Fill Out a Valid Alabama Ppt Form

Fill Out a Valid Alabama Ppt Form

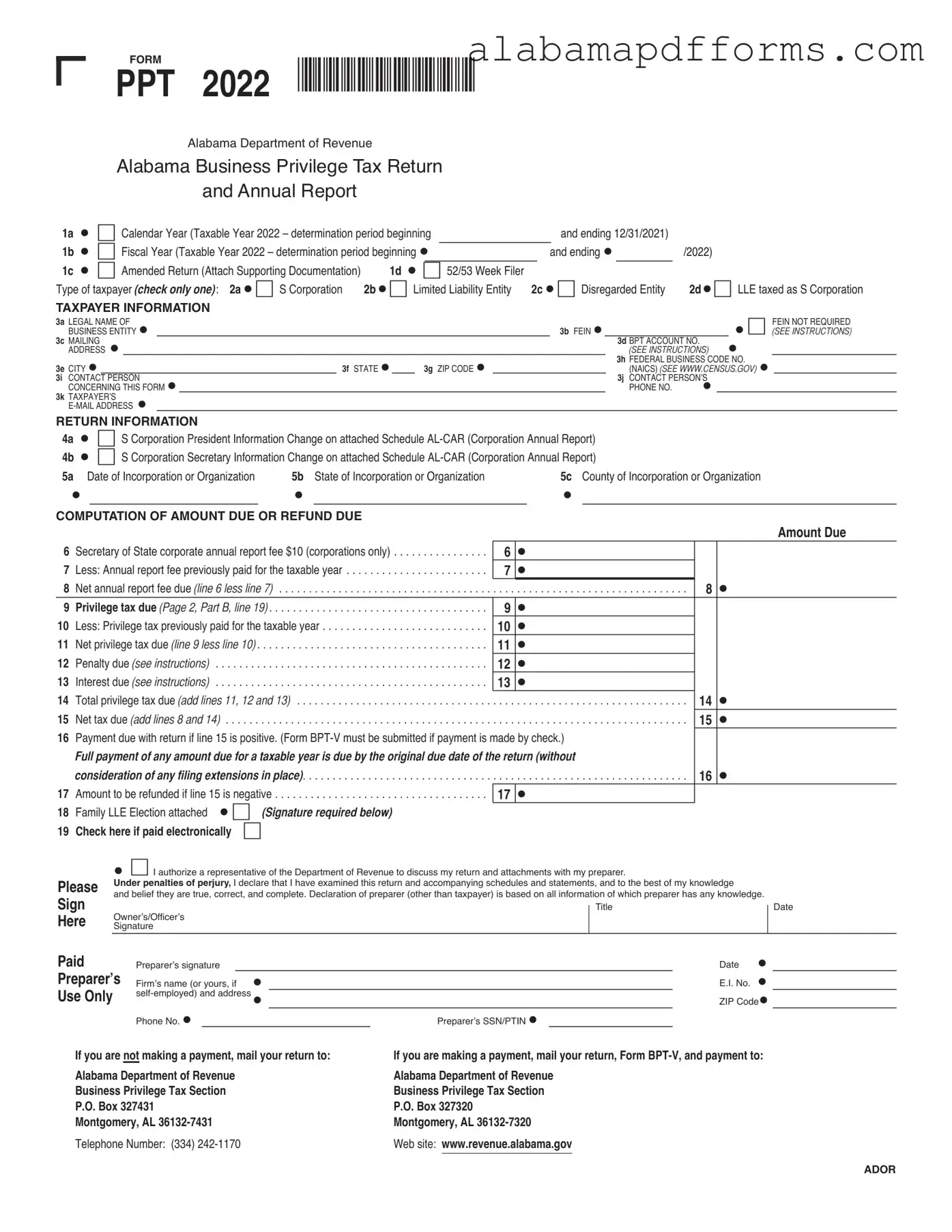

The Alabama Business Privilege Tax Return, commonly referred to as the Alabama PPT form, is a crucial document for businesses operating in the state. This form is used to report the annual business privilege tax owed to the Alabama Department of Revenue. It encompasses various essential sections, including taxpayer information, tax computation, and payment details. Businesses must indicate their type, such as S Corporations or Limited Liability Entities, and provide specific information like their legal name, federal employer identification number (FEIN), and contact details. The form also requires a computation of the amount due or any potential refund, taking into account the corporate annual report fee and any prior payments made. Additionally, it outlines the necessary calculations for determining net worth and the applicable privilege tax based on that figure. For businesses with specific circumstances, such as amended returns or fiscal year filers, the form includes options to accommodate these needs. Completing the Alabama PPT form accurately is vital, as it ensures compliance with state tax laws and helps avoid penalties or interest charges for late payments.

