Fill Out a Valid Bit V Alabama Form

Fill Out a Valid Bit V Alabama Form

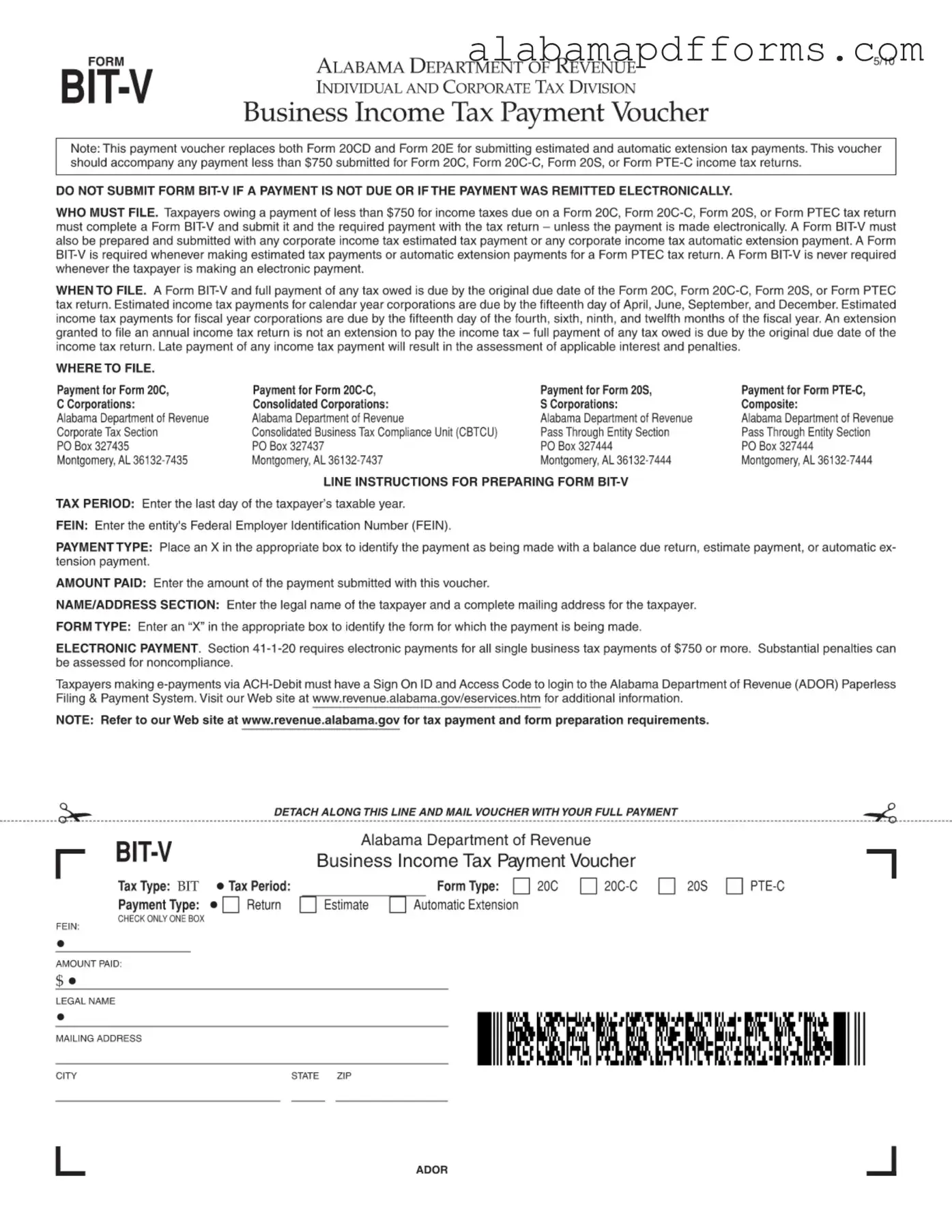

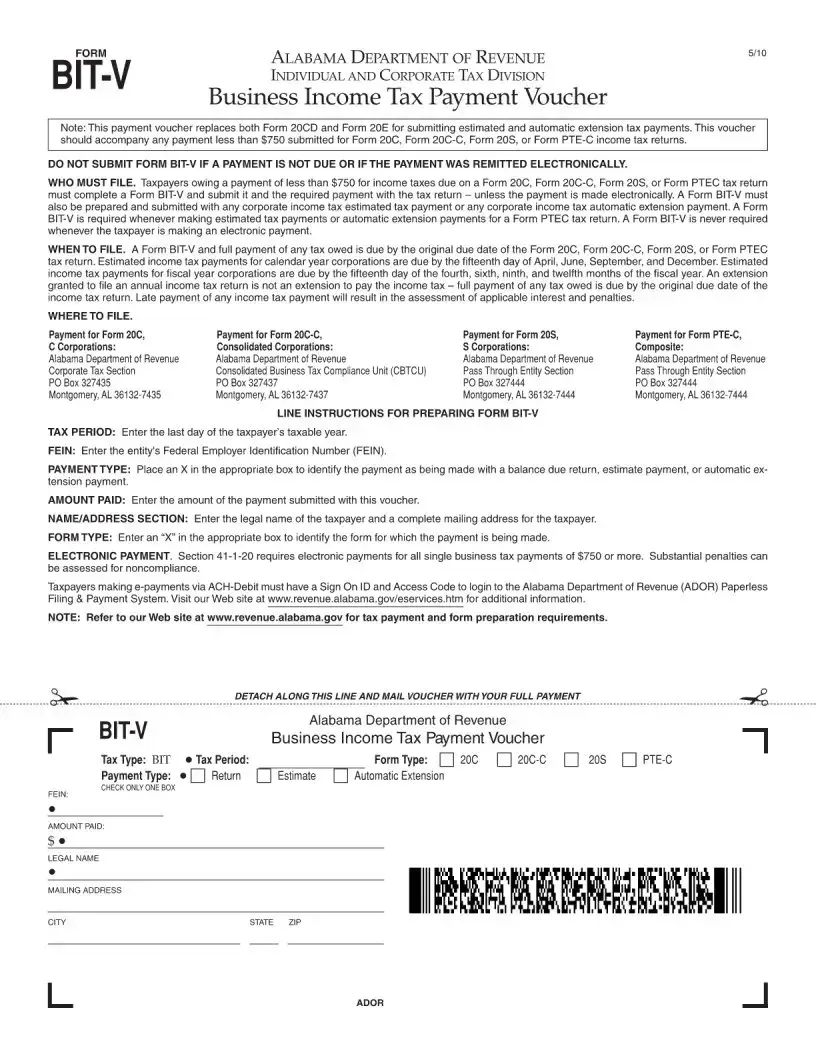

The Bit V Alabama form is an essential document for taxpayers in Alabama who owe income taxes on specific tax returns. This payment voucher serves as a streamlined method for submitting estimated and automatic extension tax payments, effectively replacing the older Form 20CD and Form 20E. Designed for payments of less than $750, the Bit V form must accompany returns for C Corporations (Form 20C), Consolidated Corporations (Form 20C-C), S Corporations (Form 20S), or Composite returns (Form PTE-C). Taxpayers should only use this form when a payment is due; electronic payments do not require its submission. Timeliness is crucial, as the form and payment must be filed by the original due date of the respective tax return. Additionally, the form provides specific instructions on completing various sections, including tax period, payment type, and amount due. It also outlines where to send payments based on the type of corporation. Understanding the requirements and deadlines associated with the Bit V form is vital for compliance and avoiding penalties.

Understanding the Bit V Alabama form can be challenging, and several misconceptions may lead to confusion. Here are four common misunderstandings about this important tax document:

This is not accurate. While the form is often associated with corporate income tax payments, it is also applicable to individual taxpayers who owe less than $750 for their income taxes on specific tax returns. Therefore, both individuals and corporations may need to use this form.

Many believe that any payment made towards income taxes requires a Bit V submission. In reality, the form should only accompany payments that are less than $750 and are not made electronically. If a payment is made electronically, the Bit V form is not necessary.

This is a common misunderstanding. An extension granted for filing a tax return does not extend the deadline for paying any taxes owed. Taxpayers must ensure that full payment is made by the original due date to avoid penalties and interest.

Some individuals think they can submit the Bit V form at their convenience. However, it is crucial to remember that the form and any payment must be submitted by the original due date of the related tax return. Late submissions can lead to additional fees and complications.

Alabama 3 - Contact details for independent references are to be provided at the end of the form.

Medicare Savings Program - Be mindful of deadlines in submitting your application to the District Office.

Utilizing the Oklahoma Transfer-on-Death Deed provides peace of mind for property owners, ensuring that your real estate will seamlessly pass to your beneficiaries without the hassle of probate. For more information and to access the necessary forms, visit https://todform.com/blank-oklahoma-transfer-on-death-deed.

Title Loan Repossession Laws Alabama - It is crucial to keep a record of the date of repossession as it needs to be indicated on the form.

