Fill Out a Valid Alabama 41 Form

Fill Out a Valid Alabama 41 Form

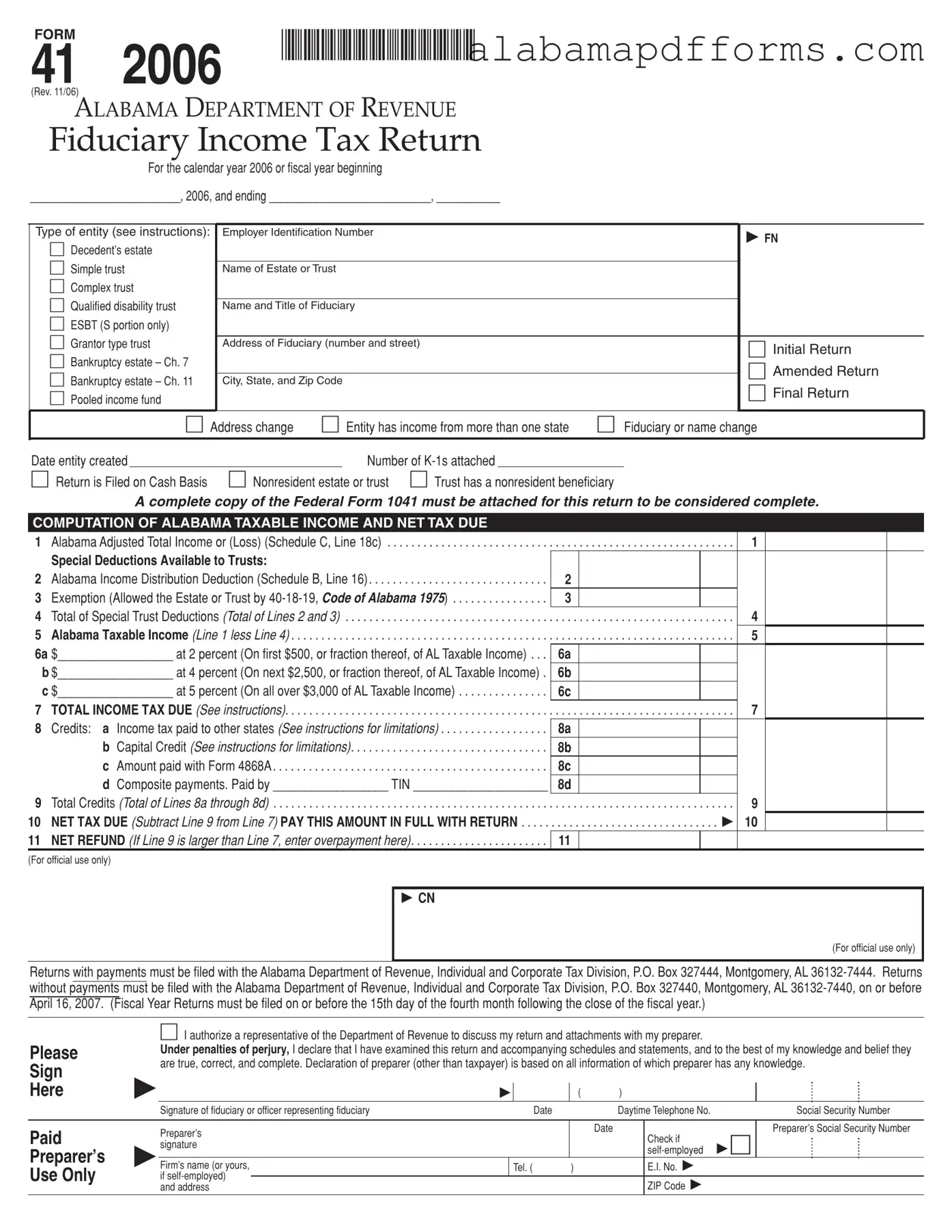

The Alabama 41 form is a crucial document for fiduciaries managing estates and trusts in Alabama. It serves as the state's fiduciary income tax return, detailing the income generated by the estate or trust for a specific calendar year or fiscal year. Various types of entities can use this form, including decedent’s estates, simple trusts, complex trusts, and even bankruptcy estates. The form requires specific information such as the entity's name, employer identification number, and the fiduciary's contact details. It also includes sections for reporting Alabama taxable income, calculating the net tax due, and claiming any available credits. Notably, a complete copy of the federal Form 1041 must accompany the Alabama 41 for the return to be considered complete. This form not only helps ensure compliance with state tax laws but also allows fiduciaries to take advantage of deductions and credits that may reduce their overall tax liability. Understanding the Alabama 41 form is essential for fiduciaries to fulfill their responsibilities accurately and efficiently.

Misconception 1: The Alabama 41 form is only for large estates or trusts.

This is not true. The Alabama 41 form is required for various types of entities, including simple trusts and decedent’s estates, regardless of their size. Even smaller estates or trusts with minimal income must file this form if they meet certain criteria.

Misconception 2: You do not need to attach the Federal Form 1041 when filing the Alabama 41 form.

In fact, a complete copy of the Federal Form 1041 must be attached for the Alabama 41 return to be considered complete. This is a crucial requirement that ensures the Alabama Department of Revenue has all necessary information to process your return.

Misconception 3: Filing the Alabama 41 form is optional if the estate or trust has no income.

Even if an estate or trust has no income, filing the Alabama 41 form may still be necessary. If the entity was created or has any other tax obligations, it is important to file to avoid potential penalties or complications in the future.

Misconception 4: The due date for filing the Alabama 41 form is the same for all entities.

