Fill Out a Valid Alabama A 1 Form

Fill Out a Valid Alabama A 1 Form

The Alabama A-1 form is an essential document for employers in Alabama, serving as the Employer’s Quarterly Return of Income Tax Withheld. This form must be submitted by the last day of the month following the end of each quarter, ensuring timely reporting of income tax withheld from employees’ wages. New employers are required to obtain a withholding tax account number before filing. While personalized coupons are typically provided to facilitate the filing process, blank forms can be used if necessary. Employers must indicate if the A-1 form is a final return by marking an “X” if they have ceased withholding Alabama income tax. The form includes several lines for reporting key information, such as the number of employees, total income tax withheld, and any penalties or interest incurred due to late filing or payment. Additionally, employers may claim credits for overpayments from previous periods. Proper completion and timely submission of the A-1 form are crucial to avoid penalties and ensure compliance with Alabama tax regulations.

Understanding the Alabama A-1 form is crucial for employers who withhold income tax from their employees. However, several misconceptions can lead to confusion. Below is a list of common misunderstandings about the Alabama A-1 form, along with clarifications.

The A-1 form must be submitted by the last day of the month following the end of the quarter. For example, if the quarter ends on March 31, the form is due by April 30.

New employers are required to apply for a withholding tax account number through the Alabama Department of Revenue's website before they can file the A-1 form.

Blank forms should only be used when personalized coupons cannot be obtained in time. Employers typically receive personalized coupons that contain their specific information.

If an employer ceases to withhold Alabama income tax, they must indicate this by placing an "X" on Line 1 of the A-1 form to signify a final return.

Late filing incurs a penalty of 10% of the tax due or a minimum of $50. Additionally, late payments also attract a 10% penalty, and both penalties can be combined if applicable.

The interest rate for late payments is variable and is determined based on federal tax deficiencies. Employers should check with the Withholding Tax Section for the current rate.

The amount remitted must correspond to the calculations on Line 8. If the remitted amount differs, a detailed explanation must accompany the return.

Payments must be mailed to the specified address: Income Tax Administration Division, Withholding Tax Section, P.O. Box 327483, Montgomery, AL 36132-7483.

All employers who withhold Alabama income tax, regardless of the number of employees, are required to file the A-1 form.

