Fill Out a Valid Alabama Cpt Form

Fill Out a Valid Alabama Cpt Form

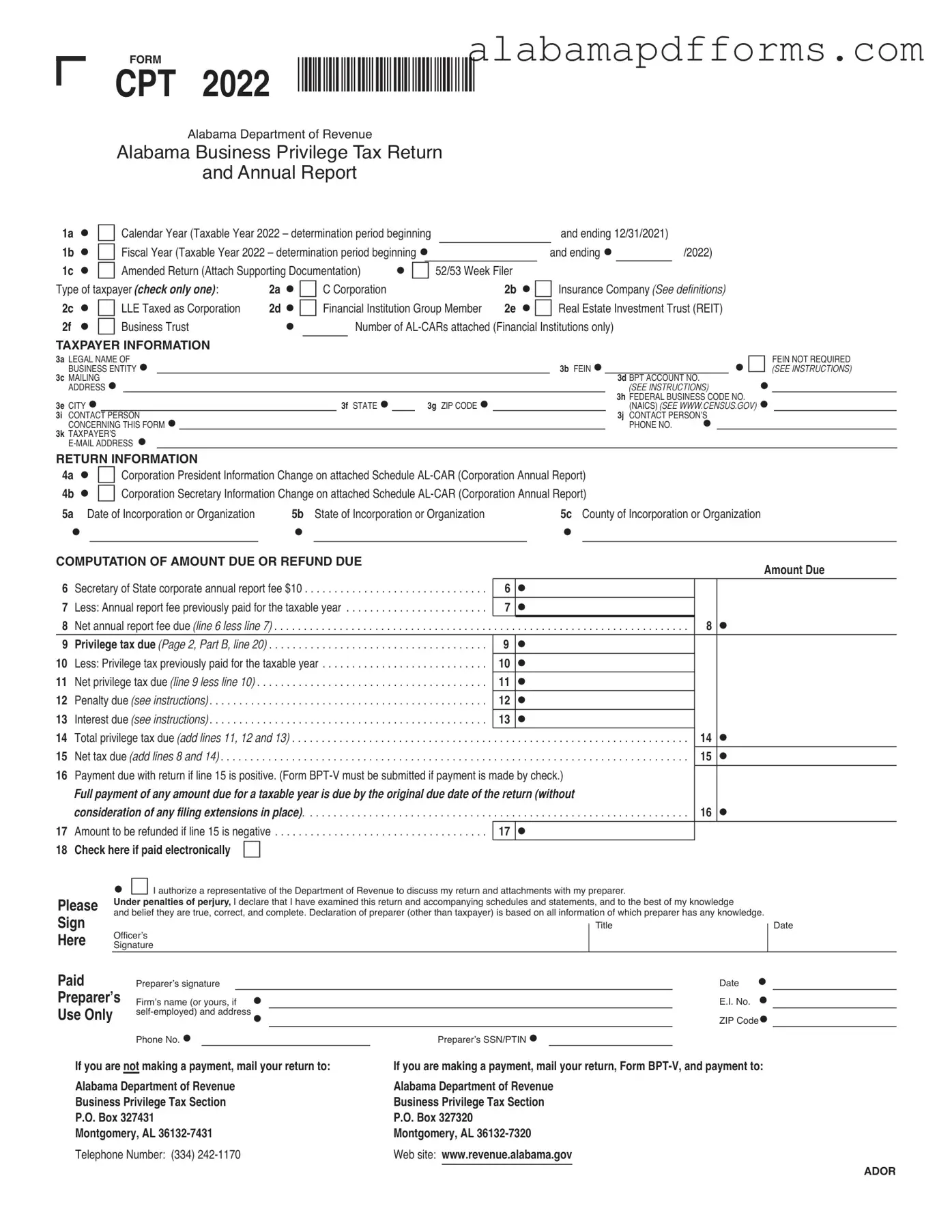

The Alabama CPT form is an essential document for C-Corporations that need to file their Business Privilege Tax Return and Annual Report. This form serves multiple purposes, including providing taxpayer information, detailing the computation of the amount due or any potential refund, and ensuring compliance with Alabama's tax regulations. It requires taxpayers to indicate their type of corporation and specify the determination period, which can be either a calendar year or a fiscal year. The form includes sections for taxpayer information, such as the legal name, Federal Employer Identification Number (FEIN), and mailing address. Additionally, it addresses changes in corporate leadership and whether the return is amended or initial. The computation section breaks down the annual report fee, privilege tax due, penalties, and interest, allowing for a clear calculation of the total amount owed or refunded. Corporations must also provide details on net worth and related exclusions and deductions, which are crucial for determining the taxable amount. Overall, the Alabama CPT form is a comprehensive tool that ensures C-Corporations meet their reporting obligations while accurately calculating their tax liabilities.

Misconceptions about the Alabama CPT form can lead to confusion and potential errors in tax reporting. Below are ten common misconceptions, along with clarifications to help ensure accurate understanding and compliance.

Understanding these misconceptions can help ensure that C-Corporations comply with Alabama's tax requirements effectively and avoid unnecessary complications.

|

FORM |

|

*220001CP* |

|

|

|

|

|

CPT 2022 |

|

|

|

|||

|

Alabama Department of Revenue |

|

|

|

|

||

|

Alabama Business Privilege Tax Return |

|

|

|

|||

|

and Annual Report |

|

|

|

|

||

1a |

6 Calendar Year (Taxable Year 2022 – determination period beginning |

|

and ending 12/31/2021) |

|

|||

1b |

