|

|

|

|

|

|

|||||

Payments |

16 |

. . . . . . . . . . . . . . . . .Amount of tax paid with original return |

. . |

. . . . . . . . |

. |

. . . |

. . . . |

. |

. . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . |

. |

16 |

|

||||||||

|

|

17 |

. . . . . . . .Other payments |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . |

. |

. . . |

. . . . |

. |

. . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . |

. |

17 |

|

||||||

|

|

18 |

. . . . . . . . . . . . . . . . . . . . . . .Total (add lines 14 through 17) |

. . |

. . . . . . . . |

. |

. . . |

. . . . |

. |

. . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . |

. |

18 |

|

|||||||

|

|

19 |

Overpayment, if any, as shown on return (or as previously adjusted by Alabama Department of Revenue) |

. |

19 |

|

||||||||||||||||

|

Refund |

20 |

. . . . . . . . . . . . . . . . . . . . . . . . . .Subtract line 19 from line 18 |

. . |

. . . . . . . . |

. |

. . . |

. . . . |

. |

. . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . |

. |

20 |

|

|||||||

|

21 |

BALANCE DUE. If line 13, column C is more than line 20, enter difference. Pay in full with this return. |

|

|

|

|||||||||||||||||

|

or |

|

|

(If applicable, include interest from due date and penalties.) |

|

|

|

|

|

|

|

|

||||||||||

Balance Due |

|

|

Tax $_____________________ + Interest $_____________________ + Penalties $_____________________ = |

|

21 |

• |

||||||||||||||||

|

|

22 |

REFUND to be received. If line 13, column C is less than line 20, enter difference |

. . |

. . . . . . . . . . |

. |

22 |

• |

||||||||||||||

|

|

|

I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer. |

|

|

RECEIVING STAMP |

||||||||||||||||

|

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and |

|

|

|

|

|

||||||||||||||

|

Please |

|

statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other |

|

|

|

|

|

||||||||||||||

|

|

than taxpayer) is based on all information of which preparer has any knowledge. |

|

|

|

|

|

|

|

|

||||||||||||

|

Sign |

|

▼ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Here |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your signature |

|

|

|

|

|

|

|

Date |

|

|

|

|

|

|

|

|

|||

|

|

|

▼ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s signature (if filing jointly, BOTH must sign even if only one had income) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

|

Preparer’s |

▼ |

|

|

|

|

|

|

|

Date |

|

|

|

|

|

|

|

|

||

|

|

Signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Preparer’s |

|

Firm’s name (or yours, |

|

|

|

|

|

|

|

|

|

Telephone |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Use Only |

|

if self employed) |

▼ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

and address |

|

|

|

|

|

|

|

Preparer’s SSN or PTIN |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*XX12830240X*

Form 40X |

Page 2 |

EXPLANATION OF CHANGES TO INCOME, EXEMPTIONS, DEDUCTIONS, AND CREDITS.

Enter the line reference from page 1 for which you are reporting a change, and give the reason for each change. Attach applicable schedules.

MAILING INSTRUCTIONS. Mail this return to: Alabama Department of Revenue Individual and Corporate Tax Division P.O. Box 327464

Montgomery, AL

Do Not mail your current return with Form 40X, it must be mailed to a different address.

Alabama Environment - This form is vital in ensuring that patient dismissals are conducted fairly and with due process.

When creating a rental agreement, it's important to have a proper Lease Agreement template that ensures all necessary details are captured correctly. This template can guide you through the key aspects needed for a successful rental. For more information, visit our site to explore a customizable Lease Agreement sample for your needs.

Alabama Poa - If you’re unable to travel or meet deadlines, this form can serve as a practical solution.

The IRS Form 1040 serves as the standard individual income tax return for U.S. taxpayers. Like the Alabama 40X form, it allows individuals to report their income, deductions, and tax liability for a given tax year. The 1040 form is essential for calculating federal tax obligations and can be amended using Form 1040-X, which is similar to the Alabama 40X in that it addresses changes to previously filed returns. Both forms require taxpayers to provide personal information, income details, and any adjustments necessary for accurate reporting.

