Fill Out a Valid Alabama 96 Form

Fill Out a Valid Alabama 96 Form

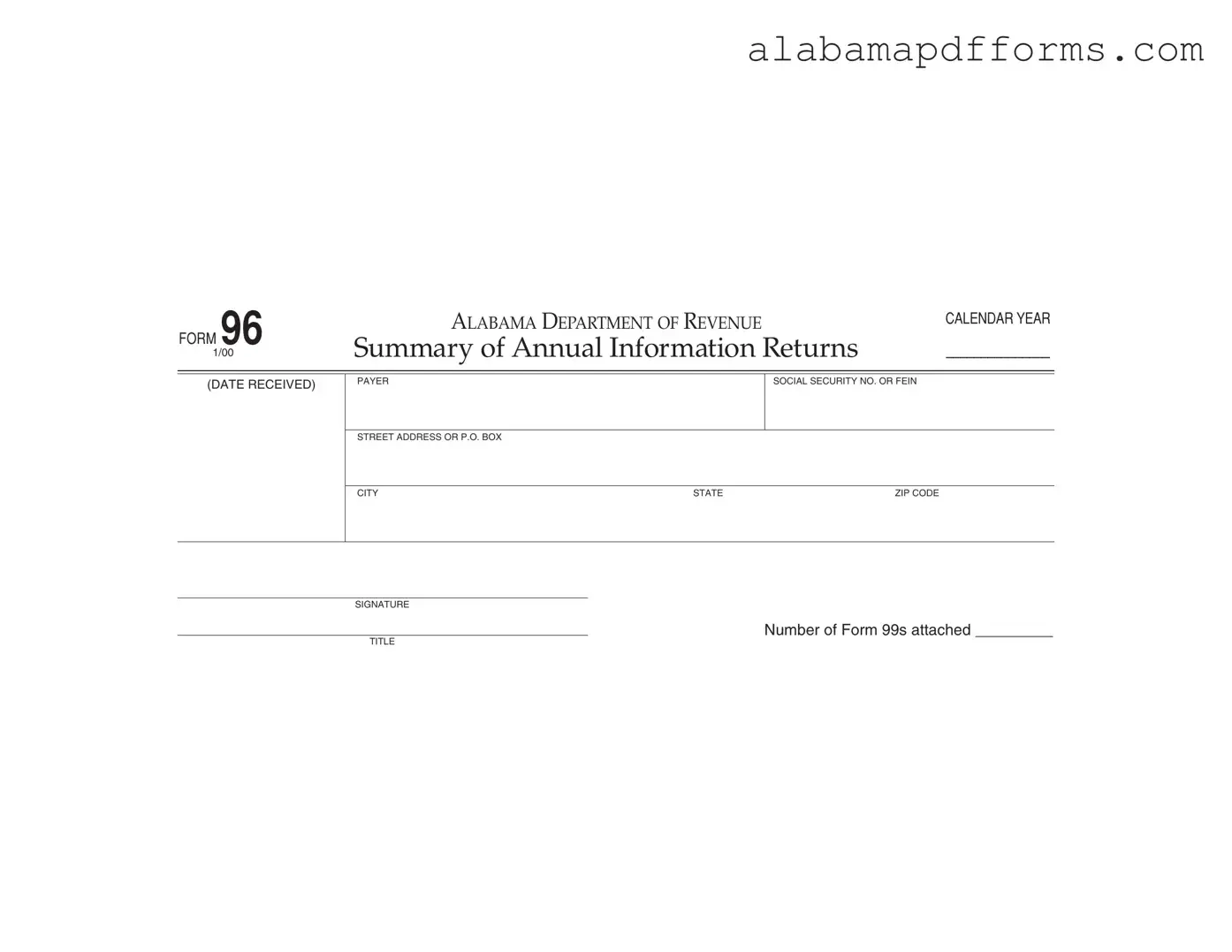

The Alabama 96 form serves as a vital tool for reporting annual information returns to the Alabama Department of Revenue. This form is essential for any individual, corporation, association, or agent that makes payments of $1,500 or more in gains, profits, or income to a taxpayer subject to Alabama income tax during the calendar year. It requires the payer to provide specific details, including their Social Security number or Federal Employer Identification Number (FEIN), as well as their address information. Additionally, the form must indicate the number of Form 99s attached, which are required for reporting these payments. It is crucial to note that if Alabama income tax has been withheld from the payments, the filer must use Form A-3 instead of the Alabama 96. The deadline for submitting this form is March 15 of the following year, ensuring that all payments made during the previous calendar year are reported in a timely manner. For those who have voluntarily withheld Alabama income tax, filing Form 99 or an approved substitute is mandatory, regardless of the payment amount. Understanding the Alabama 96 form is essential for compliance and proper tax reporting in the state.