6 Fiscal Year (Taxable Year 2022 – determination period beginning |

|

and ending |

/2022) |

|||

1c |

6 Amended Return (Attach Supporting Documentation) |

6 52/53 Week Filer |

|

|

|||

Type of taxpayer (check only one): |

2a |

6 C Corporation |

|

2b |

6 Insurance Company (See definitions) |

||

2c |

6 LLE Taxed as Corporation |

2d |

6 Financial Institution Group Member |

2e |

6 Real Estate Investment Trust (REIT) |

||

2f |

6 Business Trust |

|

Number of |

|

|||

TAXPAYER INFORMATION

3a |

LEGAL NAME OF |

|

|

|

6 |

FEIN NOT REQUIRED |

|

|

BUSINESS ENTITY |

|

|

3b FEIN |

(SEE INSTRUCTIONS) |

||

3c |

MAILING |

|

|

3d |

BPT ACCOUNT NO. |

|

|

|

ADDRESS |

|

|

|

(SEE INSTRUCTIONS) |

|

|

|

|

|

|

|

3h |

FEDERAL BUSINESS CODE NO. |

|

3e |

CITY |

|

3f STATE |

3g ZIP CODE |

|

(NAICS) (SEE WWW.CENSUS.GOV) |

|

3i |

CONTACT PERSON |

|

|

3j |

CONTACT PERSON’S |

|

|

|

CONCERNING THIS FORM |

|

|

|

PHONE NO. |

|

|

3k |

TAXPAYER’S |

|

|

|

|

|

|

|

|

|

|

|

|

||

RETURN INFORMATION |

|

|

|

|

|

||

4a |

6 Corporation President Information Change on attached Schedule |

|

|

||||

4b |

6 Corporation Secretary Information Change on attached Schedule |

|

|

||||

5a Date of Incorporation or Organization |

5b State of Incorporation or Organization |

5c County of Incorporation or Organization |

|

||||

COMPUTATION OF AMOUNT DUE OR REFUND DUE |

Amount Due |

|

|

|

|

6 Secretary of State corporate annual report fee $10 |

6 |

|

7 Less: Annual report fee previously paid for the taxable year |

7 |

|

8 Net annual report fee due (line 6 less line 7) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 |

|

9 |

Privilege tax due (Page 2, Part B, line 20) |

9 |

10 |

Less: Privilege tax previously paid for the taxable year |

10 |

11 |

Net privilege tax due (line 9 less line 10) |

11 |

12 |

Penalty due (see instructions) |

12 |

13 |

Interest due (see instructions) |

13 |

14 |

Total privilege tax due (add lines 11, 12 and 13) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 |

