Fill Out a Valid Irp Alabama Form

Fill Out a Valid Irp Alabama Form

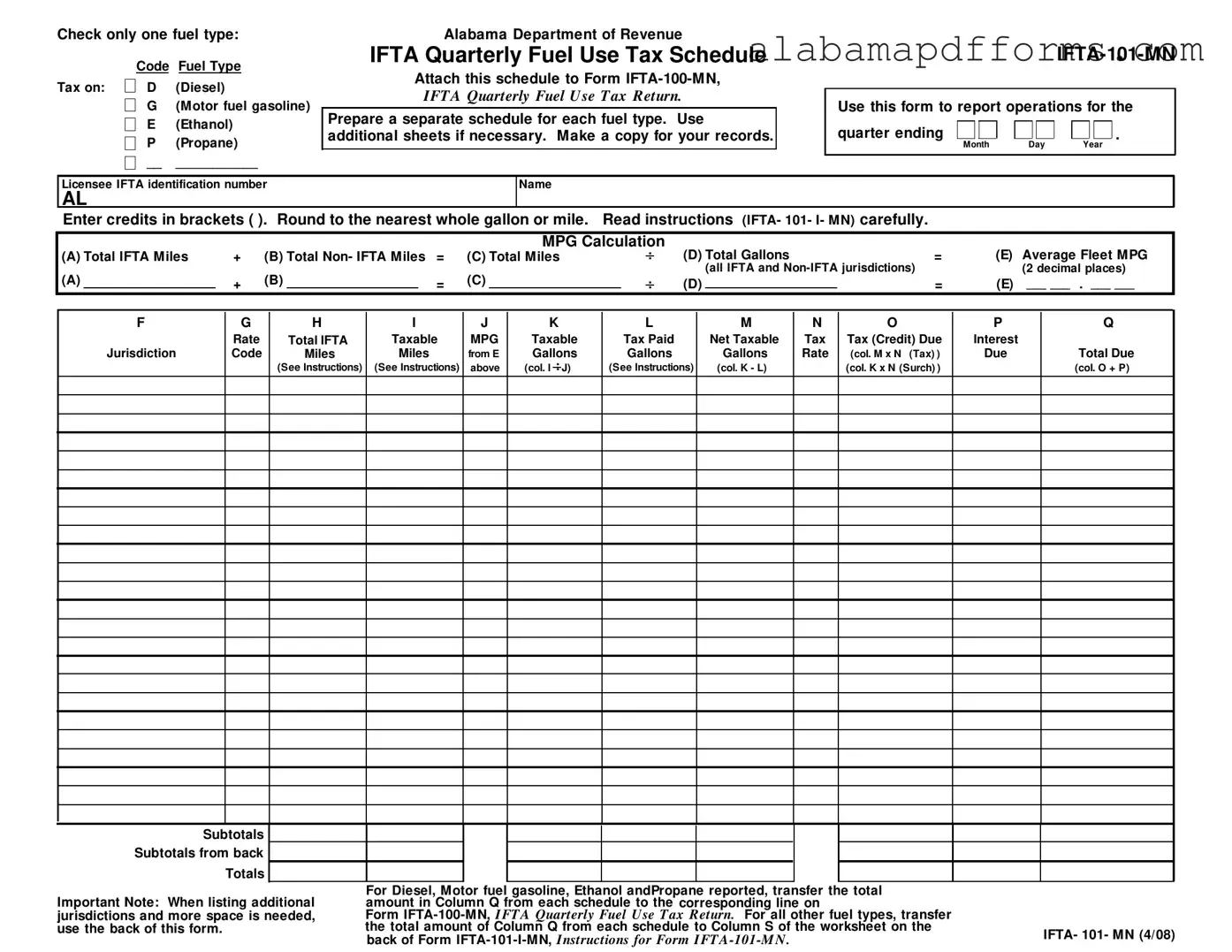

The IFTA Alabama form is an essential tool for businesses and individuals involved in the transportation industry, specifically for those who operate commercial vehicles across state lines. This form helps users report fuel consumption and calculate the taxes owed to various jurisdictions under the International Fuel Tax Agreement (IFTA). It requires the reporting of different fuel types, including diesel, gasoline, ethanol, and propane, making it versatile for diverse operations. Each quarter, operators must detail their total miles driven in IFTA and non-IFTA jurisdictions, as well as the gallons of fuel used. This information is crucial for determining the taxable gallons and the corresponding tax due. Additionally, the form includes sections for credits, interest calculations, and total amounts due, ensuring that all financial aspects are accounted for accurately. Users should pay close attention to the instructions provided, as they guide the completion of the form and help avoid common mistakes. By maintaining accurate records and completing the IFTA Alabama form diligently, operators can ensure compliance and streamline their tax reporting process.