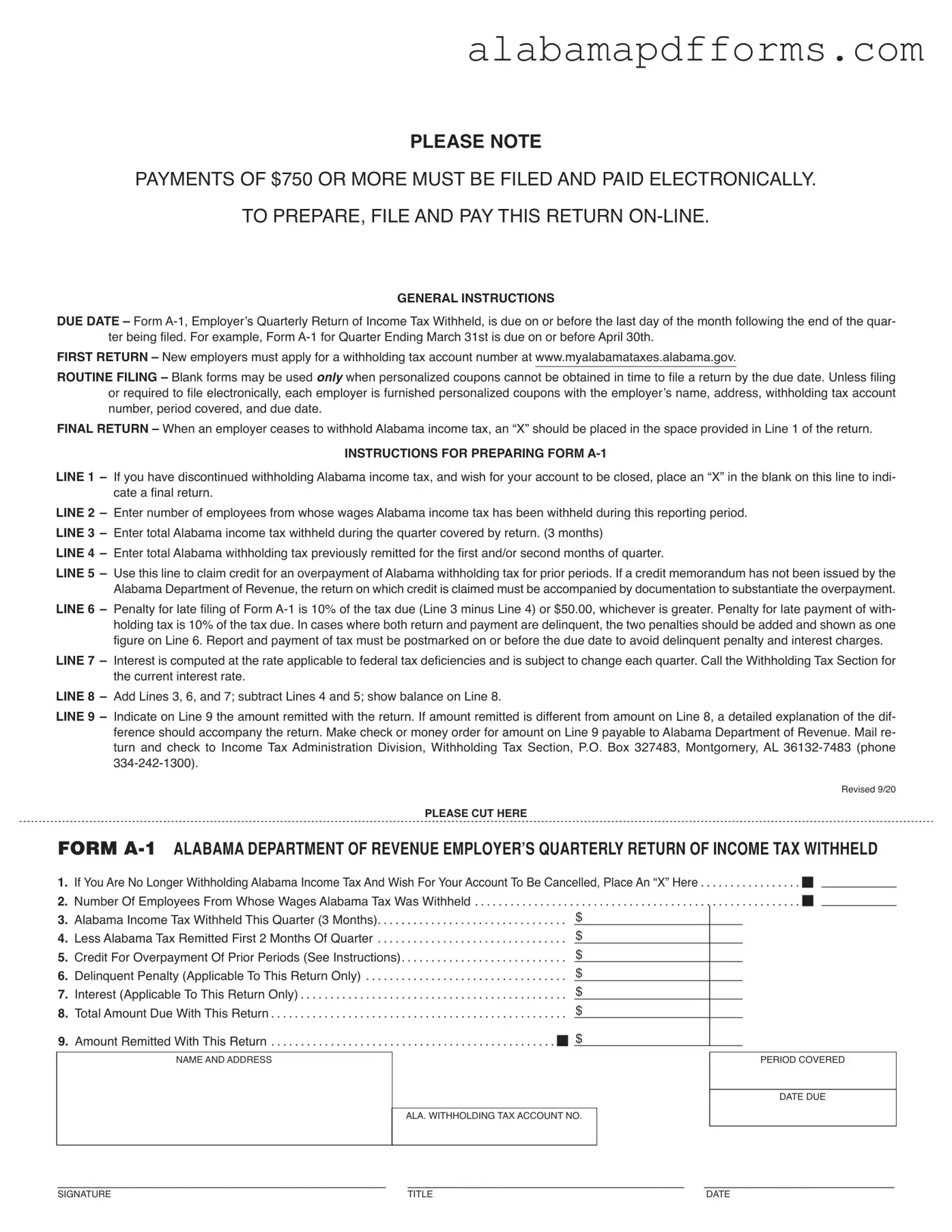

PLEASE NOTE

PAYMENTS OF $750 OR MORE MUST BE FILED AND PAID ELECTRONICALLY.

TO PREPARE, FILE AND PAY THIS RETURN

GENERAL INSTRUCTIONS

DUE DATE – Form

FIRST RETURN – New employers must apply for a withholding tax account number at www.myalabamataxes.alabama.gov.

ROUTINE FILING – Blank forms may be used only when personalized coupons cannot be obtained in time to file a return by the due date. Unless filing or required to file electronically, each employer is furnished personalized coupons with the employer’s name, address, withholding tax account number, period covered, and due date.

FINAL RETURN – When an employer ceases to withhold Alabama income tax, an “X” should be placed in the space provided in Line 1 of the return.

INSTRUCTIONS FOR PREPARING FORM

LINE 1 – If you have discontinued withholding Alabama income tax, and wish for your account to be closed, place an “X” in the blank on this line to indi- cate a final return.

LINE 2 – Enter number of employees from whose wages Alabama income tax has been withheld during this reporting period. LINE 3 – Enter total Alabama income tax withheld during the quarter covered by return. (3 months)

LINE 4 – Enter total Alabama withholding tax previously remitted for the first and/or second months of quarter.

LINE 5 – Use this line to claim credit for an overpayment of Alabama withholding tax for prior periods. If a credit memorandum has not been issued by the Alabama Department of Revenue, the return on which credit is claimed must be accompanied by documentation to substantiate the overpayment.

LINE 6 – Penalty for late filing of Form

LINE 7 – Interest is computed at the rate applicable to federal tax deficiencies and is subject to change each quarter. Call the Withholding Tax Section for the current interest rate.

LINE 8 – Add Lines 3, 6, and 7; subtract Lines 4 and 5; show balance on Line 8.

LINE 9 – Indicate on Line 9 the amount remitted with the return. If amount remitted is different from amount on Line 8, a detailed explanation of the dif- ference should accompany the return. Make check or money order for amount on Line 9 payable to Alabama Department of Revenue. Mail re- turn and check to Income Tax Administration Division, Withholding Tax Section, P.O. Box 327483, Montgomery, AL

Revised 9/20

PLEASE CUT HERE

FORM

1. If You Are No Longer Withholding Alabama Income Tax And Wish For Your Account To Be Cancelled, Place An “X” Here . . . . . . . . . . . . . . . . . y

2. Number Of Employees From Whose Wages Alabama Tax Was Withheld . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . y 3. Alabama Income Tax Withheld This Quarter (3 Months). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

4. Less Alabama Tax Remitted First 2 Months Of Quarter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

5. Credit For Overpayment Of Prior Periods (See Instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . $

6. Delinquent Penalty (Applicable To This Return Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

7. Interest (Applicable To This Return Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

8. Total Amount Due With This Return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

9. Amount Remitted With This Return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . y $

NAME AND ADDRESS |

PERIOD COVERED |

DATE DUE

ALA. WITHHOLDING TAX ACCOUNT NO.

______________________________________ ________________________________ ______________________

SIGNATURE |

TITLE |

DATE |

Alabama Court Forms - This process aims to ensure that children receive financial support consistently.

For those seeking to streamline their employment verification process, understanding the key elements of the Employment Verification form guide is paramount. This form plays a vital role in validating an employee's work history and can significantly assist in various scenarios, including securing loans or housing. By ensuring accurate completion and timely submission, both employers and employees can facilitate smoother transitions during these important processes.