15 |

Net tax due (add lines 8 and 14) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 |

16Payment due with return if line 15 is positive. (Form

Full payment of any amount due for a taxable year is due by the original due date of the return (without

|

consideration of any filing extensions in place) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 |

17 |

Amount to be refunded if line 15 is negative |

17 |

18 |

Check here if paid electronically 6 |

|

Please

Sign

Here

6I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge

and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Title |

Date |

Officerʼs |

|

Signature |

|

Paid

Preparer’s

Use Only

Preparerʼs signature

Firmʼs name (or yours, if

Phone No. |

Preparerʼs SSN/PTIN |

Date

E.I. No.

ZIP Code

If you are not making a payment, mail your return to: |

If you are making a payment, mail your return, Form |

Alabama Department of Revenue |

Alabama Department of Revenue |

Business Privilege Tax Section |

Business Privilege Tax Section |

P.O. Box 327431 |

P.O. Box 327320 |

Montgomery, AL |

Montgomery, AL |

Telephone Number: (334) |

Web site: www.revenue.alabama.gov |

ADOR

FORM |

BUSINESS PRIVILEGE |

*220002CP* |

Alabama Department of Revenue |

CPT |

TAXABLE/FORM YEAR |

Alabama Business Privilege Tax |

|

PAGE 2 |

2022 |

|

Privilege Tax Computation Schedule |

1a. FEIN |

1b. LEGAL NAME OF BUSINESS ENTITY |

1c. DETERMINATION PERIOD END DATE (BALANCE SHEET DATE) |

|

V |

|

|

(MM/DD/YYYY) |

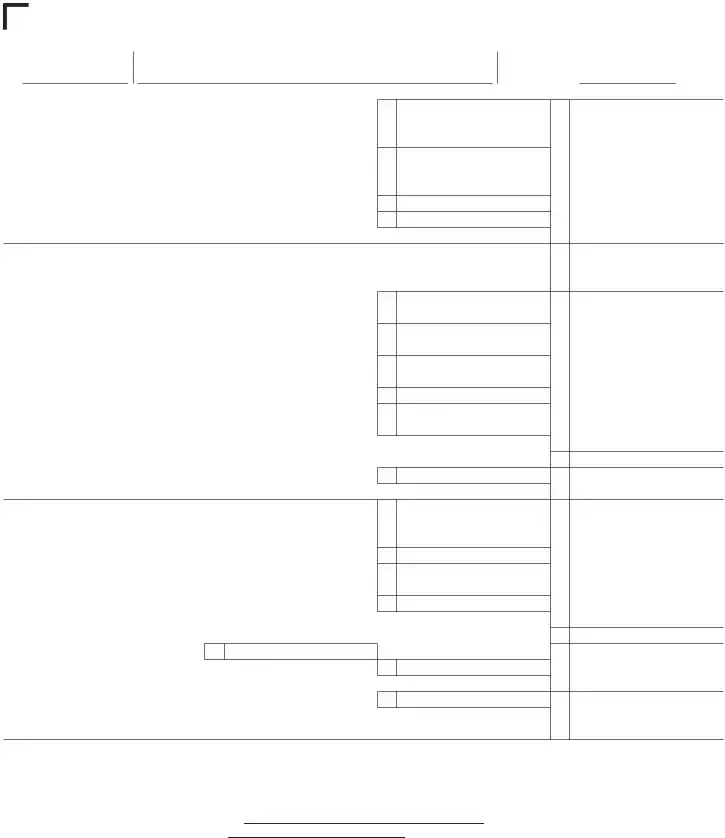

PART A – NET WORTH COMPUTATION

Corporations & Entities Taxed as Corporations

1Issued capital stock and additional paid in capital (without reduction for treasury stock)

|

but not less than zero |

1 |

2 |

Retained earnings, but not less than zero, including dividends payable. For LLC’s taxed |

|

|

as corporations and |

|

|

minus liabilities |

2 |

3 |

Gross amount of related party debt exceeding the sums of line 1 and 2 |

3 |

4 |

All payments for compensation or similar amounts in excess of $500,000 |

4 |

5 |

Total net worth (add lines |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 |