This is misleading. The due date for the Alabama 41 form is typically April 16 for calendar year filers. However, fiscal year filers must submit their returns by the 15th day of the fourth month following the close of their fiscal year. It is essential to check the specific due date that applies to your situation.

FORM |

|

*0612830141* |

41 |

2006 |

(Rev. 11/06)

ALABAMA DEPARTMENT OF REVENUE

Fiduciary Income Tax Return

For the calendar year 2006 or fiscal year beginning

__________________________, 2006, and ending ____________________________, ___________

Type of entity (see instructions): Decedent’s estate

Simple trust

Complex trust

Qualified disability trust

ESBT (S portion only)

Grantor type trust

Bankruptcy estate – Ch. 7

Bankruptcy estate – Ch. 11

Pooled income fund

Employer Identification Number

Name of Estate or Trust

Name and Title of Fiduciary

Address of Fiduciary (number and street)

City, State, and Zip Code

FN

Initial Return

Amended Return

Final Return

|

|

Address change |

Entity has income from more than one state |

Fiduciary or name change |

||||

|

|

|

|

|

|

|

|

|

Date entity created |

|

|

|

Number of |

|

|

|

|

Return is Filed on Cash Basis |

|

Nonresident estate or trust |

Trust has a nonresident beneficiary |

|

|

|||

A complete copy of the Federal Form 1041 must be attached for this return to be considered complete.

COMPUTATION OF ALABAMA TAXABLE INCOME AND NET TAX DUE |

|

|

1 |

Alabama Adjusted Total Income or (Loss) (Schedule C, Line 18c) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 |

|

Special Deductions Available to Trusts: |

|

2 |

Alabama Income Distribution Deduction (Schedule B, Line 16) |

2 |

3 |

Exemption (Allowed the Estate or Trust by |

3 |

4 |

Total of Special Trust Deductions (Total of Lines 2 and 3) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 |

5 |

Alabama Taxable Income (Line 1 less Line 4) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 |

6a |

$__________________ at 2 percent (On first $500, or fraction thereof, of AL Taxable Income) . . . |

6A |

b$__________________ at 4 percent (On next $2,500, or fraction thereof, of AL Taxable Income) . 6B |

||

c $__________________ at 5 percent (On all over $3,000 of AL Taxable Income) |

6C |

|

7 |

TOTAL INCOME TAX DUE (See instructions) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 |