Understanding the Alabama Ppt form can be challenging due to several misconceptions. Here are eight common misunderstandings, along with clarifications to help navigate the process.

By clarifying these misconceptions, businesses can better prepare for their tax obligations and ensure compliance with Alabama's requirements.

FORM

PPT 2022 *220001PP*

Alabama Department of Revenue

Alabama Business Privilege Tax Return

and Annual Report

1a |

6 Calendar Year (Taxable Year 2022 – determination period beginning |

and ending 12/31/2021) |

|

||

1b |

6 Fiscal Year (Taxable Year 2022 – determination period beginning |

|

and ending |

/2022) |

|

1c |

6 Amended Return (Attach Supporting Documentation) |

1d |

6 52/53 Week Filer |

|

|

Type of taxpayer (check only one): 2a |

6 S Corporation |

2b |

6 Limited Liability Entity |

2c 6 Disregarded Entity |

2d |

6 LLE taxed as S Corporation |

|||

TAXPAYER INFORMATION |

|

|

|

|

|

|

|

|

|

3a LEGAL NAME OF |

|

|

|

|

|

|

6 |

FEIN NOT REQUIRED |

|

BUSINESS ENTITY |

|

|

|

|

3b FEIN |

|

(SEE INSTRUCTIONS) |

||

3c MAILING |

|

|

|

|

3d BPT ACCOUNT NO. |

|

|

||

ADDRESS |

|

|

|

|

(SEE INSTRUCTIONS) |

|

|

||

|

|

|

|

|

|

3h FEDERAL BUSINESS CODE NO. |

|

||

3e CITY |

3f |

STATE |

3g ZIP CODE |

|

(NAICS) (SEE WWW.CENSUS.GOV) |

|

|||

3i CONTACT PERSON |

|

|

|

|

3j CONTACT PERSON’S |

|

|

||

CONCERNING THIS FORM |

|

|

|

|

PHONE NO. |

|

|

|

|

3k TAXPAYER’S |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

RETURN INFORMATION |

|

|

|

|

|

|

|

|

|

4a |

6 S Corporation President Information Change on attached Schedule |

|

|

|

|||||

4b |

6 S Corporation Secretary Information Change on attached Schedule |

|

|

|

|||||

5a |

Date of Incorporation or Organization |

5b State of Incorporation or Organization |

|

5c County of Incorporation or Organization |

|

||||

COMPUTATION OF AMOUNT DUE OR REFUND DUE |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

Amount Due |

6 Secretary of State corporate annual report fee $10 (corporations only) |

6 |

|

|

|

|

||||

7 Less: Annual report fee previously paid for the taxable year . |

. . . . . . |

. . . . . . . . . . . . . . . . . |

7 |

|

|

|

|

||

8 Net annual report fee due (line 6 less line 7) |

. . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

8 |

|

|

||

9 |

Privilege tax due (Page 2, Part B, line 19) |

. . . . . . |

. . . . . . . . . . . . . . . . . |

9 |

|

|

|

|

|

10 |

Less: Privilege tax previously paid for the taxable year |

. . . . . . |

. . . . . . . . . . . . . . . . . |

10 |

|

|

|

|

|

11 |

Net privilege tax due (line 9 less line 10) |

. . . . . . |

. . . . . . . . . . . . . . . . . |

11 |

|

|

|

|

|

12 |

Penalty due (see instructions) |

. . . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . |

12 |

|

|

|

|

13 |

Interest due (see instructions) |

. . . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . |

13 |

|

|

|

|

14 |

Total privilege tax due (add lines 11, 12 and 13) |

. . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

14 |

|

|

|

15 |

Net tax due (add lines 8 and 14) |

. . . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

15 |

|

|

16Payment due with return if line 15 is positive. (Form

Full payment of any amount due for a taxable year is due by the original due date of the return (without

|

consideration of any filing extensions in place) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 |