PART B – PRIVILEGE TAX EXCLUSIONS AND DEDUCTIONS |

|

|

Exclusions (Attach supporting documentation) (SEE INSTRUCTIONS) |

|

|

1 |

Total net worth from line 5 above |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 |

2 |

Book value of the investments by the taxpayer in the equity of other taxpayers |

2 |

3Financial institutions, only – Book value of the investments in other corporations or LLE’s

|

if the taxpayer owns more than 50 percent of the corporation or LLE |

3 |

4 |

Unamortized portion of goodwill and core deposit intangibles resulting from a direct |

|

|

purchase |

4 |

5 |

Unamortized balance of properly elected |

5 |

6Financial institutions, only – The amount adjusted net worth

|

exceeds six percent of total assets (see instructions) |

6 |

|

|

7 |

Total exclusions (sum of lines |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 7 |

8 |

Net worth subject to apportionment (line 1 less line 7) |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 8 |

9 |

Apportionment factor (see instructions) |

9 |

. |

% |

10 |

Total Alabama net worth (multiply line 8 by line 9) |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 10 |

Deductions (Attach supporting documentation) (SEE INSTRUCTIONS)

11Net investment in bonds and securities issued by the State of Alabama or

political subdivision thereof, when issued prior to January 1, 2000. . . . . . . . . . . . . . . . . . . 11

12 Net investment in all air, ground, or water pollution control devices in Alabama. . . . . . . . . . 12

13Reserves for reclamation, storage, disposal, decontamination, or retirement associated

|

with a plant, facility, mine or site in Alabama . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

13 |

|

14 |

Book value of amount invested in qualifying low income housing projects (see instructions) |

14 |

|

|

15 |

Total deductions (add lines |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . 15 |

16 |

Taxable Alabama net worth (line 10 less line 15) |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . 16 |

|

17a |

Federal Taxable Income Apportioned to AL . . |

17a |

|

|

17b |

Tax rate (see instructions) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

17b |

. |

18 |

Gross privilege tax calculated (multiply line 16 by line 17b) |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . 18 |

|

19 |

Alabama enterprise zone credit (see instructions) |

19 |

|

|

20Privilege Tax Due (line 18 less line 19) (minimum $100, for maximum see instructions)

Enter also on Form CPT, page 1, line 9, Privilege Tax Due . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Full payment of any amount due for a taxable year is due by the original

due date of the return (without consideration of any filing extensions in place).

an Alabama Schedule

ADOR

Alabama Ju 26D - The form represents a formal channel for minors to assert their legal rights.

Understanding the importance of a Colorado Do Not Resuscitate Order form is essential for individuals wishing to communicate their healthcare preferences. This legal document ensures that in the event of a medical crisis, such as the cessation of breathing or heartbeat, medical personnel will honor the patient's wishes. For those looking to obtain this form, resources like Colorado PDF Forms can provide the necessary documentation.

Irp Alabama - Forms can be completed manually or digitally for convenience.

The Alabama Business Privilege Tax Return (CPT) shares similarities with the California Corporate Franchise Tax Board Form 100. Both forms require corporations to report their income and calculate taxes owed based on net income or net worth. The California form also includes sections for taxpayer information, determination periods, and tax computations, reflecting a similar structure aimed at assessing corporate tax obligations. Each form mandates the filing of an annual report and includes specific instructions regarding penalties for late submissions.

For boat owners in California, ensuring the proper transfer of ownership is crucial, which is why utilizing forms like the Marine Bill of Sale can facilitate a smooth transaction process. This document protects both parties involved by clearly recording essential details of the sale, thus serving as a vital part of the buying and selling experience.