Form 1040-X is specifically designed for amending a federal income tax return. Much like the Alabama 40X, it allows taxpayers to correct errors or make adjustments to their original Form 1040. The process involves providing a clear explanation of the changes, which mirrors the Alabama form's requirement for detailing adjustments to income or deductions. Both forms aim to ensure that taxpayers can rectify mistakes and comply with tax regulations effectively.

Form 40 is Alabama's standard individual income tax return, similar to the IRS Form 1040. The Alabama 40X form is used to amend this return. While Form 40 captures the original details of a taxpayer's income and deductions, the 40X allows for corrections and updates. Both forms share a common structure, including sections for personal information, income calculations, and tax liabilities, but the 40X focuses specifically on changes made after the original submission.

Form 40A is a simplified version of the Alabama income tax return for certain taxpayers. Like the Alabama 40X, it provides a streamlined approach to reporting income and deductions. The 40X can be used by individuals who initially filed a 40A and later need to amend their return. Both forms emphasize clarity and accuracy in reporting, making them accessible for individuals with varying levels of tax knowledge.

Form E40 is used for non-resident individuals who earn income in Alabama. This form is similar to the Alabama 40X in that it requires detailed reporting of income and deductions for those who may not be full-time residents. If a non-resident needs to amend their tax return, they would use the 40X form, which allows for adjustments similar to those made on the E40. Both forms ensure that non-residents accurately report their Alabama tax obligations.

Form 40NR is specifically for non-residents and part-year residents filing an income tax return in Alabama. The Alabama 40X serves a similar purpose for amending returns filed on the 40NR. Both forms require specific details about income earned in Alabama and allow for adjustments based on changes in circumstances or corrections. This ensures that non-residents are held accountable for their tax responsibilities while providing a means to rectify any errors.

Form 41 is designed for fiduciaries, such as estates or trusts, to report income and deductions. Like the Alabama 40X, it allows for amendments to previously filed fiduciary returns. Both forms require detailed reporting of income, deductions, and tax liabilities, with the 40X specifically catering to changes made to the original fiduciary return. This ensures that fiduciaries can accurately report their tax obligations and make necessary adjustments.

The IRS Form 1040 is an essential document for individual taxpayers in the United States, similar to the Alabama 40X form in that both are used for reporting income and calculating tax liability. Unlike the Alabama 40X form, which specifically addresses amendments or changes to a previously filed Alabama tax return, the IRS Form 1040 encompasses the entirety of individual income tax reporting. Adjustments made on the 40X can often have federal tax implications, and taxpayers may also need to reflect similar changes on their federal Form 1040 to maintain accuracy across their tax documentation. Additionally, understanding related agreements, such as a Hold Harmless Agreement, can provide further insight into liability considerations during the tax process.

Form CR is used to claim various tax credits in Alabama. While it serves a different purpose than the Alabama 40X, both forms can intersect when an individual needs to amend their return to reflect changes in credits claimed. The 40X allows taxpayers to adjust their overall tax liability, which may include updates to the credits reported on Form CR. This connection highlights the importance of accurate reporting across different forms for a complete tax picture.

Filling out the Alabama 40X form can be a straightforward task, but many people make common mistakes that can delay processing or lead to incorrect filings. One frequent error is forgetting to include the correct social security numbers. This information is crucial for the tax authorities to identify your records accurately. If you’re filing jointly, both social security numbers must be included. Missing even one can cause complications.

Another common mistake involves not checking the correct box for the form originally filed. Whether you filed Form 40, Form 40A, or another version, it’s important to indicate this accurately. If you check the wrong box, it may confuse the reviewers and slow down your application for a refund or adjustment.

People often overlook the importance of signing the form. Both spouses must sign if filing jointly. An unsigned form can be considered incomplete, leading to delays or rejection. Ensure that you and your spouse both sign and date the form before submitting it.

Some individuals fail to provide a clear explanation of the changes being made on Page 2. The tax authorities require a detailed description of the adjustments. If this section is left blank or filled out vaguely, it can lead to questions and further inquiries, prolonging the process.

Additionally, many forget to attach necessary documents. If your federal return has been audited, a copy of that report must be included. Neglecting to attach relevant schedules can also result in the form being returned for missing information.

Finally, double-checking your math is essential. Errors in calculations can lead to incorrect tax liabilities or refunds. Take the time to review each line carefully. A small mistake can have a big impact on your financial situation.