|

17 |

Amount to be refunded if line 15 is negative |

17 |

|

18 |

Family LLE Election attached |

6 (Signature required below) |

|

19 |

Check here if paid electronically |

6 |

|

Please

Sign

Here

6I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge

and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Title |

Date |

Ownerʼs/Officerʼs |

|

Signature |

|

Paid |

Preparerʼs signature |

|

|

Date |

Preparer’s |

Firmʼs name (or yours, if |

|

|

E.I. No. |

Use Only |

|

|

ZIP Code |

|

|

|

|

||

|

|

|

|

|

|

Phone No. |

Preparerʼs SSN/PTIN |

||

If you are not making a payment, mail your return to: |

If you are making a payment, mail your return, Form |

|||

Alabama Department of Revenue |

Alabama Department of Revenue |

|||

Business Privilege Tax Section |

Business Privilege Tax Section |

|||

P.O. Box 327431 |

P.O. Box 327320 |

|||

Montgomery, AL |

Montgomery, AL |

|||

Telephone Number: (334) |

Web site: www.revenue.alabama.gov |

|||

|

|

|

|

|

ADOR

|

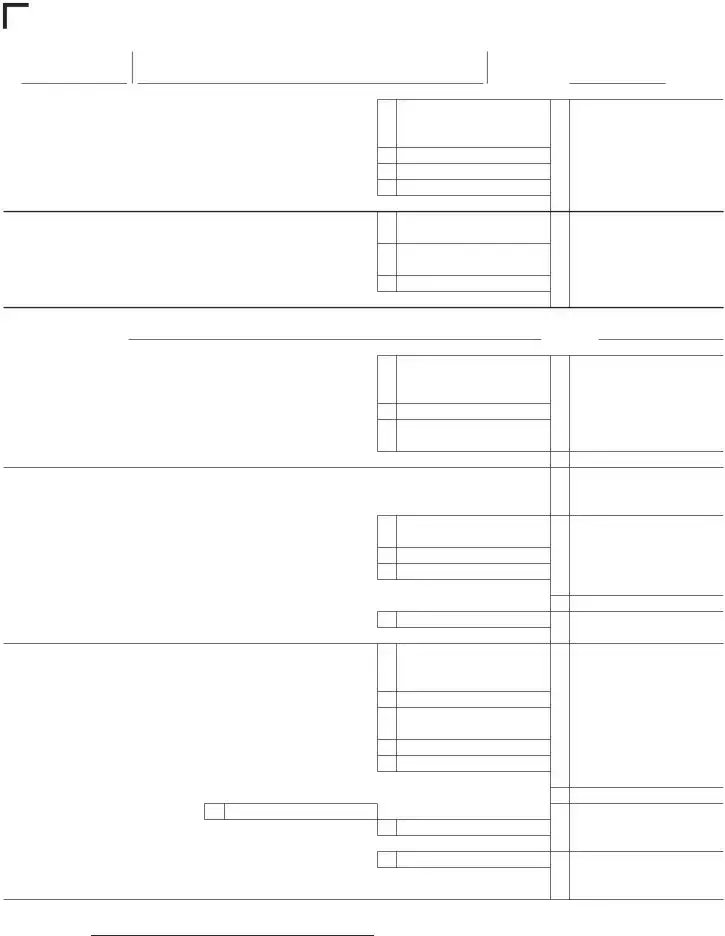

FORM |

BUSINESS PRIVILEGE |

*220002PP* |

Alabama Department of Revenue |

|

PPT |

TAXABLE/FORM YEAR |

Alabama Business Privilege Tax |

|

|

PAGE 2 |

2022 |

|

Privilege Tax Computation Schedule |

1a. |

FEIN |

1b. LEGAL NAME OF BUSINESS ENTITY |

1c. DETERMINATION PERIOD END DATE (BALANCE SHEET DATE) |

|

V |

|

|

(MM/DD/YYYY) |

|

PART A – NET WORTH COMPUTATION |

|

|

||

I. |

|

|

|

|

1 |

Issued capital stock and additional paid in capital (without reduction for treasury stock) |

|

||

|

but not less than zero |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

1 |

|

2 |

Retained earnings, but not less than zero, including dividends payable |

2 |

||

3 |

Gross amount of related party debt exceeding the sums of line 1 and 2 |

3 |

||

4 |

All payments for compensation, distributions, or similar amounts in excess of $500,000. . . . |

4 |

||

5 |

Total net worth (add lines |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 |

||

II. Limited Liability Entities (LLE's) |

|

|

||

6 |

Sum of the partners’/members’ capital accounts, but not less than zero |

6 |

||

7All compensation, distributions, or similar amounts paid to a partner/member in

|

excess of $500,000 |

7 |

8 |

Gross amount of related party debt exceeding the amount on line 6 |

8 |

9 |

Total net worth (add lines 6, 7 and 8). Go to Part B, line 1 |

9 |

III. Disregarded Entities |

|

|

10 |

Single Member Name: |

FEIN/SSN: |

11If a disregarded entity has as its single member a taxpayer that is subject to the privilege tax, then the disregarded entity pays the minimum tax. (Go to Part B, line 19.)