The Form 1040-V is similar to the Bit V Alabama form in that it serves as a payment voucher for individual taxpayers submitting their federal income tax returns. Like the Bit V, it is used when taxpayers owe a balance and need to submit a payment along with their return. The 1040-V must be included with the payment, ensuring that the IRS can accurately apply the payment to the taxpayer’s account. Both forms emphasize the importance of submitting the payment by the original due date to avoid penalties and interest.

The Form 4868, the application for an automatic extension of time to file an individual income tax return, shares similarities with the Bit V form. While the Bit V is used for making payments, the 4868 allows taxpayers to extend their filing deadline without extending the payment deadline. Both forms require careful attention to deadlines, as failing to pay taxes owed by the original due date can lead to penalties. The 4868 also highlights the necessity of filing the form even if no payment is due, while the Bit V is only necessary when a payment is owed.

The Form 941-V, which is a payment voucher for employers submitting their quarterly payroll tax returns, resembles the Bit V in its function of facilitating payment processing. Both forms require the taxpayer to indicate the type of payment being made, whether it is a balance due or an estimated payment. The 941-V ensures that payments are correctly attributed to the appropriate quarter, just as the Bit V ensures payments are linked to the specific tax returns being filed. Timeliness is crucial for both forms to avoid penalties.

The Form 1120-W is used by corporations to make estimated tax payments and is similar to the Bit V in that it addresses estimated payments for taxes owed. Both forms require taxpayers to calculate their payments based on expected tax liabilities. The 1120-W is specifically designed for corporations, while the Bit V caters to various business entities. Both emphasize the importance of making timely payments to avoid interest and penalties, reinforcing the need for accurate tax planning.

The Form 990-T, used by tax-exempt organizations to report unrelated business income, has similarities with the Bit V form in terms of payment requirements. Organizations must file this form when they owe taxes on unrelated business income, and it includes a payment voucher section. Like the Bit V, the 990-T requires attention to detail in reporting and payment to avoid penalties for late submissions. Both forms reflect the obligation to meet tax responsibilities even when the entity is generally exempt from income tax.

Understanding the various forms used for estimated tax payments is crucial for compliance, much like the importance of a Hold Harmless Agreement in managing liabilities during activities that carry risk. Each form, whether it's the Bit V, IRS Form 1040-ES, or state-specific versions, serves to streamline payment processes and reinforce the need for accurate records. By grasping the purpose and requirements of these forms, taxpayers can ensure timely submissions, avoiding unnecessary penalties and fostering clarity in their financial responsibilities.

Lastly, the Form 720 is a quarterly federal excise tax return that includes a payment voucher. It is similar to the Bit V in that it provides a mechanism for taxpayers to submit payments related to specific tax liabilities. Both forms require taxpayers to provide identifying information and the amount of payment due. Timeliness is crucial in both cases, as late payments can result in significant penalties. The Form 720 emphasizes the importance of compliance with federal excise taxes, paralleling the Bit V’s focus on state business income taxes.

Completing the Bit V Alabama form can be straightforward, yet many individuals make common mistakes that can lead to complications. One prevalent error is failing to submit the form when a payment is due. Taxpayers must ensure they complete and send the Bit V form if they owe less than $750. Ignoring this requirement can result in penalties and interest.

Another frequent mistake involves incorrect payment type selection. Taxpayers must clearly indicate whether the payment is for a balance due return, an estimated payment, or an automatic extension payment. An incorrect selection can delay processing and may lead to additional inquiries from the Alabama Department of Revenue.

Providing an incomplete or incorrect mailing address is also a common oversight. Taxpayers should ensure that the legal name and complete mailing address are accurately filled out. Missing or incorrect information can cause delays in communication or even misdirect the payment.

Many individuals neglect to enter the correct Federal Employer Identification Number (FEIN). This number is crucial for identifying the taxpayer's entity. Omitting it or providing an incorrect FEIN can complicate the processing of the form and payment.

Additionally, taxpayers sometimes fail to specify the correct tax period. Entering the last day of the taxable year is essential for proper record-keeping and compliance. Without this information, the Department of Revenue may struggle to associate the payment with the correct tax year.

Another mistake occurs when taxpayers do not follow the specific instructions for where to file the form. Each type of corporation has a designated mailing address. Sending the form to the wrong address can result in significant delays in processing the payment.

Lastly, some taxpayers mistakenly believe that submitting the Bit V form is unnecessary if they have made an electronic payment. However, the form is required for certain situations, such as estimated tax payments or automatic extensions. Understanding the nuances of when to use the Bit V form is essential for compliance and avoiding penalties.