8 |

Credits: a Income tax paid to other states (See instructions for limitations) |

8A |

|

b Capital Credit (See instructions for limitations) |

8B |

|

c Amount paid with Form 4868A |

8C |

|

d Composite payments. Paid by __________________ TIN _____________________ |

8D |

9 |

Total Credits (Total of Lines 8a through 8d) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 |

10 |

NET TAX DUE (Subtract Line 9 from Line 7) PAY THIS AMOUNT IN FULL WITH RETURN |

. . . . . . . . . . . . . . . . . . . . . . . . . . . 10 |

11 |

NET REFUND (If Line 9 is larger than Line 7, enter overpayment here) |

11 |

(For official use only) |

|

|

|

CN |

|

(For official use only)

Returns with payments must be filed with the Alabama Department of Revenue, Individual and Corporate Tax Division, P.O. Box 327444, Montgomery, AL

Please

Sign

Here

I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

( )

Signature of fiduciary or officer representing fiduciary |

Date |

Daytime Telephone No. |

Social Security Number |

Paid

Preparer’s

Use Only

Preparer’s signature

Firm’s name (or yours, if

|

|

Date |

|

Preparer’s Social Security Number |

|

|

|

Check if |

|

|

|

|

|

|

|

Tel. ( |

) |

E.I. No. |

|

|

|

|

|

|

|

|

|

ZIP Code |

|

|

|

|

|

|

FORM |

*0612830241* |

|

41 2006 |

Alabama Fiduciary Income Tax Return |

PAGE 2

Name of estate or trust

Employer identification number

Name and title of fiduciary

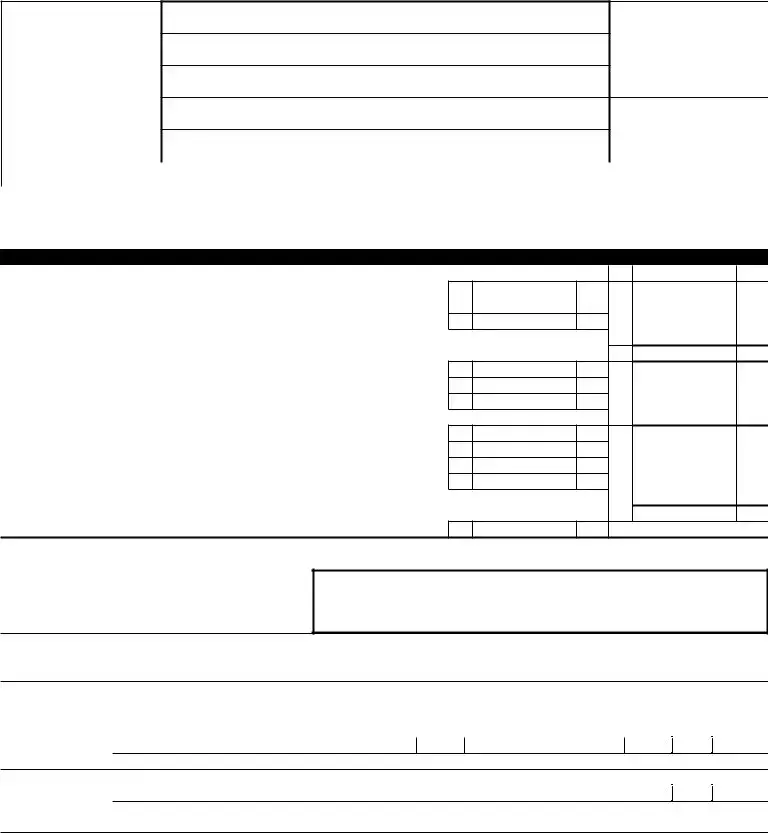

SCHEDULE A – ALABAMA CHARITABLE DEDUCTION. Do not complete for a simple trust or a pooled income fund. |

||

|

|

1 |

1 |

Amounts paid or permanently set aside for charitable purposes from gross income |

|

|

|

2 |

2 |

Alabama |

|

|

|

3 |

3 |

Subtract line 2 from line1 |

|

|

|

4 |

4 |

Capital gains for the tax year allocated to corpus and paid or permanently set aside for charitable purposes |