12Assets minus liabilities for all disregarded entities that have as a single member an entity that is not subject to the privilege tax, but not less than zero (supporting

documentation required). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

13 Gross amount of related party debt exceeding the amount on line 12 . . . . . . . . . . . . . . . . . 13

14For disregarded entities, all compensation, distributions,

|

or similar amounts paid to a member in excess of $500,000 |

14 |

|

|

15 Total net worth (sum of lines 12, 13 and 14). Go to Part B, line 1 |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 15 |

|

PART B – PRIVILEGE TAX EXCLUSIONS AND DEDUCTIONS |

|

|

|

|

Exclusions (Attach supporting documentation) (SEE INSTRUCTIONS) |

|

|

|

|

1 |

Total net worth from Part A – line 5, 9, or 15 |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 1 |

2 |

Book value of the investments by the taxpayer in the equity of other taxpayers |

2 |

|

|

3 |

Unamortized portion of goodwill resulting from a direct purchase |

3 |

|

|

4 |

Unamortized balance of properly elected |

4 |

|

|

5 |

Total exclusions (sum of lines |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 5 |

6 |

Net worth subject to apportionment (line 1 less line 5) |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 6 |

7 |

Apportionment factor (see instructions) |

7 |

. |

% |

8 |

Total Alabama net worth (multiply line 6 by line 7) |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . |

. . 8 |

Deductions (Attach supporting documentation) (SEE INSTRUCTIONS)

9Net investment in bonds and securities issued by the State of Alabama or

political subdivision thereof, when issued prior to January 1, 2000. . . . . . . . . . . . . . . . . . . .

10 Net investment in all air, ground, or water pollution control devices in Alabama. . . . . . . . . .

11Reserves for reclamation, storage, disposal, decontamination, or retirement

|

associated with a plant, facility, mine or site in Alabama |

11 |

|

|

12 |

Book value of amount invested in qualifying low income housing projects (see instructions) |

12 |

|

|

13 |

30 percent of federal taxable income apportioned to Alabama, but not less than zero |

13 |

|

|

14 |

Total deductions (add lines |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . 14 |

15 |

Taxable Alabama net worth (line 8 less line 14) |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . 15 |

|

16a |

Federal Taxable Income Apportioned to AL . . |

16a |

|

|

16b |

Tax rate (see instructions) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

16b |

. |

17 |

Gross privilege tax calculated (multiply line 15 by line 16b) |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . 17 |

|

18 |

Alabama enterprise zone credit (see instructions) |

18 |

|

|

19Privilege Tax Due (line 17 less line 18) (minimum $100, for maximum see instructions)

Enter also on Form PPT, page 1, line 9, Privilege Tax Due (must be paid by the original due date of the return) . . . . . . . . . . . . . . . . 19

|

|

Other (noncorporate) |

|

are not required to file an Alabama Schedule |

ADOR |

|

Alabama Form 40es 2023 - The Alabama Department of Revenue does not send payment notices for estimated tax.

Alabama Income Tax Forms - This form must be prepared for each reporting period the business operates in Alabama.

For anyone navigating job applications or verifying employee credentials, understanding the importance of a reliable application is crucial. This guide provides insights into completing an effective Employment Verification form, ensuring you have the right documentation for any employment-related verification needs.

How Much Is Child Support in Alabama for One Child - The affidavit must be filed in the appropriate circuit or district court in Alabama.

The Alabama Business Privilege Tax Return and Annual Report (Form PPT) shares similarities with the IRS Form 1065, which is used by partnerships to report income, deductions, gains, and losses. Both forms require detailed information about the entity's financial performance and tax obligations. While Form 1065 focuses on partnerships, the Alabama PPT form is tailored for business entities operating in Alabama, ensuring compliance with state-specific tax regulations. Both forms also necessitate the disclosure of ownership structures and financial data, making them essential for proper tax reporting.

Another document akin to the Alabama PPT form is the IRS Form 1120S, which is designated for S Corporations. Like the PPT, Form 1120S requires S Corporations to report their income, deductions, and credits. Both forms emphasize the importance of accurate financial reporting, and they require details about shareholders and distributions. While the IRS form is federal, the Alabama PPT form addresses state-level tax obligations, highlighting the need for compliance at both levels.

The Alabama PPT form is also similar to the Georgia Form 600, which is the state income tax return for corporations. Both documents require corporations to report their income and calculate taxes owed to the state. They include sections for detailing financial performance and for reporting any tax credits or deductions applicable. The Georgia Form 600, like the Alabama PPT, ensures that businesses fulfill their state tax responsibilities while providing a clear structure for reporting financial information.