Understanding the IRP Alabama form can be challenging, and several misconceptions can lead to confusion. Here are four common misunderstandings:

By addressing these misconceptions, individuals and businesses can better navigate the requirements of the IRP Alabama form and ensure compliance.

Check only one fuel type: |

|

|

|

|

Alabama Department of Revenue |

|

|

|

|

|

|

|

|

||||||||||||

|

|

Code |

Fuel Type |

|

|

IFTA Quarterly Fuel Use Tax Schedule |

|

|

|

||||||||||||||||

|

|

|

|

Attach this schedule to Form |

|

|

|

|

|

||||||||||||||||

Tax on: |

D |

(Diesel) |

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

IFT A Quarterly Fuel U se T ax Return. |

|

|

|

|

|

|

|

|

|||||||||||||

|

|

G |

(Motor fuel gasoline) |

|

|

|

|

|

Use this form to report operations for the |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

Prepare a separate schedule for each fuel type. Use |

|

||||||||||||||||||||||

|

|

E |

(Ethanol) |

|

|

|

|

|

quarter ending |

|

|

|

|||||||||||||

|

|

|

|

|

additional sheets if necessary. Make a copy for your records. |

|

|

|

|

. |

|||||||||||||||

|

|

P |

(Propane) |

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Month |

|

Day |

Year |

||||

|

|

__ |

___________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Licensee IFTA identification number |

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

AL |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter credits in brackets ( ). Round to the nearest whole gallon or mile. |

Read instructions (IFTA- 101- I- MN) carefully. |

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MPG Calculation |

|

|

|

|

|

(E) |

Average Fleet MPG |

|||||

(A) Total IFTA Miles |

+ (B) Total Non- IFTA Miles |

= (C) Total Miles |

|

: |

|

(D) Total Gallons |

= |

||||||||||||||||||

(A) |

|

|

|

|

(B) |

|

|

|

(C) |

|

|

|

|

|

(all IFTA and |

|

(2 decimal places) |

||||||||

|

|

|

+ |

|

|

= |

|

|

: |

|

(D) |

|

|

|

= |

(E) |

___ ___ |

. ___ ___ |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

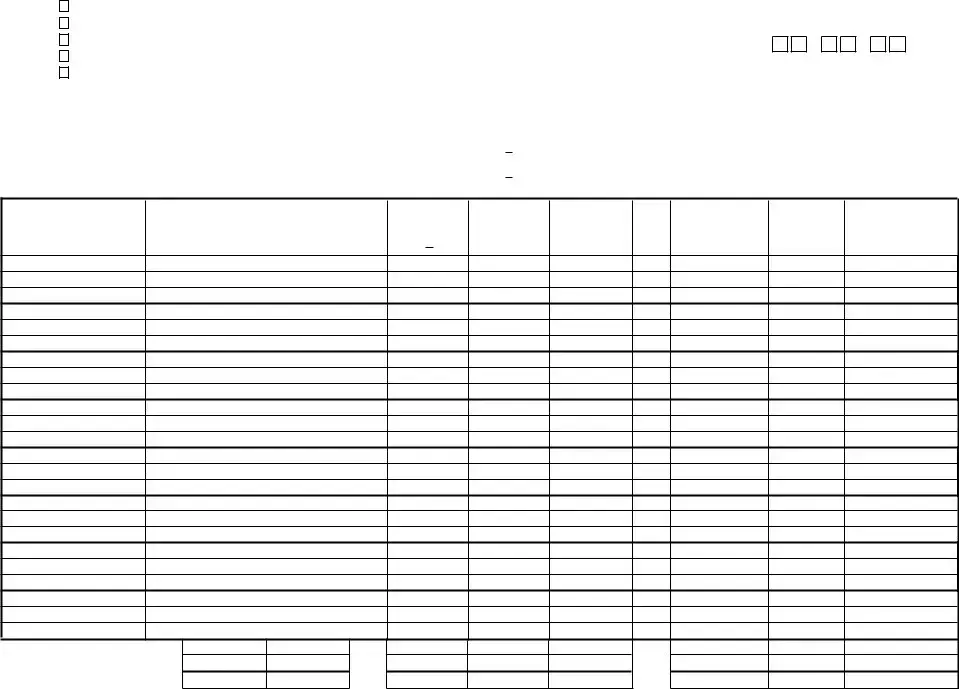

F

Jurisdiction

G

Rate Code

H |

I |

J |

Total IFTA |

Taxable |

MPG |

Miles |

Miles |

from E |

(See Instructions) |

(See Instructions) |

above |

|

|

|

K

Taxable Gallons

(col. I : J)