|

|

|

5 |

5 |

Alabama Charitable Deduction.Add Line 3 and Line 4. Enter total here and on Page 3, Schedule C, Line 13, Column C |

|

SCHEDULE B – COMPUTATION OF ALABAMA INCOME DISTRIBUTION DEDUCTION |

|

|

|

|

1 |

1 |

Alabama Adjusted Total Income (Page 1, Lne 1) |

|

2The amount of gain from the sale of capital assets, but only if the gain was allocated to corpus and not paid, credited,

|

2 |

or required to be distributed to any beneficiary during the taxable year or not included in Line 4, Schedule A (see instructions) |

|

|

3 |

3 Subtract the amount entered on Line 2 from the amount entered on Line 1, and enter in Line 3 |

|

4The amount of loss from the sale of capital assets – entered as a positive number, only if the loss was not considered

|

in the determination of the amount to be paid, credited, or required to be distributed to any beneficiary during taxable year |

4 |

5 |

Amount of tax exempt interest income excluded in computing Alabama taxable income |

5 |

6 |

Other adjustments – see instructions |

6 |

7 |

Alabama Distributable Net Income (Sum of Lines 3 through 6) |

7 |

8If a complex trust, enter accounting income for the tax year as determined under the

|

governing instrument and applicable local law |

8 |

|

|

|

|

|

|

|

|

|

9 Income required to be distributed currently |

9 |

||

|

|

|

|

10 |

Other amounts paid, credited, or otherwise required to be distributed |

10 |

|

|

|

|

|

11 |

Total distributions. add Lines 9 and 10 |

11 |

|

|

|

|

|

12 |

Enter the amount of |

12 |

|

|

|

|

|

13 |

Tentative income distribution deduction. Subtract Line 12 from Line 11 |

13 |

|

|

|

|

|

14 |

Tentative income distribution deduction. Subtract Line 5 from Line 7. If zero or less, enter |

14 |

|

|

|

|

|

15 |

Special Alabama Income Distribution Deduction (see instructions for applicability of the special limitation) |

15 |

|

16Alabama Income Distribution Deduction. Enter the smallest of Line 13, Line 14, or, if applicable, Line 15,

on this line and on Page 1, Line 2. (Do not enter less than zero.) |

16 |

CHANGE IN ALABAMA TAX LAW

CONCERNING ESTATES AND TRUSTS

The Alabama Legislature passed the Subchapter J and Business Trust Conformity Act (Act Number

At the time the 2006 Form 41 was being developed, the promulgation process had begun for the regulations to implement the Act.