Another comparable document is the California Form 100, the state's corporate franchise tax return. Both the Alabama PPT and California Form 100 require corporations to disclose their financial information and calculate taxes based on net income. They also include provisions for penalties and interest if payments are late. The main distinction lies in the state-specific requirements and rates, but the underlying purpose of both forms is to ensure compliance with state tax laws.

The Alabama PPT form has parallels with the New York State Form CT-3, which is the general business corporation franchise tax return. Both forms require corporations to report their income and calculate their tax liability. They also necessitate information about the corporate structure and any tax credits that may apply. While the New York form is specific to New York State, the Alabama PPT serves a similar function for businesses operating within Alabama.

Similar to the Alabama PPT form is the Texas Franchise Tax Report. Both documents require businesses to report their revenue and calculate taxes owed based on their financial performance. They include sections for detailing deductions and credits. Although the Texas report is focused on franchise tax, like the Alabama PPT, it emphasizes the importance of accurate reporting to avoid penalties and ensure compliance with state tax laws.

The Florida Corporate Income Tax Return (Form F-1120) is another document that resembles the Alabama PPT form. Both forms require corporations to report their income and calculate taxes owed to the state. They also include provisions for penalties and interest on late payments. While the Florida form is specific to corporate income tax, the Alabama PPT focuses on business privilege tax, yet both serve to ensure businesses meet their tax obligations at the state level.

The importance of legal documents cannot be underestimated in maintaining compliance and protecting interests in business operations, and this extends to various forms utilized within different jurisdictions. One such important document is the Hold Harmless Agreement, which plays a critical role in mitigating legal risks associated with various activities. This agreement underscores the importance of understanding liability and risk management in any business endeavor, especially when navigating complex regulatory frameworks.

The Ohio Commercial Activity Tax (CAT) Annual Return is also comparable to the Alabama PPT form. Both require businesses to report their financial activity and calculate taxes based on gross receipts. They emphasize the need for accurate reporting to avoid penalties. While the Alabama PPT is focused on privilege tax, the Ohio CAT is based on commercial activity, yet both documents aim to ensure compliance with state tax regulations.

Lastly, the Pennsylvania Corporate Tax Report (RCT-101) shares similarities with the Alabama PPT form. Both forms require corporations to disclose their financial information and calculate taxes owed. They include provisions for reporting income, deductions, and credits. While the Pennsylvania form is specific to corporate taxes, the Alabama PPT serves a similar purpose for businesses operating in Alabama, reinforcing the need for compliance with state tax laws.

Filling out the Alabama Business Privilege Tax Return and Annual Report (Form PPT) can be a complex task, and many individuals make common mistakes that can lead to complications. Understanding these pitfalls can help ensure a smoother filing process.

One frequent error occurs when taxpayers fail to select the correct type of taxpayer. The form provides options such as S Corporation, Limited Liability Entity, and Disregarded Entity. Not checking the appropriate box can result in misclassification, which may affect tax calculations and compliance. Always take a moment to review the options and select the one that accurately reflects your business structure.

Another common mistake is neglecting to provide the correct Federal Employer Identification Number (FEIN). The FEIN is crucial for identification purposes. If this number is missing or incorrect, it can lead to delays in processing the return and potential penalties. Ensure that you double-check this information against official documents.

Inaccurate calculations of the net worth can also lead to significant issues. The form requires specific computations, and miscalculating figures can affect the overall tax liability. This includes failing to account for all relevant assets and liabilities. It is advisable to carefully review the calculations and consider using accounting software or consulting with a professional if necessary.

Additionally, taxpayers often overlook the requirement for supporting documentation. Certain deductions and exclusions necessitate attachments to substantiate claims. Failing to include these documents can result in disallowance of deductions, leading to a higher tax liability than anticipated. Always attach the necessary documentation as outlined in the instructions.

Another mistake is related to the payment of taxes. Taxpayers sometimes misunderstand the payment requirements, especially regarding the submission of Form BPT-V when making payments by check. Not following the correct procedure can lead to processing delays or penalties. Make sure to read the instructions carefully regarding payment methods and deadlines.

Lastly, many individuals forget to sign the return. A signature is not just a formality; it is a declaration of the accuracy of the information provided. A missing signature can result in the return being considered incomplete, which can lead to further complications. Always remember to sign and date the return before submission.

By being aware of these common mistakes, individuals can navigate the Alabama PPT form more effectively, reducing the risk of errors and ensuring compliance with state tax regulations.