Another document akin to the Alabama CPT is the New York State Corporation Franchise Tax Return (CT-3). This form serves C-Corporations in New York and requires details about the corporation’s income, deductions, and credits. Like the Alabama form, it necessitates taxpayer identification information and has a clear layout for tax calculations. Both documents also include provisions for amended returns, emphasizing the importance of accuracy in corporate tax reporting.

The Texas Franchise Tax Report is another document comparable to the Alabama CPT. Texas corporations must file this report annually, detailing their revenue and calculating the franchise tax based on their margin. Similar to the Alabama form, it requires basic information about the corporation and provides a framework for calculating tax liabilities. Both forms also allow for deductions and credits, reflecting the states' efforts to ensure fair taxation of corporations.

Additionally, the Florida Corporate Income Tax Return (F-1120) is similar to the Alabama CPT form. Corporations in Florida must complete this form to report their income and calculate the corporate income tax. Both documents include sections for taxpayer information, income reporting, and tax computation. Furthermore, they both require corporations to maintain compliance with state regulations and file returns by specific deadlines to avoid penalties.

The Illinois Corporation Income and Replacement Tax Return (IL-1120) is another relevant document. This form is used by corporations to report their income and calculate taxes owed to the state of Illinois. Similar to the Alabama CPT, it requires detailed information about the corporation, including its financial status and tax calculations. Both forms aim to ensure that corporations meet their tax obligations while allowing for certain deductions and credits based on specific criteria.

The Pennsylvania Corporate Net Income Tax Return (RCT-101) also bears resemblance to the Alabama CPT form. Corporations in Pennsylvania utilize this form to report their income and calculate the corporate net income tax. Both documents require comprehensive financial data and include sections for various deductions and credits. They also emphasize the importance of timely filing to avoid penalties, maintaining a consistent approach to corporate taxation across states.

Another document that aligns with the Alabama CPT is the Ohio Corporate Franchise Tax Report (FT-1120). Corporations in Ohio use this form to report their taxable income and calculate the franchise tax owed. Similarities include the structure of the form, which captures taxpayer information, income details, and tax computations. Both forms also allow for the inclusion of various deductions, reflecting the states' approaches to corporate taxation.

Lastly, the Massachusetts Corporate Excise Tax Return (Form 355) is comparable to the Alabama CPT form. Corporations in Massachusetts must file this return to report their income and calculate the excise tax owed. Both forms require detailed taxpayer information and provide a framework for income reporting and tax calculations. They also share common deadlines for submission and penalties for late filings, emphasizing the importance of compliance in corporate tax responsibilities.

Filling out the Alabama CPT form can be a straightforward process, but many people make mistakes that can lead to complications. One common error is failing to check the correct type of taxpayer. The form specifically asks for C Corporations, but some individuals mistakenly check boxes for other types of entities, such as insurance companies or limited liability entities. This can lead to delays or even rejection of the form.

Another frequent mistake involves the determination period dates. Taxpayers often forget to fill in both the beginning and ending dates. Leaving these fields blank creates confusion and may result in the form being returned for correction. It's essential to ensure that these dates accurately reflect the corporation's fiscal year or calendar year.

Many also overlook the importance of providing complete taxpayer information. Missing details, such as the legal name, Federal Employer Identification Number (FEIN), or mailing address, can cause significant issues. The Alabama Department of Revenue needs this information to process the return accurately. Incomplete forms can lead to delays in processing and potential penalties.

Additionally, some people neglect to check the appropriate boxes regarding whether the return is amended or initial. This oversight can complicate the review process. If a taxpayer submits an amended return without indicating so, it may not be processed correctly. Always double-check these boxes to ensure clarity.

Lastly, many individuals forget to sign the form. A signature is not just a formality; it is a declaration that the information provided is true and accurate. Without a signature, the form may be considered incomplete, leading to further complications. Always remember to sign and date the form before submission to avoid unnecessary delays.