FORM |

*0612830341* |

|

41 2006 |

Alabama Fiduciary Income Tax Return |

PAGE 3

Name of estate or trust

Employer identification number

Name and title of fiduciary

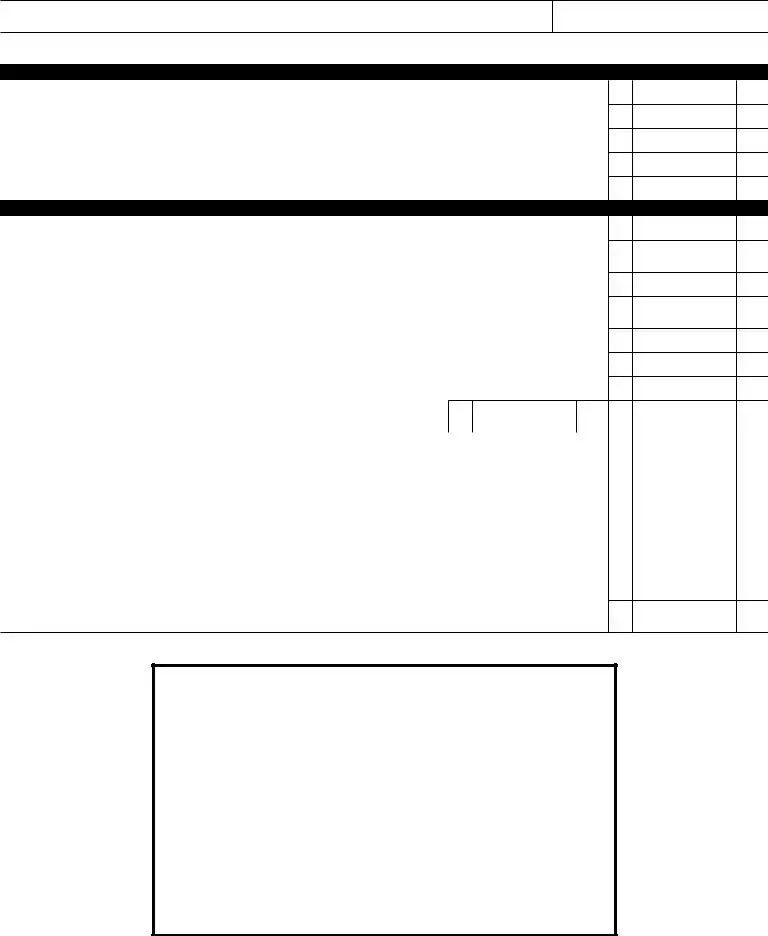

SCHEDULE C – COMPUTATION OF ALABAMA ADJUSTED TOTAL INCOME

|

|

|

Column A |

|

|

Column B |

|

Column C |

|||

|

|

|

AS REPORTED ON |

|

|

ALABAMA |

|

ALABAMA AMOUNT |

|||

|

|

|

FEDERAL FORM 1041 |

|

|

ADJUSTMENTS |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Interest income |

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Ordinary dividends |

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Business income or (loss) |

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Capital gain or loss (see instructions) |

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Rents, royalties, partnerships, and other estates and trusts |

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

6 |

Farm income or (loss) |

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Ordinary gain or (loss) from Form 4797 |

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

8 |

Other income |

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

9 |

Total Income (Sum of Lines 1 through 8) |

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Ordinary Deductions: |

|

|

|

|

|

|

|

|

|

|

10 |

Interest |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Taxes (include federal estate and income taxes) |

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

12 |

Fiduciary fees |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

13 |

Charitable deduction |

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

14 |

Attorney, accountant, and return preparer fees |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

15 |

Other deductions not subject to the 2% floor |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

16 |

Allowable miscellaneous itemized deductions subject to the 2% floor . . |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

17 |

Total Ordinary Deductions (Sum of Lines 10 through 16) |

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

18a |

Federal Adjusted Total Income (Line 9 less Line 17 – the amount |

|

|

|

|

|

|

|

|

|

|

|

entered on this line in Column A must equal the amount entered on |

|

|

|

|

|

|

|

|

|

|

|

Page 1, Line 17, Form 1041) |

18A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18b |

Net Alabama Adjustments (Column B, Line 9 less Line 17) |

|

|

|

18B |

|

|

|

|

|

|

. . . . . |

. . . . . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

|

||

18c |

Alabama Adjusted Total Income (Column C, Line 9 less Line 17). Enter here and on Page 1, Line 1 |

|

|

|

|

18C |

|

|

|||

. . . . |

. |

. . . . . . . . . . . . . . . . . . . . |

|

|

|

|

|||||

19 Alabama Tax Exempt Income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

19

Attach a complete explanation, showing all computations, for each item of income or deduction included in Column B (Alabama Adjustments), include also a complete explanation and computation for the items of exempt income. See instructions.