L

Tax Paid

Gallons

(See Instructions)

M

Net Taxable

Gallons

(col. K - L)

N

Tax Rate

O

Tax (Credit) Due

(col. M x N (Tax) ) (col. K x N (Surch) )

P

Interest

Due

Q

Total Due

(col. O + P)

Subtotals

Subtotals from back

Totals

Important Note: When listing additional jurisdictions and more space is needed, use the back of this form.

For Diesel, Motor fuel gasoline, Ethanol andPropane reported, transfer the total |

|

|

amount in Column Q from each schedule to the corresponding line on |

|

|

Form |

|

|

the total amount of Column Q from each schedule to Column S of the worksheet on the |

IFTA- 101- MN (4/08) |

|

back of Form |

||

|

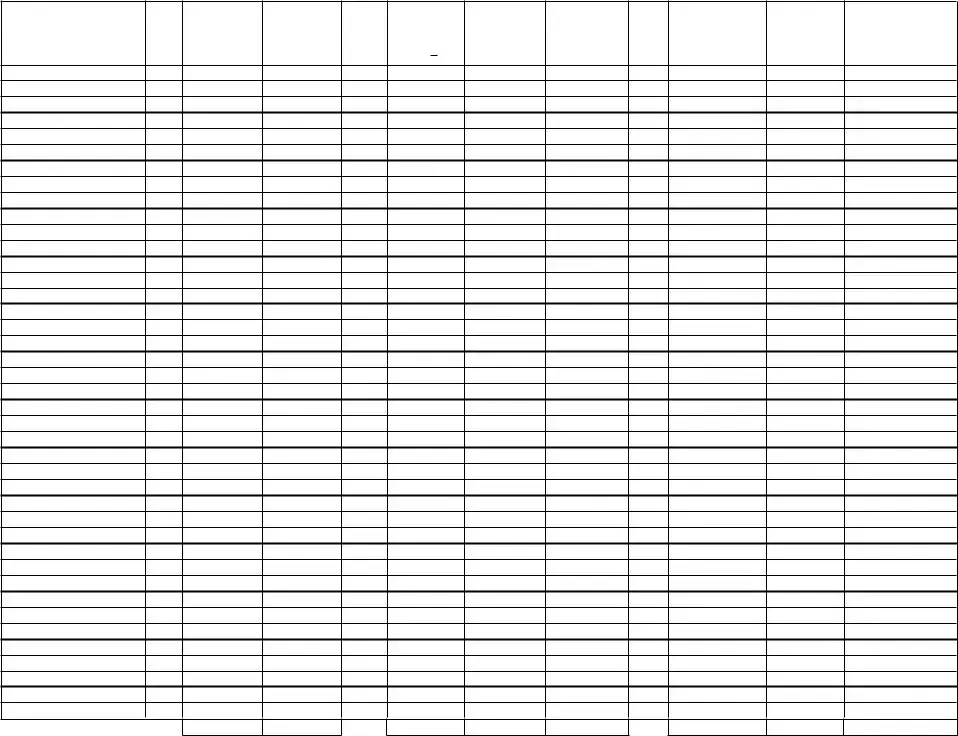

F

Jurisdiction

G

Rate Code

H |

I |

Total IFTA |

Taxable |

Miles |

Miles |

(See Instructions) (See Instructions)

J

MPG

from E on front

K

Taxable

Gallons

(col. I : J)

L

Tax Paid

Gallons

(See Instructions)

M

Net Taxable

Gallons

(col. K - L)

N

Tax Rate

O

Tax (Credit) Due

(col. M x N (Tax)) (col. K x N (Surch))

P

Interest

Due

Q

Total Due

(col. O + P)

Transfer the subtotal am ounts Subtotals

to the front of this schedule.

Anonymous Tip Hotline - Complete and accurate incident reports are essential for successful criminal prosecution.

Completing a Last Will and Testament form is vital for anyone looking to ensure their final wishes are respected and that their estate is managed according to their preferences. This form not only clarifies the distribution of assets but also provides guidance on the care of dependents, making it a cornerstone of effective estate planning.

