Fill Out a Valid Alabama 9501 Form

Fill Out a Valid Alabama 9501 Form

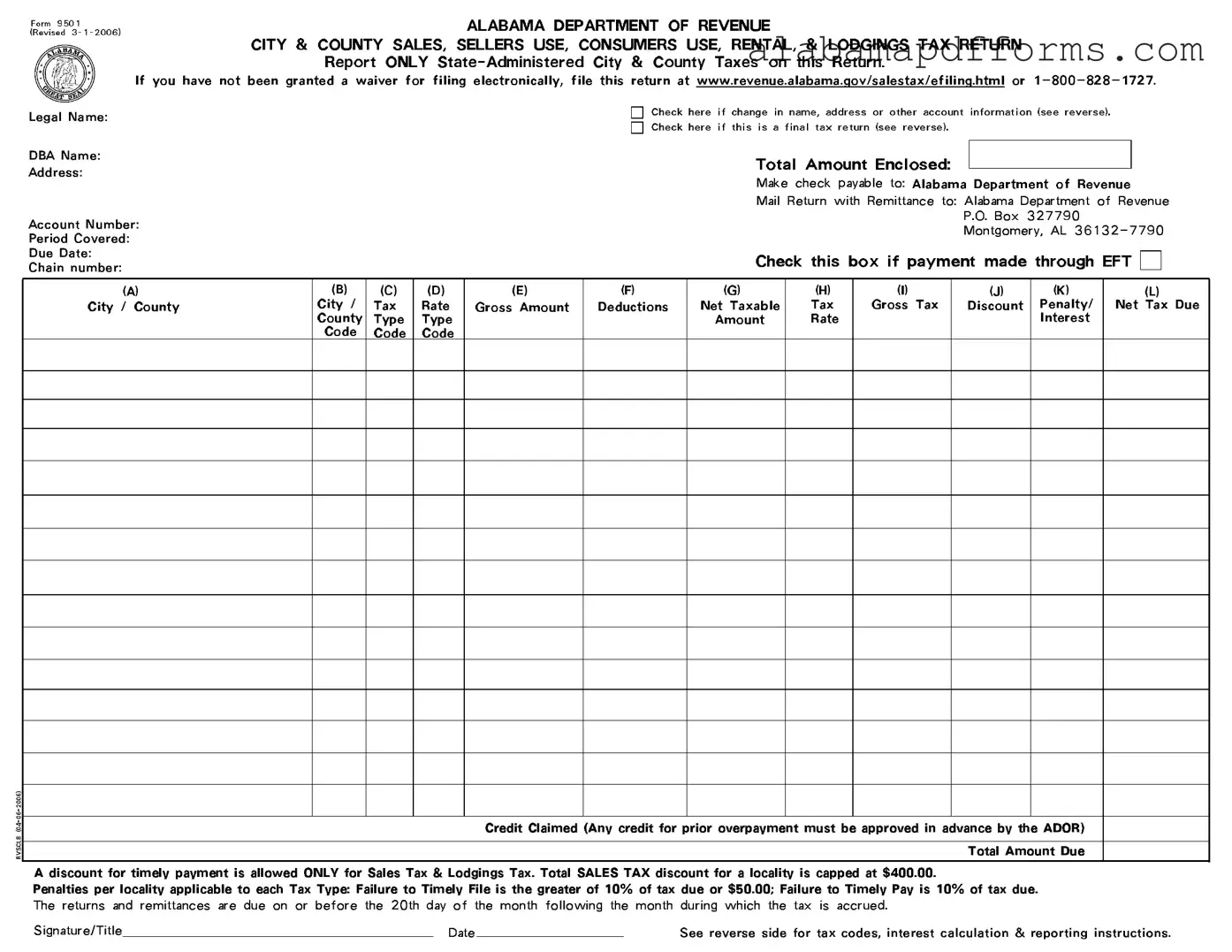

The Alabama 9501 form serves as a crucial document for businesses operating within the state, specifically for reporting various local taxes such as sales, rental, and lodgings taxes. Designed to streamline the tax reporting process, this form requires businesses to provide essential information, including their legal name, address, and account number, as well as details about the tax period covered. Taxpayers must report only state-administered city and county taxes on this return. The form also includes checkboxes for indicating any changes in business name or address and for marking a final tax return. Each section of the form is meticulously structured to capture the necessary data, from gross amounts and deductions to net taxable amounts and applicable tax rates. Timeliness is emphasized, as returns and payments are due by the 20th of the month following the tax accrual. Failure to comply may result in penalties, which vary depending on the nature of the delay. Understanding the intricacies of the Alabama 9501 form is vital for ensuring compliance and avoiding unnecessary financial repercussions.

Below is a list of misconceptions regarding the Alabama 9501 form, along with clarifications for each:

This form is required for any business that collects state-administered city and county taxes, regardless of size.

Even businesses operating online or from out of state must file the Alabama 9501 form if they collect applicable taxes from Alabama customers.

Timely filing is crucial. Returns and payments are due by the 20th of the month following the tax period to avoid penalties.

Discounts are only available for sales tax and lodgings tax, with specific caps on the amount that can be claimed.

Any changes must be reported on the form to ensure that tax records remain accurate.

Credits for prior overpayments can be claimed, but they must be approved in advance by the Alabama Department of Revenue.