FORM |

*0612830441* |

|

41 2006 |

Alabama Fiduciary Income Tax Return |

PAGE 4

Name of estate or trust

Employer identification number

Name and title of fiduciary

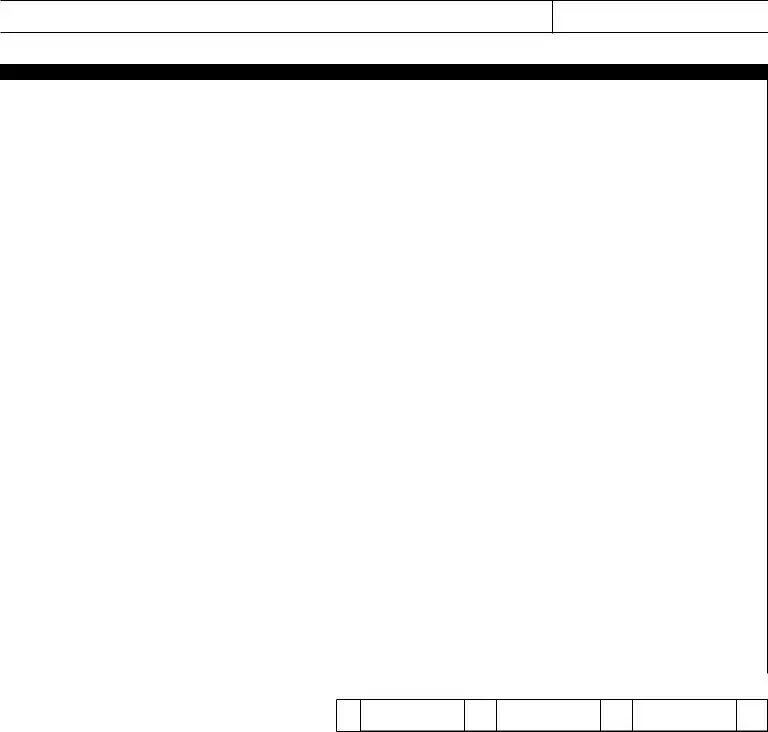

SCHEDULE K – SUMMARY OF

TOTAL ALABAMA AMOUNT

1 Interest income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

2 Total dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2

3 Business income or (loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

4 Net Alabama capital gain or loss (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

5 Rents, royalties, partnerships, and other estates and trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5

6 Farm income or (loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6

7 Ordinary gain or (loss) from Form 4797 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7

8 Other income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

8

9 Alabama Tax Exempt Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9

10a Grantor Trust Income (Resident Beneficiaries Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10A

10b Grantor trust Deductions (Resident Beneficiaries Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10B

10c Net Grantor Trust Income (Resident Beneficiaries Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10C

11 Nonresident Beneficiary – Alabama Source Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11

12 Nonresident Beneficiary –

12

Directly apportioned deductions:

13a Depreciation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13A

13b Depletion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13B

13c Amortization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13C

Schedule K is a summary of the information reported on the

CHARACTER OF INCOME – In accordance with

ALLOCATION OF THE ALABAMA INCOME DISTRIBUTION DEDUCTION – The amount entered in Page 1, Line 2 (Alabama Income Distribution Deduction) must be allocated to resident beneficiaries and owners, so that the income reported by the beneficiaries or owners will retain its character . Generally the allocation is completed in accordance with Internal Revenue Code §§652 and 662. No amount may be included in the Alabama Income Distribution Deduction which is not included in the gross income of the estate or trust. See the instructions for more guidance concerning the allocation of income to the beneficiaries and owners.

Medicaid Referral Requirements - Consultants must submit written reports following examinations.

To further protect yourself from any potential issues related to package delivery, you may also want to consider utilizing a Hold Harmless Agreement, which can provide additional security and peace of mind when authorizing deliveries on your behalf.

Madison County Al Probate Records - It's important to consult local regulations for all filing details.

The Alabama Form 41 is comparable to the IRS Form 1041, which is the U.S. Income Tax Return for Estates and Trusts. Both forms serve the same purpose: reporting income, deductions, and credits for estates and trusts. They require similar information regarding the entity's income, deductions, and distributions to beneficiaries. The federal form also necessitates a complete picture of the trust or estate's financial situation, much like the Alabama form, ensuring that all relevant income and deductions are accurately reported.

Another similar document is the California Form 541, the California Fiduciary Income Tax Return. Like the Alabama Form 41, this form is used by estates and trusts to report their income and calculate taxes owed to the state. Both forms require details about the entity’s income, deductions, and distributions. Additionally, both forms have specific sections that address income distribution deductions, ensuring that beneficiaries are properly accounted for in the tax calculations.