Misconceptions about the Alabama 96 form can lead to confusion and potential compliance issues. Here are ten common misconceptions clarified:

Understanding these misconceptions can help ensure compliance with Alabama tax regulations and avoid unnecessary complications.

FORM 96 |

ALABAMA DEPARTMENT OF REVENUE |

CALENDAR YEAR |

|

|

|

1/00 |

Summary of Annual Information Returns |

_______________ |

(DATE RECEIVED)

PAYER

SOCIAL SECURITY NO. OR FEIN

STREET ADDRESS OR P.O. BOX

CITY |

STATE |

ZIP CODE |

SIGNATURE

NUMBER OF FORM 99S ATTACHED _________

TITLE

Instructions

Information returns on Form 99 must be filed by every resident individual, corporation, association or agent making payment of gains, profits or income (other than interest coupons payable to bearer) of $1,500.00 or more in any calendar year to any taxpayer subject to Alabama income tax. If you have voluntarily withheld Alabama income tax from such payments, you must file Form 99 or approved substitute regardless of the amount of the payment. Employers filing Form

Returns must be filed with the Alabama Department of Revenue for each calendar year on or before March 15 of the following year.

Mail to: Alabama Department of Revenue |

NOTE: IF ALABAMA INCOME TAX HAS BEEN WITHHELD ON FORM 99 |

Individual & Corporate Tax Division |

DO NOT USE THIS FORM; USE FORM |

P.O. Box 327489 |

OF ALABAMA INCOME TAX WITHHELD. |

Montgomery, AL |

|

Alabama Wage and Labor Law - Minors aged 14 and 15 have detailed restrictions on working hours during the school year, promoting their welfare.

In order to ensure protection for all parties involved, utilizing a Release of Liability form is essential, which often accompanies a Hold Harmless Agreement. This legal document clearly outlines that one party will not be held accountable for any mishaps or damages that occur during activities that involve certain risks, such as sports or volunteering. By signing this form, participants confirm their awareness of potential risks and their decision to proceed with the activity voluntarily.

Vin Check Alabama - Exceptions include registration renewals and vehicles registered under specific provisions of Alabama law.

Alabama Lost Title - Montgomery, Alabama, is where the Alabama Department of Revenue processes the MVT 4-1 applications.

The Alabama Form 99 is closely related to the Alabama 96 form as both are used for reporting income payments to the state. Form 99 specifically requires individuals and entities to report payments of $1,500 or more made to Alabama taxpayers. This form is crucial for ensuring that the state collects the appropriate income tax from individuals who receive substantial payments. Just like the Alabama 96 form, which summarizes these annual returns, Form 99 must be filed annually and is due by March 15 of the following year. Both forms help maintain accurate records for tax purposes and ensure compliance with state tax laws.

Another document similar to the Alabama 96 form is the IRS Form 1099. This federal form is used to report various types of income other than wages, salaries, and tips. Just as the Alabama 96 form summarizes annual information returns, Form 1099 provides detailed information about payments made to individuals, including independent contractors and freelancers. The IRS requires that Form 1099 be issued for payments exceeding $600, which aligns with the reporting requirements of the Alabama 96. Both forms serve the purpose of tracking income and ensuring that taxes are paid accordingly.

The IRS Form W-2 is another document that shares similarities with the Alabama 96 form. While W-2 is specifically for reporting wages paid to employees, it also plays a vital role in income reporting. Employers must provide W-2 forms to their employees at the end of the year, detailing the income earned and taxes withheld. Like the Alabama 96, W-2 forms help the state and federal government track income and ensure compliance with tax obligations. Both forms must be filed annually and are critical for accurate income reporting.

The Alabama A-3 form is yet another document that parallels the Alabama 96 form. This form is used for the annual reconciliation of Alabama income tax withheld from employee wages. Employers who have withheld state income tax from their employees must file this form to summarize the total amount withheld for the year. Similar to the Alabama 96, the A-3 form ensures that the state receives accurate information regarding tax withholdings, thereby facilitating proper tax collection and compliance.