Do I Need a Bill of Sale If I Have the Title in Alabama - Next of kin who complete the form should retain a copy for their records.

Letters of Testamentary Alabama - This form must be filled out by the person being adopted or their legal representatives.

The IFTA-100-MN form is closely related to the IRP Alabama form. Both documents serve as essential tools for reporting fuel use and taxes related to commercial vehicle operations. The IFTA-100-MN is specifically designed for reporting quarterly fuel use taxes across multiple jurisdictions, while the IRP Alabama form focuses on the registration and licensing of commercial vehicles. Both forms require detailed calculations of miles traveled and fuel consumed, ensuring compliance with state and federal regulations.

The IFTA-101-MN form is another document similar to the IRP Alabama form. This form is used to provide a breakdown of fuel consumption by type, such as diesel or gasoline. Like the IRP Alabama form, it requires users to report specific data related to their operations. The IFTA-101-MN allows for a more granular view of fuel usage, which is crucial for accurate tax reporting and compliance. Both forms emphasize the importance of maintaining precise records for audits and inspections.

The Schedule C (Form 1040) is also comparable to the IRP Alabama form, especially for individuals who operate businesses using commercial vehicles. Schedule C is used by sole proprietors to report income and expenses, including fuel costs. While the IRP Alabama form focuses on vehicle registration and fuel tax reporting, both documents require meticulous record-keeping and accurate reporting of operational costs. This ensures that all deductions and tax obligations are correctly calculated.

The Form 2290, Heavy Highway Vehicle Use Tax Return, shares similarities with the IRP Alabama form as well. This form is specifically for reporting and paying taxes on heavy vehicles that operate on public highways. Both forms require detailed information about vehicle usage and mileage. While the IRP Alabama form addresses registration and fuel tax, Form 2290 focuses on the tax liability associated with heavy vehicle operations, highlighting the importance of compliance in both areas.

The Form 940, Employer's Annual Federal Unemployment (FUTA) Tax Return, also relates to the IRP Alabama form in terms of reporting requirements. While Form 940 deals with unemployment taxes for employees, both forms require accurate tracking of operational details and financial information. Businesses must ensure they comply with tax obligations, whether related to fuel use or employee taxes. This underscores the importance of maintaining thorough records across various tax forms.

In addition to these various tax-related documents, individuals and businesses in West Virginia may also need to consider the implications of liability protection when engaging in different activities. For this purpose, a crucial tool is the Hold Harmless Agreement, which helps in mitigating risks by ensuring that one party does not bear the liability for potential damages or losses incurred by another. This agreement plays a significant role in various business transactions and services, safeguarding interests and promoting clarity while navigating legal obligations.

Finally, the Form 941, Employer's Quarterly Federal Tax Return, is similar to the IRP Alabama form in that it requires businesses to report tax information on a regular basis. Form 941 is used to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. Like the IRP Alabama form, it necessitates accurate record-keeping and timely submissions to avoid penalties. Both forms are integral to ensuring compliance with federal and state tax laws, reinforcing the need for diligent tracking of financial activities.

When filling out the IRP Alabama form, individuals often make several common mistakes that can lead to delays or complications in processing. One frequent error is failing to check the correct fuel type. The form requires that only one fuel type be selected, such as Diesel, Motor fuel gasoline, Ethanol, or Propane. Choosing more than one can create confusion and may result in the form being rejected.

Another mistake is not providing accurate mileage calculations. The form requires a breakdown of Total IFTA Miles and Total Non-IFTA Miles, which must be added together to determine Total Miles. Many individuals overlook this step or miscalculate these figures, which can affect tax calculations and lead to incorrect tax filings.

People also often neglect to round their numbers properly. The instructions specify that entries should be rounded to the nearest whole gallon or mile. Failing to adhere to this guideline can result in discrepancies in the reported figures, causing potential issues with tax assessments.

Additionally, not attaching the required schedules can be a significant oversight. Each fuel type must have a separate schedule, and if these are not included with the submission, it may delay processing. It is essential to ensure that all necessary documents are attached before sending in the form.

Another common error involves misplacing or omitting credits. When entering credits, individuals should use brackets, as indicated in the instructions. Not doing so can lead to misunderstandings regarding the amounts owed or refunded, complicating the overall tax situation.

Lastly, many people forget to make a copy of their completed form for their records. Keeping a copy is crucial for future reference and can be helpful if any questions arise regarding the submission. Without this record, it may be difficult to resolve any issues that come up later.