Alabama Court Forms - This form protects the rights of defendants during the bail process.

Alabama Ppt - Failure to attach necessary supporting documents can invalidate a claim for deduction.

The Alabama A-1 form is similar to the IRS Form 941, which is the Employer's Quarterly Federal Tax Return. Both forms require employers to report the taxes withheld from employees' wages. Employers must file Form 941 quarterly, just like the A-1, and both forms include sections for reporting the number of employees and the total amount of taxes withheld during the quarter. The penalties for late filing and payment are also comparable, emphasizing the importance of timely submissions to avoid additional costs.

In navigating the complexities of legal agreements, the Hold Harmless Agreement serves as an essential tool for protecting parties from potential liabilities that may arise from various activities or transactions, similar to how various tax forms manage reporting obligations and financial protections for employers.

Another document that shares similarities with the Alabama A-1 form is the IRS Form 944. This form is designed for smaller employers who file annually rather than quarterly. Like the A-1, Form 944 requires employers to report withheld income tax and Social Security and Medicare taxes. While the frequency of filing differs, both forms serve the same purpose of ensuring that employers accurately report and remit taxes withheld from employee wages.

The Alabama A-1 form is also akin to the California Form DE 9, which is the Quarterly Contribution Return and Report of Wages. This form is used to report wages paid and the state payroll taxes withheld. Both forms require detailed information about the number of employees and the total taxes withheld, ensuring compliance with state tax laws. The deadlines for filing are also similar, requiring employers to submit these forms promptly to avoid penalties.

Additionally, the New York State Form NYS-1, the Quarterly Combined Withholding, Wage Reporting, and Unemployment Insurance Return, is comparable to the Alabama A-1 form. Employers in New York must report wages and withholding for state taxes quarterly. Both forms ask for information on the number of employees and total tax withheld, and both have strict deadlines for submission to prevent penalties.

The Texas Form C-3, which is the Employer's Quarterly Report, is another document similar to the Alabama A-1 form. Employers use this form to report wages paid and taxes withheld for state unemployment tax. Like the A-1, the C-3 requires reporting on the number of employees and total taxes withheld, and both forms emphasize the importance of timely filing to avoid penalties.

The Florida Form RT-6, also known as the Employer's Quarterly Report, resembles the Alabama A-1 form as well. This form is used to report wages and taxes withheld for state unemployment compensation. Both forms require detailed information about employees and the total amount withheld, and they both carry deadlines that, if missed, can result in penalties for the employer.

Another related document is the Illinois Form UI-3/40, which is the Employer's Contribution and Wage Report. This form is used for reporting wages and unemployment taxes. Like the A-1, it requires information on the number of employees and the total amount of taxes withheld, and it also imposes penalties for late filing, reinforcing the importance of compliance with state regulations.

Lastly, the Pennsylvania Form UC-2 is similar to the Alabama A-1 form. This form is used to report wages and taxes withheld for unemployment compensation. Both require the reporting of employee counts and total taxes withheld. The deadlines for submission are crucial, as both forms impose penalties for late filing, ensuring that employers adhere to state tax obligations.

Completing the Alabama A-1 form requires attention to detail. Many individuals make mistakes that can lead to penalties or delays. Here are seven common errors to avoid.

First, failing to file electronically when the payment exceeds $750 is a significant mistake. The instructions clearly state that payments of this amount or more must be submitted electronically. Ignoring this requirement can result in penalties and complicate the filing process.

Second, many new employers overlook the need to apply for a withholding tax account number. Without this number, the form cannot be properly filled out. Ensure you register at www.myalabamataxes.alabama.gov before attempting to file your return.

Another frequent error occurs with Line 1. Employers who have stopped withholding Alabama income tax must indicate this by placing an "X" in the designated space. Failing to do so may lead to confusion and unnecessary follow-up from the tax authorities.

Inaccuracies in reporting employee numbers on Line 2 can also create issues. Make sure to enter the correct number of employees from whose wages Alabama income tax has been withheld during the reporting period. Double-checking this number can prevent discrepancies later.

Line 3 requires the total Alabama income tax withheld for the quarter. Many individuals miscalculate this figure, leading to incorrect totals on subsequent lines. Always verify your calculations to ensure accuracy.

Another mistake often made involves Line 9, where the amount remitted with the return is indicated. If this amount differs from what is shown on Line 8, a detailed explanation must accompany the return. Failing to provide this information can delay processing and lead to further inquiries.

Lastly, be mindful of deadlines. The A-1 form is due on or before the last day of the month following the quarter being filed. Missing this deadline can result in penalties that compound the stress of filing. Always mark your calendar to ensure timely submission.

By avoiding these common mistakes, you can streamline the filing process and reduce the risk of penalties. Paying close attention to the details will help ensure compliance and peace of mind.