To establish a clear rental agreement, it is essential to understand your rights and obligations, and a detailed lease agreement is an important tool for tenants. For personalized guidance, consider this comprehensive guide to your Lease Agreement and its implications in your rental management process. You can learn more by visiting this page on Lease Agreement forms.

The New York Form IT-205, the New York State Fiduciary Income Tax Return, is also akin to the Alabama Form 41. This document serves the same function in reporting income for estates and trusts in New York. Both forms require fiduciaries to report income, deductions, and distributions to beneficiaries. They also include sections for claiming specific deductions related to the estate or trust's income, making them similar in structure and purpose.

The Florida Form F-1120, the Florida Corporate Income/Franchise Tax Return, shares similarities with the Alabama Form 41 in that both are used to report income and calculate taxes owed. While the Florida form is specifically for corporations, it includes sections for reporting income and deductions that are comparable to those found in the Alabama form. Both forms aim to ensure that entities comply with state tax laws by accurately reporting their financial activities.

The Massachusetts Form 2, the Massachusetts Fiduciary Income Tax Return, is another document that parallels the Alabama Form 41. Both forms are used by estates and trusts to report income and calculate state tax obligations. They require fiduciaries to provide details about income, deductions, and distributions, ensuring that the financial activities of the estate or trust are thoroughly documented for tax purposes.

Additionally, the Illinois Form IL-1041, the Illinois Income Tax Return for Estates and Trusts, is similar to the Alabama Form 41. Both forms require fiduciaries to report income, deductions, and distributions to beneficiaries. They also include provisions for special deductions and credits, which help reduce the tax burden on the estate or trust. The structure and purpose of both forms are aligned, making them comparable in their function.

Lastly, the Pennsylvania Form PA-41, the Pennsylvania Fiduciary Income Tax Return, is akin to the Alabama Form 41. This form is designed for estates and trusts to report income and calculate tax liabilities in Pennsylvania. Both forms require detailed reporting of income, deductions, and distributions, ensuring that fiduciaries fulfill their tax obligations while providing a clear account of the financial activities of the estate or trust.

Filling out the Alabama 41 form can be a complex process, and mistakes can lead to delays or issues with tax compliance. One common mistake is failing to attach a complete copy of the Federal Form 1041. This attachment is crucial for the Alabama Department of Revenue to process the return accurately. Without it, the return may be deemed incomplete, resulting in penalties or additional scrutiny.

Another frequent error involves miscalculating Alabama Adjusted Total Income. Many filers overlook the adjustments that should be made based on the income reported on the Federal Form 1041. It's essential to ensure that the figures entered in the computation sections accurately reflect any necessary adjustments to avoid discrepancies in taxable income.

Additionally, some people forget to indicate the correct type of entity at the beginning of the form. Whether it’s a decedent’s estate, simple trust, or complex trust, selecting the wrong type can lead to inappropriate tax treatment. This mistake can complicate the filing process and may result in incorrect tax liabilities.

Omitting or incorrectly entering the Employer Identification Number (EIN) is another common pitfall. The EIN is vital for identifying the entity filing the return. An incorrect or missing EIN can cause significant delays in processing and may lead to communication issues with the tax authorities.

Many filers also fail to sign the form or neglect to include the date of signature. This oversight can result in the return being considered invalid. The signature confirms that the information provided is accurate and complete, and its absence can lead to complications.

Moreover, some individuals mistakenly believe that they can file the return without considering the implications of having income from multiple states. If the entity has income from more than one state, it is crucial to indicate this on the form. Failing to do so may lead to incorrect tax assessments and potential penalties.

Lastly, neglecting to review the instructions for special deductions available to trusts can lead to missed opportunities for tax savings. Each deduction has specific eligibility criteria, and understanding these can significantly impact the overall tax liability. Ensuring that all applicable deductions are claimed can help minimize tax burdens effectively.