It is essential to refer to the Local Tax Rate Schedule or contact the Alabama Department of Revenue to ensure accurate reporting.

Alabama Environment - This form is revised periodically to meet current Medicaid policies and requirements.

Tuscaloosa Small Claims Court - Every claim submitted must be factually correct to ensure proper legal proceedings.

Completing a Colorado Do Not Resuscitate Order form is essential for individuals who wish to communicate their end-of-life preferences clearly. By signing this document, patients can ensure that their wishes regarding resuscitation are honored in critical situations, providing peace of mind for both themselves and their loved ones. For more information on how to obtain this vital document, you can visit Colorado PDF Forms.

Alabama Poa - Proper usage of this form can result in a more streamlined experience when handling vehicle transactions.

The Alabama 9501 form is similar to the IRS Form 1040, which is the standard individual income tax return. Both documents require taxpayers to report their income and calculate taxes owed. Just as the Alabama 9501 form collects specific information about state-administered taxes, the IRS Form 1040 gathers data on federal income taxes. Both forms require personal information, such as name and address, and include sections for deductions and credits, allowing taxpayers to reduce their tax liability. Completing either form accurately is essential to avoid penalties and ensure compliance with tax laws.

Another document similar to the Alabama 9501 form is the California Sales and Use Tax Return (Form BOE-401-A). This form serves a similar purpose by requiring businesses to report sales and use tax collected in California. Like the Alabama 9501, it includes sections for gross sales, deductions, and the calculation of net tax due. Both forms also provide a mechanism for taxpayers to claim discounts for timely payment, thereby incentivizing prompt remittance. The structure and requirements of these forms reflect the need for transparency and accuracy in tax reporting across different states.

The New York State Sales and Use Tax Return (Form ST-100) is another comparable document. This form is used by businesses to report sales and use taxes collected in New York. Similar to the Alabama 9501, it requires detailed reporting of sales amounts, deductions, and the calculation of taxes owed. Both forms include instructions for taxpayers to follow, ensuring they understand how to complete their returns correctly. The emphasis on accurate reporting and timely payment is a common theme across these tax forms, highlighting the importance of compliance with state tax regulations.

In addition, the Florida Sales and Use Tax Return (Form DR-15) bears similarities to the Alabama 9501 form. Businesses in Florida use this form to report sales tax and remit payments to the state. Like the Alabama form, it includes sections for gross sales, deductions, and tax rates. Both documents require businesses to be diligent in reporting their tax obligations accurately. The penalties for late filing or payment are also comparable, underscoring the importance of adhering to deadlines to avoid additional fees.

The Texas Sales and Use Tax Return (Form 01-114) is another document that shares characteristics with the Alabama 9501 form. This form is utilized by Texas businesses to report sales and use tax. Both forms require similar information, including gross sales, deductions, and the calculation of net tax due. They also provide guidance on penalties for late submissions. The similarities in structure and required information illustrate the common framework of state tax reporting, aimed at ensuring compliance and accountability among businesses.

The Illinois Sales and Use Tax Return (Form ST-1) is also comparable to the Alabama 9501 form. This form requires businesses to report their sales and use tax obligations in Illinois. Like the Alabama form, it includes fields for gross sales, allowable deductions, and tax calculations. Both forms emphasize the need for accurate reporting to avoid penalties and ensure compliance with state tax laws. The design and requirements of these forms reflect the shared goal of facilitating proper tax administration across states.

For those looking to ensure a smooth transaction, understanding the important aspects of a comprehensive Motor Vehicle Bill of Sale is critical. This form not only documents the sale but also protects the interests of both buyer and seller, making it a vital tool in the vehicle transfer process.

Lastly, the Pennsylvania Sales and Use Tax Return (Form REV-183) is similar to the Alabama 9501 form. Businesses in Pennsylvania use this form to report their sales and use tax. Similar to the Alabama form, it includes sections for gross sales, deductions, and the calculation of taxes owed. Both forms highlight the importance of timely filing and accurate reporting, with penalties in place for late submissions. This commonality reinforces the necessity for businesses to maintain compliance with state tax regulations, regardless of their location.

Filling out the Alabama 9501 form can be a straightforward process, but there are common mistakes that individuals and businesses often make. One frequent error is neglecting to update personal information. If there has been a change in your legal name, address, or other account details, it is essential to check the corresponding box on the form. Failing to do so may result in delays or complications in processing your return.

Another common mistake involves miscalculating tax amounts. When entering figures in the Gross Amount and Deductions columns, accuracy is crucial. Double-check your calculations to ensure that the Net Taxable Amount is correct. Errors in these calculations can lead to either underpayment or overpayment, both of which can have financial repercussions.

Many people also overlook the requirement to include the correct City/County Code. Each city and county in Alabama has a unique code, which must be accurately entered in the appropriate section of the form. If you are unsure of the code, resources are available through the Alabama Department of Revenue. Not using the correct code can lead to the rejection of your return.

Additionally, individuals often forget to sign and date the form before submission. This step may seem minor, but it is a critical part of the process. A missing signature can result in the return being considered incomplete, which may delay processing and lead to penalties.

Lastly, many filers neglect to verify the due date for their submission. The returns and payments are due on or before the 20th day of the month following the month in which the tax was accrued. Missing this deadline can incur penalties and interest charges, adding unnecessary stress to an already complicated process.