For landlords and tenants seeking to formalize their rental agreements, understanding the importance of a well-prepared Lease Agreement template is essential. This document lays out the rental terms in a clear manner to foster mutual understanding and protect both parties involved. For more information on this crucial process, check out this helpful Lease Agreement resource.

The IRS Form 945 is also relevant in this context, as it is used to report federal income tax withheld from nonpayroll payments. This includes payments made to independent contractors and other non-employees. Like the Alabama 96 form, which summarizes various payments made throughout the year, Form 945 serves a similar function at the federal level. Both forms ensure that the appropriate taxes are reported and remitted to the government, thereby maintaining compliance with tax laws.

Another important document is the Alabama Form 40, which is the state's individual income tax return. While the Alabama 96 form summarizes information returns, Form 40 is where individuals report their total income, deductions, and tax liability. Both forms are essential for tax compliance, but they serve different purposes in the tax reporting process. The Alabama 96 aids in the reporting of payments made, while Form 40 focuses on the individual's overall tax situation.

The IRS Schedule C is also similar to the Alabama 96 form, particularly for self-employed individuals. Schedule C is used to report income or loss from a business operated as a sole proprietorship. Just as the Alabama 96 form summarizes payments made to individuals, Schedule C summarizes income earned by self-employed individuals. Both documents are crucial for reporting income accurately and ensuring that the appropriate taxes are calculated and paid.

Form 1040, the U.S. Individual Income Tax Return, can also be compared to the Alabama 96 form. While the Alabama 96 focuses on reporting specific payments made to individuals, Form 1040 is the comprehensive tax return that individuals file to report their overall income and tax liability. Both forms play a critical role in the tax reporting process, with the Alabama 96 providing detailed information that contributes to the figures reported on Form 1040.

The IRS Form 1098 is another relevant document, as it is used to report mortgage interest paid by individuals. Similar to the Alabama 96 form, which summarizes various income payments, Form 1098 provides important information that can affect an individual's tax return. Both forms are essential for accurate tax reporting and compliance, ensuring that taxpayers receive the appropriate deductions and credits.

Lastly, the Alabama Form 40NR is similar in that it is used by non-residents filing income tax returns in Alabama. Like the Alabama 96 form, which deals with reporting payments made to Alabama taxpayers, Form 40NR is focused on ensuring that non-residents pay the correct amount of tax on income earned within the state. Both forms are vital for maintaining accurate tax records and ensuring compliance with Alabama's tax laws.

Filling out the Alabama 96 form can be straightforward, but many people make common mistakes that can lead to issues down the line. One frequent error is not including the correct payer's Social Security Number or Federal Employer Identification Number (FEIN). This number is crucial for identifying the payer and ensuring that the information is processed correctly.

Another mistake often seen is failing to provide a complete address. The form requires the street address or P.O. Box, city, state, and zip code. Omitting any of these details can delay processing or cause confusion regarding the payer's identity.

Many individuals overlook the importance of signing the form. A signature is necessary to validate the information provided. Without it, the form may be considered incomplete, leading to potential penalties or rejection by the Alabama Department of Revenue.

Additionally, some filers forget to indicate the number of Form 99s attached. This information is essential for the Department to assess the total payments reported. Neglecting to include this detail can result in an inaccurate filing and further complications.

People sometimes misinterpret the instructions regarding withholding Alabama income tax. If tax has been withheld, it is crucial to use the appropriate form, such as Form A-3, instead of the Alabama 96 form. Misusing forms can lead to filing errors and may trigger audits.

Another common mistake is not adhering to the filing deadline. The form must be submitted by March 15 of the following year. Late submissions can incur penalties, so it’s important to mark the date on your calendar.

Some filers also fail to keep copies of their submitted forms and any attachments. Having these records can be invaluable if questions arise in the future or if there is a need to verify information.

Incorrectly reporting the amounts paid is another frequent error. The form requires accurate figures for payments made during the calendar year. Double-checking these amounts can prevent discrepancies that might lead to audits.

Finally, many individuals do not seek help when they are unsure about how to fill out the form. Consulting with a tax professional or using reliable resources can provide clarity and help avoid mistakes. Taking the time to understand the requirements can save a lot of trouble later on.